Download

1 / 4

40 likes | 124 Views

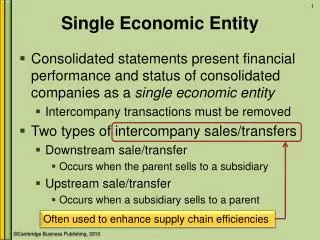

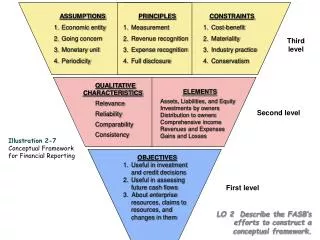

ASSUMPTIONS Economic entity Going concern Monetary unit Periodicity. PRINCIPLES Measurement Revenue recognition Expense recognition Full disclosure. CONSTRAINTS Cost-benefit Materiality Industry practice Conservatism. Third level. QUALITATIVE CHARACTERISTICS Relevance Reliability

E N D

ASSUMPTIONS • Economic entity • Going concern • Monetary unit • Periodicity • PRINCIPLES • Measurement • Revenue recognition • Expense recognition • Full disclosure • CONSTRAINTS • Cost-benefit • Materiality • Industry practice • Conservatism Third level QUALITATIVE CHARACTERISTICS Relevance Reliability Comparability Consistency ELEMENTS Assets, Liabilities, and Equity Investments by owners Distribution to owners Comprehensive income Revenues and Expenses Gains and Losses Second level Illustration 2-7 Conceptual Framework for Financial Reporting OBJECTIVES 1. Useful in investment and credit decisions 2. Useful in assessing future cash flows 3. About enterprise resources, claims to resources, and changes in them First level LO 2 Describe the FASB’s efforts to construct a conceptual framework.

ASSUMPTIONS • Economic entity • Going concern • Monetary unit • Periodicity • Accrual • PRINCIPLES • Measurement • Revenue recognition • Expense recognition • Full disclosure • CONSTRAINTS • Cost • Materiality Third level • QUALITATIVE CHARACTERISTICS • Fundamental qualities • Enhancing qualities • ELEMENTS • Assets • Liabilities • Equity • Income • Expenses Second level Illustration 2-7 Framework for Financial Reporting OBJECTIVE Provide information about the reporting entity that is useful to present and potential equity investors, lenders, and other creditors in their capacity as capital Providers. First level LO 2 Describe efforts to construct a conceptual framework.