Download

1 / 10

100 likes | 262 Views

The European Central Bank warned on Wednesday that the euro zone’s slumping economy and a surge in problem loans were raising the risk of a renewed banking crisis, even as overall stress in the region’s financial markets had receded. http://www.enotes.com/homework-help/westhill-consulting-reviews-jakarta-open-437809

E N D

Risk of Bank Failures Is Rising in Europe, E.C.B. Warns http://www.nytimes.com/2013/05/30/business/global/risk-of-bank-failures-rising-in-europe-ecb-warns.html?pagewanted=all&_r=1&

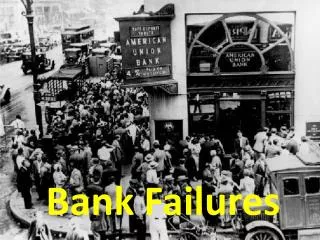

A bank in Athens. Recession has made it harder for many borrowers to repay their loans.

FRANKFURT — The European Central Bank warned on Wednesday that the euro zone’s slumping economy and a surge in problem loans were raising the risk of a renewed banking crisis, even as overall stress in the region’s financial markets had receded. In a sober assessment of the state of the zone’s financial system, the E.C.B. said that a prolonged recession had made it harder for many borrowers to repay their loans, burdening banks that had still not finished repairing the damage caused by the 2008 financial crisis. Last year “was not a good year for banks at all,” Vítor Constâncio, the vice president of the E.C.B., said Wednesday. While the E.C.B., as customary, did not mention specific banks, it said the most vulnerable were those in countries with high unemployment or falling house prices. That list would include Italy, Spain, Greece and Portugal among others. But ailing banks are also a problem in stronger countries like Germany, where Commerzbank and publicly owned landesbanks, or state banks, are struggling with bad loans to the shipping industry and other problems.

Germany has drawn criticism for lecturing other countries on excessive government debt, while trying to protect its own banks from greater scrutiny. “They are very virtuous when they look at national accounts but less when they are looking at their own banks,” said Stefano Micossi, an economist who is director general of Assonime, an Italian business group. The E.C.B. takes the pulse of the European financial system every six months, but the latest report, running 128 pages, has particular importance as the central bank prepares to become the supreme regulator of euro area lenders. The report also raised concerns about whether banks were systematically underestimating risk, and served as a reminder of the monumental task that lies ahead for the E.C.B. when it assumes its new powers next year. A similarly dim snapshot of the state of the euro zone economy was issued Wednesday by the Organization for Economic Cooperation and Development in Paris. It warned of the dangers posed by weakly capitalized banks, a problem it said underlined the need for E.U. leaders to push through with a so-called banking union that would include centralized supervision of lenders.

The limited ability of European banks to absorb losses and the lack of a full banking union are potential threats to achieving a lasting stability, the O.E.C.D. said. Reduced tensions on financial markets seem to have dampened the desire to push for progress in creating joint banking mechanisms, it added. “It is important to strengthen the capital of financial institutions so that they can withstand sovereign debt write-downs if rules prove insufficient to prevent sovereign crises,” the O.E.C.D. report said. The O.E.C.D., based in Paris, predicted that gross domestic product in its 34 member countries, all of which have developed economies, would grow 1.2 percent this year, slightly below the 1.4 percent it forecast six months ago. Unemployment, especially in Europe, remains a persistent problem contributing to the uneven pace of growth globally, the O.E.C.D. said. It warned European countries that failing to address the issue would undermine the progress made from the fiscal and structural adjustments that many countries have pushed through in recent years.

The E.C.B., as part of changes designed to avert future financial crises, will begin supervising the euro area banks sometime next year, depending on when changes in E.U. law are approved by the European Parliament. The E.C.B. has already begun preparing to assume the new powers. The report issued Wednesday raised the question of whether the E.C.B. would be more willing than national regulators to require banks to confront problems like problem loans or other damaged assets. Many analysts say the euro area still has numerous so-called zombie banks, which are close to bankruptcy but have kept their losses hidden. Mr. Micossi of Assonime said he expected the E.C.B. to be an aggressive regulator. But the central bank will need time to hire the necessary staff and will face resistance from national regulators reluctant to give up power. “We can expect the E.C.B. in due course to fully play its role,” Mr. Micossi said by telephone from Rome. “My impression is this will not happen very fast, however.”

“National oversight structures are very resistant, and they will renounce as little power as they can,” he said. Over all, the E.C.B. was somewhat more upbeat about the euro area’s financial system than it was in its last review, in December. There is less concern that governments will default on their debt, the E.C.B. said, and banks in countries like Spain and Greece are having an easier time attracting deposits and raising funds. “Euro area systemic stress is at its lowest point in two years,” the E.C.B. said in the report. But the E.C.B. suggested that one reason for the lower stress was that, with official interest rates at record lows, investors were hunting for better returns and becoming more willing to buy bonds of countries like Italy, Spain and Portugal. Those countries’ borrowing rates could soar again if anything happens to unsettle investors, including political turmoil. The central bank and O.E.C.D. reports could also sharpen the debate about what, if anything, policy makers could do to stimulate lending in the most troubled countries.

Eckhard Wurzel, an economist with the O.E.C.D., predicted that if the 17 euro zone countries maintained their pace at overhauling the weaker economies, and continued to strengthen policies at the E.U. level, including implementing a banking union, a real turnaround could be seen as early as 2015. ‘‘We are on the edge of stabilizing the sovereign debt,’’ Mr. Wurzel said. ‘‘But there needs to be more at the E.U. level.’’ Without changes within the wider euro zone, he said, long-term prospects for growth would be unattainable. Meanwhile, lending to individuals and businesses in the euro zone continued to decline, according to figures reported separately Wednesday by the central bank. The E.C.B. repeated that it was looking at ways to restart the market for asset-backed securities, bundles of loans that are sold to investors. By selling loans they have issued, banks raise money to issue more loans. But the E.C.B. repeated calls for governments and bankers to do more. E.C.B. action “cannot — and indeed should not — replace measures in both the public and private sectors to address underlying vulnerabilities in balance sheets of both banks and sovereigns,” the central bank said.

There has been speculation that the E.C.B. might soon begin charging banks interest to park money at the central bank, in order to induce them to lend the excess cash instead. Mr. Constâncio said Wednesday that the E.C.B. had been intensively analyzing the consequences of a so-called negative deposit rate but had not made a decision. There is very little precedent for such a policy, and the effects are difficult to predict. Mr. Constâncio said a negative rate in Denmark caused banks to raise the interest rates they charged customers, to cover the cost of interest paid to the central bank. Such a result would be the opposite of what the E.C.B. is trying to achieve. “It’s a very difficult issue to assess,” Mr. Constâncio said. One problem for European banks, the E.C.B. said, is that outsiders still have doubts on whether they have been straightforward about how much risk they have on their books.

“A growing chorus of analysts, investors and regulators have expressed concern about the murkiness of banks’ internal models” for measuring risk, the E.C.B. report said. The bank referred to studies showing a huge variance in the way banks estimate potential losses from loans, derivatives or other business activities. The studies suggest that the banks’ methods ‘'might not in all cases be an accurate gauge of the true riskiness of the portfolios of financial institutions.” Mr. Constâncio said that when the E.C.B. took over bank supervision, the discrepancies were something it “will have to look into.” Melissa Eddy contributed reporting from Berlin.