Download

1 / 31

2.04k likes | 6k Views

WorldCom Fraud Presentation. SILKA GONZALEZ BLANCA WEGENER SILVIA OROZCO. Case Introduction. This case involves WorldCom in one of the largest public accounting frauds in history.

E N D

WorldCom Fraud Presentation SILKA GONZALEZ BLANCA WEGENER SILVIA OROZCO

Case Introduction • This case involves WorldCom in one of the largest public accounting frauds in history. • The scheme was devised by WorldCom’s CEO Bernard J. Ebbers and followed through by other senior executives consisting in $11 billion in false or unsupported accounting entries that were made in WorldCom’s financial systems in order to achieve desired reported financial results. • On June 26, 2002, the United States Securities and Exchange Commission (SEC) filed a lawsuit against WorldCom.

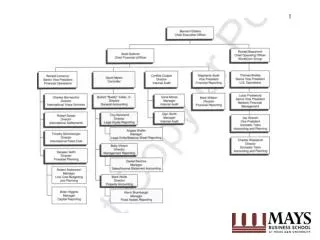

Case Facts • Bernard J. Ebbers, WorldCom’s Chief Executive Officer presented a substantially false picture to the market, to the Board of Directors, and to most of the Company’s own employees. • As he was projecting and then reporting continued growth, he was receiving internal information that was increasingly inconsistent with those projections and reports. • Ebbers was well aware that WorldCom was meeting revenue expectations through the manipulation of financial information. • The fraud was implemented by and under the direction of WorldCom’s Chief Financial Officer, Scott Sullivan.

Case Facts • As business operations fell further and further short of financial targets announced by Ebbers, Sullivan directed the making of accounting entries that had no basis in generally accepted accounting principles in order to create the false appearance that WorldCom had achieved those targets. • As he implemented the fraud, Sullivan was assisted by WorldCom’s Controller, David Myers, who in turn directed other employees to make entries he knew were not supported by valid transactions or business activities. • Upon direction of senior management, it was considered acceptable for the Accounting Departments to make entries of hundreds of millions of dollars with little or no documentation.

Case Facts • Employees in the various Accounting and Financial Departments either knew or suspected that senior financial management was engaged in improper accounting practices, but said nothing for fear of senior management and or even the loss of their jobs. • These included not only employees in Accounting Departments, but employees in other financial reporting and accounting groups whose responsibilities were affected by them. • When employees raised concerns, senior management frequently said that the issue was resolved and accepted at the total consolidated company level.

Case Facts • WorldCom’s improper accounting took two principal forms: • The first form consisted in the reduction of reported line costs, WorldCom’s largest category of expenses. Line costs are the costs of carrying a voice call or data transmission from its starting point to its ending point. • The second form consisted in the exaggeration of reported revenues. • The overall objective of these efforts was to report lower line costs and to continue reporting significant revenue growth when actual growth rates were generally substantially lower.

Case Facts • From the first quarter of 2001 through the first quarter of 2002, WorldCom improperly reduced its reported line costs by $3.8 billion, principally by capitalizing $3.5 billion of line costs. • From the second quarter of 1999 through the first quarter of 2002, WorldCom improperly reduced its reported line costs and increased pretax income by over $7 billion in total. • These line costs were ongoing operating expenses that accounting rules required WorldCom to recognize immediately.

Case Facts • Beginning in 1999, WorldCom personnel made large revenue accounting entries after the close of many quarters in order to report that it had achieved the high revenue growth targets that Ebbers and Sullivan had established. • Investigations found handwritten notes from 1999 and 2000 that calculated the difference between actual or monthly revenue results and target or needed numbers, and identified the entries necessary to make up that difference. Those entries were then made. • Throughout 2001, this process was called “Close the Gap” and was used by WorldCom’s Business Operations and Revenue Accounting groups to track these differences in order to hit the Company’s external growth projections. • This process was directed by Sullivan, and implemented by Ron Lomenzo, the Senior Vice President of Financial Operations and an employee reporting to him, Lisa Taranto.

Case Facts • Other questionable revenue entries that were identified were booked to “Corporate Unallocated" revenue accounts, which often involved large, round dollar revenue items in millions or tens of millions of dollars. • They generally appeared only in the quarter-ending month, and they were not recorded during the quarter, but instead in the weeks after the quarter had ended. • The fraud investigation identified over $958 million in revenue that was improperly recorded by WorldCom between the first quarter of 1999 and the first quarter of 2002. • The investigation also identified $1.107 billion of additional revenue items recorded during this period that they consider questionable.

Case Facts • On June 25, 2002, WorldCom announced that it intended to restate its financial statements for 2001 and the first quarter of 2002. • It stated that it had determined that certain transfers totaling $3.852 billion during that period from “line cost” expenses (costs of transmitting calls) to asset accounts were not made in accordance with generally accepted accounting principles (GAAP). • Less than one month later, WorldCom and substantially all of its active U.S. subsidiaries filed voluntary petitions for reorganization under Chapter 11 of the Bankruptcy Code.

Case Facts • WorldCom subsequently announced that it had discovered an additional $3.831 billion in improperly reported earnings before taxes for 1999, 2000, 2001 and the first quarter of 2002. • It had also written off approximately $80 billion of the stated book value of the assets on the Company’ s balance sheet at the time the fraud was announced. • On June 26, 2002, the United States Securities and Exchange Commission (SEC) filed a lawsuit against WorldCom.

Defendant’s Scheme • WorldCom’s accounting fraud covered the following three main areas: • Accruals • Capitalization • Adjusting Entries

Defendant’s Scheme - Accruals • WorldCom manipulated the process of adjusting accruals in three ways: • First, in some cases accruals were released without any apparent analysis of whether the Company actually had an excess accrual in the account. Therefore, reported line costs were reduced and pre-tax income increased without any proper basis. • Second, even when WorldCom hadexcess accruals, the Company often did not release them in the period in which they were identified. Instead, certain line cost accruals were kept and released to improve reported results when management felt this was needed.

Defendant’s Scheme - Accruals • Third, WorldCom reduced reported line costs by releasing accruals that had been established for other purposes.

Defendant’s Scheme - Accruals • They did not occur in the normal course of day to day operations, but instead in the weeks followingthe end of the quarter in question. • The timing and amounts of the releases were not supported by any analysis or documentation. • Most significantly, WorldCom employees involved in the releases generally understood that they were improper.

Defendant’s Scheme - Capitalization • From the first quarter of 2001 through the first quarter of 2002, WorldCom improperly reduced its reported line costs by $3.8 billion, principally by capitalizing $3.5 billion of line costs at Sullivan’s direction in violation of WorldCom’s capitalization policy and established accounting standards. • The line costs that WorldCom capitalized were ongoing operating expenses that accounting rules required WorldCom to recognize immediately. • By capitalizing operating expenses, WorldCom shifted these costs from its income statement to its balance sheet and increased its reported pre-tax income and earnings per share.

Defendant’s Scheme - Capitalization • If WorldCom had not capitalized these expenses, it would have reported a pre-tax loss in three of the five quarters in which the improper capitalization entries occurred. • For the fourth quarter of 2001, WorldCom reported a pre-tax income of $401 million instead of a pre-tax loss of $440 million because it capitalized $841 million of line costs. • Similarly, the improper capitalization of $818 million in line costs for the first quarter of 2002 allowed WorldCom to report pre-tax income of $240 million instead of a $578 million pre-tax loss.

Defendant’s Scheme – Adjusting Entries • Beginning in 1999, WorldCom personnel made large revenue accounting entries after the close of many quarters in order to report that it had achieved the high revenue growth targets that Ebbers and Sullivan had established.

Corporate Governance • The Board of Directors, though apparently unaware of the fraud, played far too small a role in the life, direction and culture of the Company. • The outside Directors had little or no involvement in the Company’s business other than through attendance at Board meetings. • Ebbers controlled the Board’s agenda, its discussions and its decisions. • Ebbers created, and the Board permitted, a corporate environment in which the pressure to meet the numbers was high, the departments that served as controls were weak, and the word of senior management was final and not to be challenged.

Corporate Governance • With limited exceptions, the members of the Board were reluctant to challenge Ebbers even when they disagreed with him. • For example, beginning in September of 2000 the board authorized corporate loans and guaranties that grew to over $400 million so that Ebbers could avoid selling WorldCom stock to meet his personal financial obligations. • A second example is the board’s failure to challenge Ebbers on the extent of his substantial outside business interests. • Those interests included a Louisiana rice farm, a luxury yacht building company, a lumber mill, a country club, a trucking company, a minor league hockey team, an operating marina, and a building in downtown Chicago.

Corporate Governance • The Audit Committee members did not have a sufficient understanding of the Company’s internal financial workings or its culture, and they devoted little time to their role, meeting as little as three to five hours per year. • Neither WorldCom’s Legal Department nor Internal Audit Department was structured to maximize their effectiveness as a control structure upon which the Board could depend. • At Ebbers’ direction, the Company’s lawyers were in fragmented groups. • Even the Internal Audit Department reported in most respects to Sullivan and until 2002 its duties generally did not include financial reporting matters.

External Auditors • Arthur Andersen, WorldCom’s independent external auditors, failed to detect the fraud by relying too heavily on senior management and did not conduct tests to corroborate the information it received in many areas. • Andersen conducted only very limited audit procedures in many areas where accounting irregularities were found. • WorldCom also used excessive control over Andersen’s access to information and was not candid in its dealings with Andersen. • WorldCom personnel who dealt most often with Andersen controlled Andersen’s access to information in several respects. • However, it was Andersen’s responsibility to overcome those obstacles, to perform an appropriate audit, and to inform the Audit Committee of the difficulties it faced, but it did not.

How They Were Caught • In the spring of 2002, within two months after Ebbers’ resignation as Chief Executive Officer in April 2002, the Internal Audit Department started a review of capital expenditures. • Personnel in other areas of WorldCom also questioned Sullivan or Myers about the accounting entries. Myers ultimately acknowledged to the Internal Auditors that he could not support the capitalization of line costs. • The Audit Committee of WorldCom’s Board of Directors, once advised of the issue, took it seriously and directed prompt attention to it.

How They Were Caught • After providing Sullivan the opportunity to justify the accounting, WorldCom and their external auditors concluded that the capitalization entries were improper. • The Board of Directors immediately terminated Sullivan, obtained Myers’ resignation and WorldCom disclosed the improper capitalization to the SEC and the public. • On June 26, 2002, the United States Securities and Exchange Commission (SEC) filed a lawsuit against WorldCom.

Outcome • Criminal arrest took place as early as August 2002. • In March 2004, WorldCom’s Chief Financial Officer, Scott Sullivan pled guilty and the government unsealed the indictment against Chief Executive Officer, Bernard J. Ebbers. • On March 15, 2005, a federal jury in the Southern District of New York found Bernard J. Ebbers, former CEO of WorldCom, guilty on all counts, which included conspiracy, securities fraud, and false regulatory filings.

Outcome • These charges relate to Ebbers’ role in WorldCom’s submission of fictitious financial statements to the SEC between October 2000 and June 2002, which resulted in a loss of $11 billion. • In addition to the conviction of Ebbers, five additional WorldCom executives have been convicted: Scott Sullivan, Chief Financial Officer (CFO); David Myers, Controller; Buford Yates Jr., Director General Accounting; Troy Normand, Director Legal Entity Accounting; and Betty Lynn Vinson, Director Management Reporting.

Outcome • On July 13, 2005, Bernard Ebbers was sentenced to 25 years in prison for his involvement in the $11 billion fraud that led to the collapse of WorldCom. • The unusually long prison term is part of a series of penalties against corporate executives who defrauded investors in recent years. • The government expects that the severity of the punishment will discourage other executives from cheating investors.

Outcome • Prosecutors hope these convictions will give them more power to negotiate settlements with executives accused of wrongdoing and to persuade involved individuals into testifying against their former bosses. • The other former WorldCom executives and accountants will be facing their sentencing in August 2005. • In addition to the criminal charges, there have been multiple civil lawsuits. The primary ones are a civil lawsuit from the shareholders and another one from the Security Exchange Commission against Bernard Ebbers and other WorldCom’s executives. Mr. Ebbers has agreed to settle the stockholders’ lawsuit.

Outcome • The accounting fraud of WorldCom led to the largest bankruptcy in United States history and caused billions of dollars in losses to shareholders and employees. • A total of 20,000 employees lost their jobs when WorldCom filed for bankruptcy protection. • Bernard Ebbers‘ criminal charge’s sentencing came three years after the collapse of WorldCom, which pushed lawmakers to approve the Sarbanes-Oxley Act, the most far reaching change in American securities laws since the Depression.

Opinion • This case indicates how corporations and businesses in general place too much importance on monetary performance. • They measure and reward such performance with higher salaries and bonuses. However, the business world does not measure and reward individuals based on ethics. • Additionally, the case shows that when individuals are under pressure to perform, fraudulent actions can be seen by some of them as an option.

Opinion • Some believe they can justify their unethical behavior, even CPAs who should conduct themselves with the highest ethical standards. • This case also indicates how the lack of proper corporate governance and controls can affect an institution as well as all parties related to the entity. • It clearly identified the importance of well structured Board of Directors, Audit Committees, Internal Audit Departments and Legal Departments. • Furthermore, the case shows that deficiencies in an audit approach can lead to the failure of detecting major fraud activities.