Download

1 / 57

600 likes | 1.65k Views

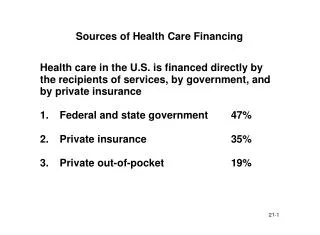

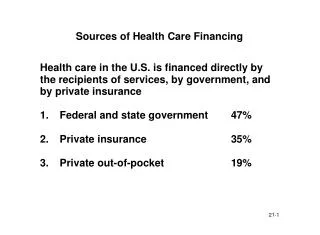

Sources of Health Care Financing. Health care in the U.S. is financed directly by the recipients of services, by government, and by private insurance 1. Federal and state government 47% 2. Private insurance 35% 3. Private out-of-pocket 19%. Coverage by Social Insurance Programs.

E N D

Sources of Health Care Financing • Health care in the U.S. is financed directly by the recipients of services, by government, and by private insurance • 1. Federal and state government 47% • 2. Private insurance 35% • 3. Private out-of-pocket 19%

Coverage by Social Insurance Programs • 1. Workers compensation pays medical expenses for work-related injuries. • 2. Federal Government is a major source of health care financing under two programs: • Medicare for persons over age 65. • Medicaid, a needs-based program for the poor.

Private Medical Expense Insurers • 1. Commercial insurance companies • 2. Blue Cross and Blue Shield • 3. Capitating health care providers • 4. Self insurers • corporate employers • Multiple Employer Trusts • MEWAs • 5. Federal CHAMPUS program

Distribution of Health-Insured Population • Percent of Population • Commercial Insurers 29.14% • Blue Cross/Blue Shield 24.94% • HMOs 22.45% • Self-Insured Plans 23.20% • Total Private Sector 68.96% • Medicare 14.16% • CHAMPUS 1.38% • Total Government 15.54% • Total Insured 84.50% • Uninsured 15.50% • Medicaid 13.94%

Extent of Medical Expense Coverage • 1. Most individuals under 65 (slightly less than two-thirds) are covered as employees or dependents under employer-sponsored medical expense plans. • 2. Where employer-sponsored coverage is not available, individual coverage may be purchased. • 3. Approximately 85% of Americans under age 65 were covered by private medical expense insurance in 1998.

Traditional Medical Expense Insurance Plans • GROUP MEDICAL EXPENSE INSURANCE • 1. Less than 10 million persons (under 5% of population) are insured under individually purchased medical expense insurance. • 2. Overwhelming dominance of group approach is due to • lower cost of group insurance • favorable tax treatment of employer-provided health insurance

Traditional Medical Expense Insurance Fee-For-Service Plans • Historically, commercial insurers and Blue Cross/Blue Shield organizations have provided fee-for-service benefits. • 1. insured sought services from a provider. • 2. insurance would pay some or all of the providers charge, directly or by reimbursing the insured. • 3. provider and insured agreed on the level of care and the insurer paid the bill.

Managed Care Plans • 1. Many experts argued that the fee-for-service approach provided an incentive to overutilize health care. • 2. Trend in recent years is away from traditional indemnity fee-for-service plans toward programs with a more direct relationship between the provider and the insurer. • 3. Newer approach includes HMOs, PPOs, and point-of-service plans. • 4. These programs are often referred to as managed care plans.

Traditional Fee-For-ServiceMedical Expense Insurance Plans • 1. Hospital expense coverage • 2. Surgical expense • 3. Physician’s expense coverage • 4. Major medical coverage

Hospitalization Insurance • 1. Hospital service benefit contracts • 2. Hospital reimbursement contracts • 3. Indemnity (cash payment) contracts

Surgical and Physician’s Expense Contracts • 1. Surgical service plans • 2. Surgical expense reimbursement contracts • 3. Physician’s expense reimbursement insurance

Major Medical Insurance • 1. High maximum (or unlimited) • 2. Deductible • 3. Coinsurance or share-loss provision

Major Medical With Base Plan $1,000,000 maximum Insurer pays 100% of costs up to maximum $10,000 Coinsured Layer of Coverage Insured pays 20% of Costs Insurer pays 80% of costs in excess of basic policies 80% of costs in excess of deductible on expenses not covered by basic $100 Corridor Deductible Basic hospitalization and surgical expense coverage (same or different insurer)

Comprehensive Major Medical $1,000,000 maximum Insurer pays 100% of costs up to maximum $10,000 Coinsured Layer of Coverage Insured pays 20% of Costs Insurer pays 80% of costs $250 per person/$500 family Deductible

Illustrated Payment Under Major Medical • Amount of loss $20,000 • Less deductible 250 • ______ • 19,750 • Insured pays 20% of expenseover deductible up to $10,000 $2,000 • Insurer pays balance $17,750

The Health Insurance Market Today • Although about 1,200 insurers that offer health insurance for medical expenses, traditional insurance plans no longer dominate the insurance market. • Many employers now offer health care coverage under alternative mechanisms. • 1. Health Maintenance Organizations • 2. Preferred Provider Organizations • 3. Point-of-Service Plans

GENERAL NATURE OF HMOs • Provide a wide range of comprehensive health care services to members in return for a fixed periodic payment. • Sponsored by a group of physicians, hospital, employer, labor union, consumer group, insurance company, or Blue Cross/Blue Shield plans. • HMO provides for the financing of health care and also delivers that care.

TYPES OF HMOs • Staff model • Group model • Individual practice association • Network model

Provider Sponsored Organizations • 1. Also sometimes called • Physician-Hospital Organizations (PHOs) • Integrated Delivery Systems (IDS’s) • 2. Similar to HMOs • PHO’s are paid a capitated fee • fee is divided among providers on a prenegotiated basis

Preferred Provider Organizations (PPO’s) • 1. Doctors or hospitals with whom employer or insurer contracts to provide medical services. • 2. Provider discounts services and sets up utilization control programs to control costs. • 3. Employees not required to use PPO, but if they go elsewhere they must pay more.

Point of Service Plans (POS) • 1. POS plans are the newest development in health insurance field. • 2. In one respect, POS plans operate like a PPO, since the employee retains right to use any provider but will pay a higher part of the cost for a provider outside network. • 3. At same time, POS is like an HMO, since care received through network is managed by primary care physician or “gatekeeper.” • 4. POS plans were created when HMOs allowed subscribers to use nonnetwork providers.

Cost Containment Provisions • In addition to managed care arrangements such as HMOs, PPOs, and POS plans, most traditional indemnity plans have adopted cost control provisions. • 1. Increased employee cost sharing • 2. Coordination of benefits • 3. Covering alternative sites of care • 4. Addressing utilization

Limited Health Insurance Contracts • Dread disease policies • Travel accident

Dental Expense Insurance • Written with a dollar reimbursement limit or on a service basis. • Coinsurance may require different cost-sharing in earlier years (e.g., 50% first year, 60% second year, 70% third year, 80% fourth year and 90% thereafter). • Coinsurance may also be structured to encourage or discourage utilization (100% for preventive care, 50% for orthodontics)

Prescription Drugs • Usually written on a group basis, as an adjunct to other coverage. • Reimbursement Basis Coverage • Generally a coinsurance or deductible. • Deductible per prescription or annual. • Service basis Coverage • Operates similar to the Blue Cross model. • Insurer payments directly to pharmacists. • Payment limited to the amount payable to a participating pharmacy.

Medical Savings Accounts • Medical savings accounts (MSAs) have been discussed for years and HIPAA-96 established an experimental MSA program: • 750,000 MSAs will be available to small business employees (50 or fewer employees) and self-employed individuals. • The MSA pilot program will end in the year 2000 or, if earlier, when the limit on the number of MSAs has been exceeded.

Medical Savings Accounts • Basic idea of the MSA is to allow individuals to make tax-sheltered contributions into a fund to be used to cover medical expenses. • Fund is used with a high deductible insurance policy and covers expenses within deductible. 1998 deductibles for the high-deductible policy • Individual coverage only $1,500 to $2,250 • Family coverage $3,000 to $4,500 • Amounts will be adjusted for inflation after 1998.

MSA Contributions • Generally, MSA contributions may be made by either the individual or his or her employer. • If made by an employer, MSA contributions are excluded from the employee's income. • If made by individual, contributions are deductible from income, subject to limits. • maximum limitation of 65% of the annual deductible for individual coverage and • 75% of the annual deductible for family coverage.

MSA Distributions • Distributions from an MSA that are used to pay for qualified medical expenses are not taxed to the MSA holder. • Distributions not used to medical expenses are taxable and subject to a 15% penalty. • Tax, but not penalty, for distributions received after MSA-holder becomes disabled, dies, or reaches Medicare eligibility.

Medicaid • Title XIX of the Social Security Act, known as Medicaid, is a federal-state program of medical assistance for needy persons that was enacted simultaneously with the Medicare program. • provides medical assistance to low income persons and certain needy persons who are not at the poverty level. • the federal government sets regulations and minimum standards. • federal share of cost is based on a formula tied to state per capita income and varied from 50% to 80% in 1998.

Medicaid Benefits • Medicaid benefits are quite comprehensive. • Benefits includes services traditionally included in a commercial group-health-insurance plan and some services, such as long-term care, that are not. • Mandatory benefits in all states include inpatient and outpatient hospital services, physician services, and home health care. • Optional services include outpatient prescription drugs, prosthetic devices and hearing aids, and dental services.

Child Health Assistance Program • BBA-97 introduced Child Health Assistance Program (Title XXI of the Social Security Act), from fiscal years 1998 through 2007. • New federal spending of $24 billion over 5 years for children’s health, with $48 billion for the initiative over the next 10 years. • Funding will allow states to provide health insurance coverage to poor uninsured children who do not qualify for Medicaid. • States can provide coverage by expanding Medicaid or under a State Children’s Health Insurance Program (or by a combination).

Buying Health Insurance • 1. When a noncontributory plan is provided by employer, no decision required by consumer, except perhaps a choice between traditional health insurance and a HMO. • 2. When and individual must choose, the primary emphasis should be on protecting against catastrophe losses.

Taxes and Health Care Costs • 1. Cost of employer-provided group plans is deductible by employer and nontaxable to the employee. • 2. For the individual, • health insurance premiums receive no special tax treatment. • premiums are combined with other health care costs and deductible to extent total exceeds 7.5% of AGI.

Health Insurance for Self-Employed • TRA-86 authorized self-employed persons to deduct 25% of cost of health insurance. The 25% later increased to 30% and then 40%. • TRA-97 phases in 100% deductibility. • Fiscal Year% Deductible • 1998-99 45% • 2000-01 50% • 2002 60% • 2003-2005 80% • 2006 90% • 2007 100%

The Health Insurance Problem • Access to health care • High cost of health care

The Access Problem • 40 million Americans have no health insurance coverage • Another 70 million are underinsured • Over 85% of the population with private insurance obtain coverage through employment

High Cost of Health Care • 1. Medical care costs growing faster than the average cost of living • 2. Consuming an increasing share of GNP • 1950 4.4% of GNP • 1998 13.+% of GNP

Some Causes of High Cost of Health Care and Health Insurance • Aging population • Improved (high-cost) medical technology • Excessive capacity • Defensive medicine • Insurance-encouraged utilization • Cost-shifting from government funded plans • Mandated benefits

Previous Attacks on the Problem • 1. State / federal legislation have addressed availability and to a lesser extent cost • COBRA • subsidized state health insurance pools • small-group reform • Oregon Medicaid experiment

COBRA • 1. Requires continuance of employer-sponsored group health insurance under specified circumstances. • 18 months for terminated employees. • 36 months for spouses of deceased, divorced or separated workers or dependent children whose eligibility for coverage ceases. • Generally, COBRA participant pays a premium based on the existing group rate.

Health Insurance Portability and Accountability Act of 1996 (HIPAA) • Health Insurance Portability and Accountability Act of 1996 (HIPAA) also known as Kassebaum-Kennedy, become effective on July 1, 1997. • Primary purpose of HIPAA-96 was to ensure the security of health insurance coverage for those that already have insurance. • HIPAA-96 was significant because, for the first time, minimum federal standards were applied nationally and to all plans, including self-insured plans.

HIPAA Reforms • HIPAA-96 imposed reforms on the • large group market (over 50 employees), • small group market (2 to 50 employees), and • individual market. • Reforms in the group market (both large and small) include • guaranteed renewability, • limitations on preexisting conditions, and • portability.

Small Group and Individual Market Reforms • In the small group market an insurer must provide all products on a guaranteed issue basis. • In the individual market, policies must be guaranteed renewable, as in the group market. • Individual market must provide access to health insurance to “eligible individuals.” An eligible individual is a person • who has at least 18 months prior health insurance coverage • most recent coverage being employer-provided and • no break in coverage lasting greater than 63 days.

Access for “Eligible Individuals” • HIPAA permits states to use one of two approaches to meeting the access requirement in the individual health insurance market. • Federal fallback approach applies if the states does nothing else. • Under federal fallback option, all insurers who operate in the individual market must offer eligible individuals at least two health plans. • Alternatively, a state may adopt an acceptable alternative mechanism, such as a high-risk pool or other mechanism to guarantee access.

Absence of Rating Reforms • Federal fallback standards contained no rating reforms. • Critics pointed out that access at an unlimited premium is not really access. • In response, Senator Edward Kennedy proposed legislation that would cap premiums to eligible individuals at 150% of the standard premium. • State small group reform programs and high risk pools that predated HIPAA include limits on rating and subsidized coverage.

HIPAA and Federal Regulation • A major development in HIPAA is the possibility of federal regulation of a state’s health insurance market. • If a state does not enact legislation to enforce federal standards, the Department of HHS performs the enforcement function. • Five states (California, Massachusetts, Michigan, Missouri, and Rhode Island) failed to comply and HHS now actively regulates insurance plans in those states.

State Efforts to Increase Access • Prior to the enactment of HIPAA, many states had addressed the problem of access to health insurance by: • establishing subsidized state health insurance pools for the uninsurable. • enacting small group reforms. • Unlike HIPAA, these state initiatives addressed the issue of cost.

Subsidized State Health Insurance Pools • 1. Individuals not eligible for Medicare or Medicaid and who cannot obtain insurance in conventional market may obtain coverage from state pools, usually at a subsidized rate. • 2. Pools provide comprehensive coverage including in-hospital services, skilled nursing facility care, and prescription drugs. • 3. The pools are subsidized, but even with the subsidy, premiums range from 125 to 200 percent of the state’s average premiums. • 4. By 1998, 30 states had created such pools. • 5. Costs in excess of premiums are covered by a subsidy, in most states from health insurers.

Small Group Reform • Prior to HIPAA, many states had passed small-group reform to improve availability of health coverage to small businesses and employees. • Typically, laws require insurers to offer plans to small groups on a guaranteed issue basis. • Insurer may not exclude individual employees and may exclude preexisting conditions only for a limited period. • If preexisting conditions requirement in one plan is met, coverage must be portable without a new preexisting conditions requirement. • Rules limit rates and annual rate increases.