Download

1 / 19

220 likes | 562 Views

Relations between External Audit, Internal Audit and Financial Inspection. Joop Vrolijk, OECD/Sigma PEMPAL Plenary meeting IA CoP Budapest, 18 June 2012. Content Presentation. Audit function in Public Sector Key elements of External Audit, Internal Audit and Financial Inspection function

E N D

Relations between External Audit, InternalAudit and Financial Inspection Joop Vrolijk, OECD/Sigma PEMPAL Plenary meeting IA CoP Budapest, 18 June 2012

Content Presentation Audit function in Public Sector Key elements of External Audit, Internal Audit and Financial Inspection function Co-ordination and Co-operation between IA and EA Practice in Europe Conclusions

1. Audit function in Public Sector The audit function strengthens public governance by providing for accountability and protecting the core values of government—ensuring managers and officials conduct public services transparently, fairly, and honestly

2.1. Key elements of External Audit • Based on constitution or Law • Assurance and advisory function to help National Assembly to hold Government to account • Functionally, Operationally and financially independent from National Assembly and Government • No governmentaloperationalorcontrollingactivities • Assesses adequacy of Government operations through: • Regularity Audits, Compliance audits; Performance audits; IT audits, etc • Makes recommendations for improvement of Government systems in interest of tax-payer • Reports directly to National Assembly and Government • Highest standards of professionalism, confidentiality, impartiality, objectivity, integrity applied

2.2. Key elements of Internal Audit • Based on a Law or secondary legislation with clear mandate • Assurance and advisory function to help manager to fulfill his responsibility • Functionally and operationally independent from management • No managing orcontrollingactivities • Assesses adequacy of internal systems through: • Compliance audits; Performance audits; IT audits • Makes recommendations for system improvement: protect management from financial corrections (by e.g. financial inspection) • Unrestrictedaccess to staff, property and records • Reports directly to topmanagement • Highest standards of professionalism, confidentiality, impartiality, objectivity, integrity applied

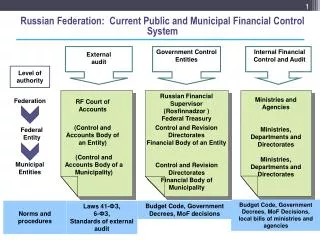

2.3 Key elements of Financial Inspection (B) Based on a Law or secondary legislation Ex post financial checks for compliance with the laws of all public organisations and state owned companies Work is transaction based Corrects/ punishes human and organisational errors and tries to recover damages No appeal procedure Fines in cases of administrative violations stipulated in the laws Report to Ministry of Finance Sends copies of reports to Prosecutor's office, when appropriate

2.4 Financial Inspection versus Internal Audit Financial Inspection ex-post checks – mainly yes/no (law compliance) from outside (bit inside executive branch of financial activities focused on transactions aim to detect violations and to impose penalties Checking past with focus on penalising – to impose financial and budgetary discipline NO International standards No operational but has controlling tasks Internal Audit ex-post assessment and consulting from inside ministry of all activities focused on systems aim to assess functioning systems and to recommend improvements Review current situation and past but focus on future - to support management Use International Standards (IIA) No operational or controlling tasks

2.5 Financial Inspection versus External Audit Financial Inspection ex-post checks – mainly yes/no (law compliance) from outside (MoF) but inside executive branch of financial activities focused on transactions aims to detect violations and to impose penalties checking the past with focus on penalising – to impose financial and budgetary discipline NO International standards no operational but has controlling tasks External Audit ex-post certification of accounts, compliance with laws and VFM from outside executive branch (Independent!) of all activities focus on systems, output and outcome and numbers aims to give assurance to NA on reliability of accounts, compliance and VFM reviewing the current situation with focus on the future - to support NA in holding Gov. to account Use International Standards (ISSAI) No operational or controlling tasks

3.1 Co-ordination and Co-operation EA and IA. Why? • Mutual interests for co‑ordination • Prevent overlaps and duplications • Reduce demands on time of auditee’s staff • Broader perspective: creating a common audit culture in the public sector • SAI’s interest in development of (independence) of IA profession • Impact on overall development of internal control in Governments operations

3.2 Pre-conditions for effective co-operation Effective existence of IA and EA Sound basis, preferably legal Co‑ordination and co-operation must be based on mutual respect and integrity Demands: Commitment, Consultation, Communications, Confidence Independence of SAIs is sometimes barrier, but need for supportive SAIs

3.3 Opportunities for co-operation between SAI- IA units Main co-operation area’s • SAI’s review of IA’s work in order to rely on IA work • Exchange planning and co-ordination audit activities, having the additional benefit of being cost-effective. • Measuring and evaluating effectiveness of PIFC system and Compliance with Laws and Regulations regarding IA Additional area’s • Regular meetings for exchanging information • Consultation on objectives, strategies, audit activities • Sharing expertise and staff exchange • Chances to work in joint audit teams (Regional Organisations)

3.3 Opportunities for co-operation between SAI and CHU Main co-operation area’s • Developing methodology, standards and definitions, a common understanding and terminology for FMC and IA • Assessing audit consequences of introduction of new systems/new initiatives of Government Additional Co-operation Area’s • Regular meetings for exchanging information • Consultation on objectives, strategies and activities • Testing IT programmes • Common training programmes • Sharing expertise and staff exchange SAI interest in well-functioning CHU • Support in developing internal audit capacity • Acknowledgement of risks faced by CHU (status, resistances and lack of staff and other resources)

4. Practice in Europe All SAIs monitor IA development AG model SAI SAI Law: CZ Rep, Netherlands, Bulgaria Formal agreement: SAI-MoF: Poland, Bulgaria, Romania SAI reliance on internal audit work: Denmark, Estonia, Netherlands, UK Planning: Ireland, Denmark Methodological support to CHU/MoF: CZ Rep, Estonia, Netherlands, Poland, UK Training: CZ Rep, Estonia, Slovenia Secondment: Estonia, Netherlands Court model SAI Transition Inspection to IA: France. A priori audit: Belgium, Greece, Spain, Italy, CC and Potential CC: IA in very early days, SAI’s more developed: mutual respect absent No cooperation but competition!!

5. Conclusions Respective roles are different, but co-operation helps both parties achieve their objectives better and easier Co-ordination and co-operation provide more efficient and effective, service to the organisation they work for and ultimately to parliament and the public.

BUT: DISCUSSION ON EQUAL BASIS IN HARMONISED WAY WITH RESPECT FOR EACH OTHERS ROLE AND RESPONSIBILITY IN STRENGHTENING PUBLIC GOVERNANCE

6. Financial Inspection AFTER full implementation of IC Still based on a Law or secondary legislation and Should still cover the whole public sector, but Should only focus on potential risks of fraud, corruption or major financial abuse (such as a bankruptcy of a municipality) and Programme of activity should be determined by complaints about activities where those complaints suggest possible fraud, corruption or major financial abuse. An intelligence service (= data-base) is indispensable The Inspection Service will report to Minister of Finance and Will cooperate closely with the CHU/IA, IA units , SAI and the Prosecutor's office

Thank you! joop.vrolijk@oecd.org