Download

1 / 11

110 likes | 233 Views

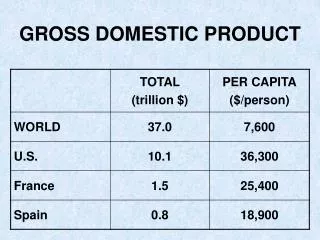

Gross Domestic Product. Definitions. GDP – final value of all goods and services produced within a country in a year. Nominal GDP – GDP reported in current prices. Real GDP – GDP adjusted for inflation. Inflation – An overall rise in prices.

E N D

Definitions • GDP – final value of all goods and services produced within a country in a year. • Nominal GDP – GDP reported in current prices. • Real GDP – GDP adjusted for inflation. • Inflation – An overall rise in prices. • Real per capita GDP - Real GDP divided by the countries population. • GDP deflator – price index that reduces current prices into prices of a base year.

Shortcomings of GDP • Not a perfect indicator of the well-being of the people. • Does not measure goods and services that people produce but do not sell. • Does not measure goods that a household produces and consumes its self. • Does not measure the value of leisure time. • Does not measure the value of illegal activities.

Productivity • Output of goods and services measured per unit of input. • Labor, capital, land • When productivity goes up more goods are produced by the same amount of resources. • Per capita GDP only increases when production grows faster than population. • Labor productivity – amount work force can produce during a given period of time.

Keys to Productivity • Quality of human resources – education, training, attitude. • Quality of management – Example: Henry Ford – installed assembly line as new method of producing cars.

Raising Productivity • Customer satisfaction – give customers what they want and expect. Conduct research or a survey to assess this. • High-quality work – set clear quality standards. Provide training and equipment to guarantee standards are met. • Employee involvement – LISTEN to employees. “Empower” employees. Involve them in decision making.

Shared vision – nurture employees commitment to company and its goals. Mission statements, company slogans, internal reward systems to recognize employee contributions.

Production and Cost Changes • Fixed costs – remain the same –real estate, taxes, managers salaries. • Variable costs – wages, utilities, raw materials. • Fixed plus variable equals total costs. • Average costs – costs divided by units produced. • Marginal cost – additional cost of increasing a unit of production.

Law of Diminishing returns • As more and more variable resources are added to fixed resources production eventually decreases. • Decreasing amount produced leads to increasing costs. • Beyond a certain point production won’t be profitable. • Marginal revenue – sales from additional products.

Marginal Analysis • Compares marginal benefits and marginal costs. • When marginal costs exceeds marginal revenue companies will stop production. • Marginal revenue = marginal costs – profits are maximized.

Economies of Scale • When a company reaches the point where it can employ large-scale production methods it has economy of scale. • cost per unit produced gores down. • Benefits – 1.divide labor into specialized tasks. 2. discounts on purchase of supplies. 3. use of specialized machinery and equipment. 4. invest in research and development.