Download

1 / 40

400 likes | 569 Views

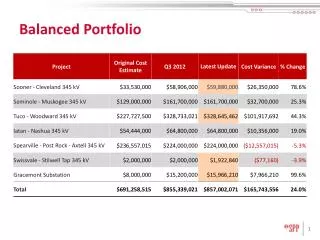

Part 1 Plans, Programs, and the Board of Pensions Balanced Investment Portfolio. 2011 Multiple Investment Programs. Independent plans/programs Diverse funding sources Distinct portfolios Separate accounting. Dues-Based Programs. 31.5% Dues. Pension, Death and Disability. Medical.

E N D

Part 1Plans, Programs, and the Board of Pensions Balanced Investment Portfolio

2011 Multiple Investment Programs • Independent plans/programs • Diverse funding sources • Distinct portfolios • Separate accounting

Dues-Based Programs 31.5% Dues Pension, Death and Disability Medical Board of Pensions 19.5% Dues 12% Dues Benefit Payments to Members Short-term Investments Short-term Investments Board of Pensions Balanced Investment Portfolio

Investment Structure U.S. Stocks International Stocks Fixed Income Alternatives Pension Death & Disability Assistance Programs Endowment Restricted Gifts/Other Programs Board of Pensions Balanced Investment Portfolio

A Portfolio that Reflects the Values of the Presbyterian Church (U.S.A.) • Two voting members on Mission Responsibility Through Investment (MRTI) • Divestment program of the PCUSA • Shareholder resolutions • Proactive proxy voting

2010 Global Market Performance Treasuries sell off Long Treasury bonds rally 2009 equity rally continues Russell 3000 peaks on 4/23/10 19% 17% 17% 13% 9% 8% Commodities lead huge risk asset rally Equity markets sell off ~ All indices include dividends; high yield bonds and long U.S. Treasuries use ETF index values ~

2010 U.S. Equity Market Performance Small stocks surge Small value stocks gain 22% Small growth stocks up 34% since August 31 29% Large stocks perform better during selloff 25% 17% 16% ~ All indices include dividends; high yield bonds and long U.S. Treasuries use ETF index values ~

Returns of Market Indices and Board of Pensions Balanced Investment Portfolio2010 Source: MSCI (net)

Board of Pensions Balanced Investment PortfolioDecember 31, 2010

Part 3: A Time Traveler Back 200 Forward 50 Proverbs, Shakespeare, Malthus, Smith, and Butterfly Wings Interconnected Global Markets in 2011

Demographics -Why It Matters D- Drinking water, discount rates, debts, deficits E-Economic growth, emerging markets, social equality M- Mortality, longevity risk, mega-cities O- Organizational structure and behaviors, outsourcing G- Geopolitical risks, genomics, global labor force R- Retirement, real estate, resource allocation A- Asset prices, asset allocation P- Pensions, pharmaceuticals H- Health, housing I- Inflation, information technology, infrastructure C- Climate, countries, commodities, communications S- Societal structures, investment sectors

“A foolish man devours all he has” Proverbs 21:20

Shakespeare, Hamlet, Act 1, Scene 3 “Neither a borrower nor a lender be, For loan oft loses both itself and friend, And borrowing dulls the edge of husbandry.”

Malthus Food, Glorious Food Smith Debt, Devious Debt

The Outlook for the Future of Food “The power of population is indefinitely greater than the power in the earth to produce subsistence for man.” The Reverend Thomas Robert Malthus, An Essay on the Principle of Population, 1798

Global Yield Growth Source: The Economist

Price Change in Selected Commodities One year ended February 28, 2011 US Stocks: 23% US Bonds: 5% Source: Bloomberg

Food, Revolutionary Food “Let them eat cake” Attributed to Marie-Antoinette, 1791

Impact of Food on Inflation Source: Bridgewater

The Outlook for the Future of Debt “Ordinary expenses ought to be equal to ordinary revenue, and it is well if it does not frequently exceed it.” Adam Smith, Philosopher Wealth of Nations, 1776

Sovereign Debt and DeficitsYear end 2010 Source: Bloomberg, IMF, Colchester

Sovereign Debt Risk Improved Worsened Source: The Economist

Sovereign Debt and GDP (Bubble size illustrates population) Poorer Richer More debt Japan Greece Italy Turkey U.S. Singapore India Ireland Egypt France Portugal Brazil Germany Vietnam Philippines Pakistan Bangladesh Ethiopia Indonesia UK Netherlands Malaysia Norway Spain Poland Denmark Argentina Mexico Canada Taiwan Saudi Venezuela Hong Kong Less debt Australia S Korea Russia Iran Nigeria Algeria China South Africa Source: CIA World Factbook, 2010 levels

The Butterfly Effect “The flapping of a butterfly’s wings might create a minuscule disturbance that, in the chaotic motion of the atmosphere…change the large scale atmospheric motion.” Edward Lorenz, Meteorologist Chaos Theory, 1963

Global Population Growth through a Presbyterian Historical Lens UPCUSA forms 1958 Book of Confessions 1967 Reunion PCUSA 1983 John Calvin born 1509 Fund for Pious Uses 1717 First GA Phila, PA Global population (billions) 1789 Moses born c1250 BC North-South split GreatPyramids c2500 BC Birth of Christ 1861 Rome c750 BC Noah born c3000 BC 1 AD 1000 1750 - 1900 1950 - 2010 70000 BC – 500 BC Source: Wikipedia, Presbyterian Historical Society, spiritrestoration.org

Global Population Growth 20 yrs 14 yrs 12 yrs 12 yrs 13 yrs 14 yrs 33 years 123 years 1804 1927 1960 74 87 99 2011 25(E) 45(E) Source: Wikipedia

Gross Domestic Product Per Capita Levels and 5-Year Growth 2004 - 2009 Source: World Bank, Purchasing Power Parity Basis

The World’s Most Populated Countries - 2010 Rest of World Russia Bangladesh Japan Nigeria Brazil Pakistan U.S. India Indonesia The ten most populated countries account for almost 60% of the world’s nearly 7 billion people China Source: Wikipedia

The World’s Most Populated Countries - 2050 Rest of World Ethiopia Congo Bangladesh Brazil Nigeria Indonesia U.S. Pakistan China By 2050, the ten most populated countries are expected to account for about 55% of the world’s more than 9 billion people. India Source: World Population Prospects, the 2008 Revision

Global Population by Region Global population (billions) Source: UN, 2008 estimates

Estimated Population Growth 2000 to 2050 Global population growth Source: UN, 2008 estimates

The Investing Cycle Point of maximum financial risk Euphoria Anxiety Thrill Denial Point of maximum financial opportunity Fear Excitement Desperation Optimism Optimism Panic Relief Hope Capitulation Depression Despondency

January 1, 2001-December 31, 2010Ten-Year Annualized Investment Returns % • U.S. Large Growth Stocks 0.0 • S&P 500 Stock Index 1.4 • Developed Mkts Int’l Stocks 3.9 • U.S. Govt and Corp Bonds 5.8 • U.S. Small Value Stocks 8.4 • Emerging Markets Bonds 10.9 • Emerging Markets Stocks 16.2

The Importance of Diversification Data: S&P 500, DJ U.S. Completion TSM, MSCI EAFE, MSCI EM, Barclays Capital Government/Credit

Where are We Today? The Outlook for 2011 • Challenging year for investors • Fragile U.S. economy • Global economic and political instability • Natural disasters of epic proportions • Interest rates and inflation will increase

Outlook for 2011 • Selective investments in credit and distressed debt remain attractive • U.S. stocks should outperform international developed markets • Emerging market stocks and bonds will provide superior long-term returns • Inflation protection and real return strategies continue to be implemented

1939 - A Great Church Now Maintains A Great Pension Program The Annual Report of the Board of Pensions of the Presbyterian Church in the United States of America 1939 2011 - Secure Benefits in Uncertain Times