Download

1 / 11

110 likes | 300 Views

CENVAT CREDIT. by g. natarajan, advocate swamy associates. CONCEPT OF CENVAT CREDIT. Milestones – 1986, 1994 & 2004. Inputs. Capital Goods. Input Services. INPUTS. Inputs definition amended – from 01.04.2011. - all goods used in the factory;

E N D

CENVAT CREDIT by g. natarajan, advocate swamy associates

CONCEPT OF CENVAT CREDIT • Milestones – 1986, 1994 & 2004. • Inputs. • Capital Goods. • Input Services.

INPUTS • Inputs definition amended – from 01.04.2011. • - all goods used in the factory; • - accessories cleared along with final product; • - goods meant for free warranty; • - all goods used for generation of electricity / steam; • - all goods used for providing output service. • Exclusions: • - Diesel, Petrol; • - goods used for construction, foundation, support • structures; • - Capital goods, except when used as parts of • final products; • - Goods primarily used for personal use by employees; • - Goods having no nexus to manufacture.

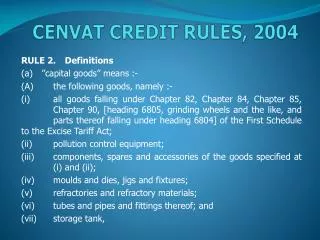

CAPITAL GOODS • ”capital goods” means :- • (A) the following goods, namely :- • all goods falling under Chapter 82, Chapter 84, Chapter 85, Chapter 90, [heading 6805, grinding wheels • and the like, and parts thereof falling under heading 6804] of the First Schedule to the Excise Tariff Act; • (ii) pollution control equipment; • (iii) components, spares and accessories of the goods specified at (i) and (ii); • (iv) moulds and dies, jigs and fixtures; • (v) refractories and refractory materials; • (vi) tubes and pipes and fittings thereof; and • (vii) storage tank, • used - • in the factory of the manufacturer of the final products, but does not include any equipment or appliance • used in an office; or • (1A) used outside the factory of the manufacturer for generation of electricity for captive use within the factory ; or • (2) for providing output service; • motor vehicle registered in the name of provider of output service for providing taxable service as • specified in sub-clauses (f), (n), (o), (zr), (zzp), (zzt) and (zzw) of clause (105) of section 65 of the Finance Act; • (C) dumpers or tippers, falling under Chapter 87 of the First Schedule to the Central Excise Tariff Act, 1985 (5 of 1986), registered in the name of provider of output service for providing taxable services as specified in sub-clauses (zzza) and (zzzy) of clause (105) of section 65 of the said Finance Act;] • components, spares and accessories of motor vehicles, dumpers or tippers, as the case may be, • used to provide taxable services as specified in sub-clauses (B) and (C);]

INPUT SERVICE Input service definition amended. - used for providing output service; - used by a manufacturer of final products, whether directly or indirectly, in or in relation to manufacture and clearance of final products up to place of removal; and includes services used in relation to modernisation, renovation or repairs of a factory, premises of provider of output service or an office relating to such factory or premises, advertisement or sales promotion, market research, storage upto the place of removal, procurement of inputs, accounting, auditing, financing, recruitment and quality control, coaching and training, computer networking, credit rating, share registry, security, business exhibition, legal services, inward transportation of inputs or capital goods and outward transportation upto the place of removal.

INPUT SERVICES • Exclusions. • - Architect, Port Service, Airport Services, commercial or industrial • construction, construction of residential complex, works contract • service – if used for construction of building / civil structure or for • laying of foundation / structures for capital goods – except where • the output services are also the above. • - Insurance of vehicles, rent a cab, service center, supply of tangible • goods (vehicles), except for courier, tour operator, rent a cab, • cargo handling, GTA, outdoor catering, pandal and shamiana. • - Employee welfare services.

RULE 6 • Exempted Vs Taxable activity. • Maintenance of separate records for • Inputs / Input Services or both. • Formula based reversal – Provisional • and Final. • “Exempted Services” amended from 01.04.11. • Protection for exports, etc. • Easy option for Banks and Insurance.

VARIOUS CONDITIONS • Eligible Duties. • Manner of utilisation. • 50 % credit for Capital Goods. • “As such” removal. • Removal of used capital goods. • SAD credit. • Write off and amendments from 01.03.11. • Depreciation Vs Cenvat credit. • Refund of credit for Exports. • Documents. • Service tax credit – after payment. • Credit for Outward Freight – the story. • Supplementary Invoice – Excise / Service tax.

VARIOUS CONDITIONS • Job work – 180 days & exceptions. • Capital goods – ownership not relevant. • First Stage Dealer / Second Stage Dealer. • Interest – Ind Swift Laboratories.

COURTS ON CENVAT CREDIT • Plastic crates • Banco Products- 2009 (235) ELT 636 LB. • Input Services • Coca Cola – 2009 (242) ELT 168 Bom. • Ultratech – 2010 (260) ELT 369 Bom. • Structural items. • Vandana Global – 2010 (253) ELT 440 Tri LB.

Thank you mail@swamyassociates.com

![The CENVAT Credit Rules, 2004. [ Notification no. 23/2004-C.E. (NT) dated 10.09.2004]](https://cdn3.slideserve.com/6230112/the-cenvat-credit-rules-2004-notification-no-23-2004-c-e-nt-dated-10-09-2004-dt.jpg)