Credit Default Swaps

100 likes | 372 Views

Credit Default Swaps. An Example. A Pension Fund Investment. A Pension Fund has $1 billion to invest An option is to lend the money to a bank, investment fund, even a corporation or municipality in return for interest.

Credit Default Swaps

E N D

Presentation Transcript

Credit Default Swaps An Example

A Pension Fund Investment • A Pension Fund has $1 billion to invest • An option is to lend the money to a bank, investment fund, even a corporation or municipality in return for interest. • For example, a bank might be willing to borrow the $1 billion and pay an interest rate of 10%. • This is a nice return on the principal, but there is one problem.

Less than stellar rating • The bank that wants to borrow the money might have an AA rating by Moody’s, but the smart money thinks the bank credit rating should be lower. • In other words, the investment community does not believe the crediting rating is accurate. • It would later be found that Moody’s, Standard and Poor’s and other rating agencies were often inflating rating to obtain business. • In this risky environment, the Pension Fund is concerned about making the loan.

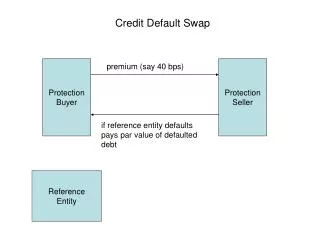

AIG to the Rescue • This is where a company like AIG comes into play. • American International Group (AIG) is an insurance company which does business in 130 countries. • For a fee, AIG is willing to insure the pension fund making the loan against any loss. • In this case, AIG will insure the pension fund for 1% interest per year.

Net benefit to the Pension Fund • The Pension Fund can then loan the money to the bank for 10%, pay AIG 1%, and have a net gain of 9%. • If the bank defaults on the loan, AIG agrees to pay the Pension Fund $1 billion.

What’s Wrong With This? • Here is the problem: companies like AIG are not regulated. • They are not required to maintain cash reserves to pay up if the bank or other creditor defaults. • By fall of 2008 it was clear to the investment community that companies like AIG had insured a great deal of bad debt and that in the case of wide-spread defaults, it could not pay its insured.

In the fall of 2008, the major rating companies downgraded AIG’s credit rating. • When this happened the SEC required AIG to increase its reserves to cover bad debt. • AIG could not do so. • It was in a Liquidity crisis. It did not have the funds required to cover its debt.

What did this mean? • If AIG could not pay its debts, hundreds of banks in America and many other countries would suffer massive losses, often forcing the bank into collapse. • As the banks fell, so also would major investment firms (think Wall Street) in America and around the world.

A Rescue • At this point, the Federal reserve bank and then Congress stepped in to shore up AIG and pay its debts. • In total the bailout by the federal government was $182.5 billion, just to AIG. • The Federal government (taxpayers) became the owner of 79.9% of AIG. • In 2009, AIG tried to use $435 million of the taxpayer money it received to give its executive bonuses.

AIG Debt • By early 2012 about 80% of AIG debt to taxpayers has been repaid. • Taxpayers still own $30 to 40 billion in AIG stock. • The remaining stock is being sold as the market recovers. • In the end, taxpayers should get all their money back and realize a profit.