Download

1 / 14

140 likes | 145 Views

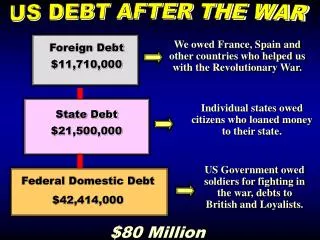

A Brief Discussion on… U.S. Debt Situation ~ Taking the ire out of dire ~. Presented by: Paul Winghart Senior Fixed Income Strategist -Vice President The Fixed Income Strategies Group. Please note important disclosures on pg. 10. $40,000 per Citizen.

E N D

A Brief Discussion on…U.S. Debt Situation ~Taking the ire out of dire ~ Presented by: Paul Winghart Senior Fixed Income Strategist -Vice President The Fixed Income Strategies Group • Please note important disclosures on pg. 10

The U.S. Debt Situation – Taking the “ire” out of “dire” $40,000 per Citizen • A bellwether for borrowing tendencies, US debt outstanding has taken a “hockey stick” appearance. • 1 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” Acceleration & Velocity • Productivity and borrowing (i.e. leverage) have a very unique fundamental relationship • 2 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” Mental Quality with a Physical Thing1 • “The suffix "-ivity", …refers to improvement in the whole collection of related abilities of people, their knowledge and tools in applying to their environment for increasing the useful products they can produce.” Philip Forbes Henshaw1Philip Forbes Henshaw on natural systems(those special machines of nature and how they record their accumulative learning)http://www.synapse9.com/ • Productivity = Output / Hour = (Product / Hour) / Hour = Product / Hour2 • 3 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” A Sea of Change • The Dow Jones Industrial Average August 30, 1982 February 19, 2008 • The growth of the financial sector was in accordance with the economy’s needs. • 4 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” Beyond the Crossroads • “For the moment, the broadly unanticipated behavior of (world) bond markets remains a conundrum.” • –Alan Greenspan then-Chairman of the Federal Reserve giving the Board's semiannual Monetary Policy Report to Congress February 16, 2005. • 5 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” Minding the Gap • Suspect to further pockets of sporadic and severe illiqudity and deflation • 6 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” The Subtle Impact • Trends in consumption are suffering from the further erosion of price stability. • 7 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” The Cost of Money • Longer-term interest rates have pressed lower, undaunted and unabated since the early 1980s • 8 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” Is Borrowing Out of Control? • Logarithmic Scale • A very natural and healthy progression for a maturing service economy • 9 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” In Summary • The economy will tend to underperform its potential until the Fed establishes long-term neutrality • (High Quality) Interest rates and the unemployment rate will fall more often than not as too will wages & prices • Its not the amount of debt that’s the issue, its where it is originating from that is making it relatively ineffective • 10 of 10

The U.S. Debt Situation – Taking the “ire” out of “dire” Appendix I In this environment, long-term interest rates have trended lower in recent months even as the Federal Reserve has raised the level of the target federal funds rate by 150 basis points. This development contrasts with most experience, which suggests that, other things being equal, increasing short-term interest rates are normally accompanied by a rise in longer-term yields. The simple mathematics of the yield curve governs the relationship between short- and long-term interest rates. Ten-year yields, for example, can be thought of as an average of ten consecutive one-year forward rates. A rise in the first-year forward rate, which correlates closely with the federal funds rate, would increase the yield on ten-year U.S. Treasury notes even if the more-distant forward rates remain unchanged. Historically, though, even these distant forward rates have tended to rise in association with monetary policy tightening. In the current episode, however, the more-distant forward rates declined at the same time that short-term rates were rising. Indeed, the tenth-year tranche, which yielded 6-1/2 percent last June, is now at about 5-1/4 percent. During the same period, comparable real forward rates derived from quotes on Treasury inflation-indexed debt fell significantly as well, suggesting that only a portion of the decline in nominal forward rates in distant tranches is attributable to a drop in long-term inflation expectations.

The U.S. Debt Situation – Taking the “ire” out of “dire” Appendix II Greenspan is at a loss for words when explaining the retrenchment in long- term yields during the most recent tightening of monetary policy. Although he goes on to list the usual suspects (mortgage hedging, demand from foreign central banks), he seemingly takes great pains to downplay reduced inflation expectations as a reason for lower long-term interest rates That being said, consumer-based inflation would have to expand at a pace slightly greater than its 10yr average (based on empirical CPI returns) in order to keep up with the stated yearly coupon rate of the basic Treasury. Therefore, it may be more of a supply issue, than an inflation issue, that is holding TIPs yields lower. . Despite the growing but limited supply, portfolio managers have unabashedly recommended TIPs as the asset of choice for the past few months. If CPI fails to impress and the government continues to favor new issuance of the product, TIPs investors, at current levels, are at risk to under-perform the rest of the market. If it weren’t for the dearth of supply, it seems as though the spread would be much tighter than it currently is, underscoring a lower expectation for inflation going forward then presently reported.

The U.S. Debt Situation – Taking the “ire” out of “dire” Appendix III “However, inferences about investors’ inflation expectations based on TIPS have been complicated over recent years by special factors such as the safe-haven demands for nominal Treasury securities and changes over time in the relative liquidity of TIPS and nominal Treasury securities.”