Download

1 / 38

470 likes | 978 Views

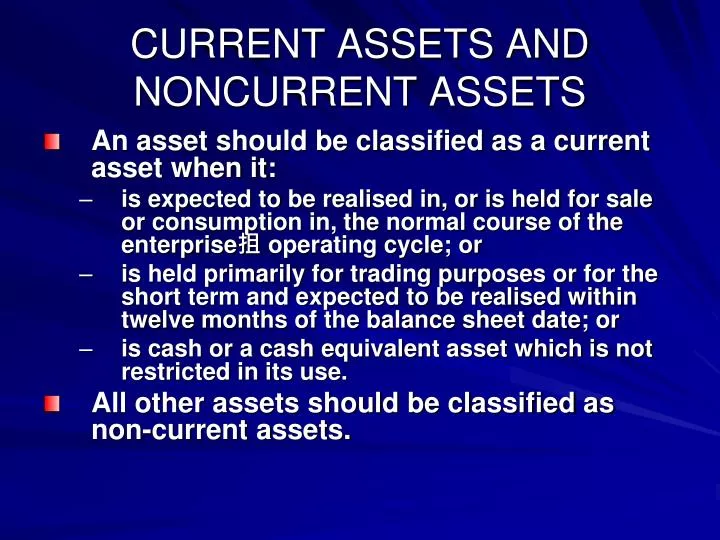

CURRENT ASSETS AND NONCURRENT ASSETS. An asset should be classified as a current asset when it: is expected to be realised in, or is held for sale or consumption in, the normal course of the enterprise抯 operating cycle; or

E N D

CURRENT ASSETS AND NONCURRENT ASSETS • An asset should be classified as a current asset when it: • is expected to be realised in, or is held for sale or consumption in, the normal course of the enterprise抯 operating cycle; or • is held primarily for trading purposes or for the short term and expected to be realised within twelve months of the balance sheet date; or • is cash or a cash equivalent asset which is not restricted in its use. • All other assets should be classified as non-current assets.

Non Current Assets • Include tangible and intangible, operating and financial asset of a long term nature. Consists of: • Plant Property and Equipment • Intangible assets • Financial assets (other than investments, trade and other receivables and cash as cash equivalents) • Long term investments /marketable securities (if they are not expected to be realised within 12 months of balance sheet date)

Plant, Property and Equipment Definition Recognition Initial cost Subsequent cost Depreciation Definition Misconceptions of Depreciation Depreciation Methods Disposal of PPE

Definition of PPE (MASB 15) • PPE are tangible items that : • A) are held for use in the • (i) production or • (ii) supply of goods or services, for • (iii) rental to others , or • (iv) for administrative purposes; and • B) are expected to be used during more than one period

Recognition of PPE • Cost of PPE shall be recognised as an asset if and only if: • It is probable that future economic benefits associated with the item will flow to the entity; and • The cost of the item can be measured reliably

Measurement: Initial costs of PPE • At recognition, an item of PPE that qualifies for recognition as an asset shall be measured at its costs • Elements of costs: • Asset dismantlement, removal and restoration costs are included as cost of PPE

Acquisition Cost of PPE • The cost of any PPE is the total cost of the asset at the point it is ready for use. • Cost include the purchase of the asset and those expenses needed to put it into working order

Acquisition Cost of PPE • May include the following: • Purchase price of the asset • Transportation cost to get the asset to the purchase’s premises • Insurance on the purchase of the asset • Taxes on the purchase of the asset • Installation costs

Revenue expenditure versusCapital expenditure • Capital expenditure • Acquisition cost of fixed asset/ expenditure to acquire fixed asset • Cost incurred to increase the operating efficiency, productive capacity or useful life of PPE/plant asset (also known as additions and improvements) • Will be reported as asset (noncurrent asset) in Balance Sheet

Revenue expenditure versusCapital expenditure (cont’d) • Revenue expenditure • Expenditure on the day to day running cost of the business • Cost of ordinary repairs incurred to maintain the operating efficiency and productive life of the • Reported as operating expenses in Income statement e.g repair and maintenance expesnes, wages, utilities

Recognition of Subsequent costs • Replacement or new addition: recognised as PPE if the recognition criteria is satisfied • Cost of day to day : servicing of PPE are expenditures often described as “repairs and maintenance and are recognised in profit & loss account as incurred • Major inspection • Major cost of inspection performed is recognised as replacement if satisfy recognition criteria (e.g Fire Engine)

Depreciation • The systematic allocation of the depreciable amount of an asset over its useful life. • Relevant principle: Matching principle

Depreciable assets • Depreciable assets are assets which: • are expected to be used during more than one accounting period; • have a limited useful life; and • are held by an enterprise for use in the production or supply of goods and services, for rental to others, or for administrative purposes.

Factors affecting useful life of depreciable assets • Expected physical wear and tear • Obsolescence (keusangan)- may be due to technological changes or change in market demand • Legal or other limits on the use of assets (expiry dates of related leases) • Useful life of a depreciable assets may be shorter than its physical life

Depreciation Methods • Straight line method • Reducing (declining) balance method • Sum of years digits • Production units method • Production hours method

Straight Line Method Annual depreciation expense = Original Cost – Expected salvage value Expected Economic Life Residual value The net amount which an entity expects to obtain for an asset at the end of its useful life after deducting the expected costs of disposal.

Reducing Balance Method A uniform rate of depreciation is applied each period to the cost of the asset reduced by accumulated depreciation Advantages: Suitable for use where the service rendered by the asset is greatest in the early years (in case of motor vehicles and machinery) Depreciation charge is lower as asset becomes older and there is likelihood of higher maintenance costs.

Reducing Balance Method Depreciation for the period = rate of depreciation x diminished balance Diminished balance = original cost - accum. depreciation

Illustration of Reducing Balance Method • A motor vehicle is bought on July 1 for RM30,000 and has an estimated residual value of RM12,000. the depreciation rate is 20% of the diminishing balance. Calculate the amount of depreciation or 4 years, after which time it is company policy that the vehicle be sold.

Sum of years digit • Depreciation charges will reduce by a constant amount each period • Also known as accelerated method • Advantages: • Suitable for use where the service rendered by the asset is greatest in the early years of its life • The depreciation charge is lower as the asset become older • Easy to calculate and write off the exact amount of depreciation required to leave the estimated residual value.

Sum of the digits method Calculate sum to be depreciated Calculate the sum of the digits in the estimated life of the asset Depreciation = (cost – residual value) x number of years lf life remaining sum of digits

Illustration of sum of digits method • A motor vehicle costing RM30,000 was purchased on July 1 2000.Registration and insurance amounting to RM1,350 were paid. The estimated useful life of the vehicle is fours years and the estimated residual value is RM12,000

Disposal of Plant Property and Equipment • An item of PPE should be eliminated from the balance sheet on disposal or when the asset is permanently withdrawn from use and no future economic benefits are expected from its disposal • Gains or losses arising fro retirement or disposal of an item of PPE should be determined as the difference between the estimated net disposal proceeds and the carrying amount of the assets and should be recognised as income or expense in the income statement

Sale of Disposal of depreciable asset Discarding of Depreciable asset Sale of Depreciable Fixed asset Trade in of a Fixed asset

Discarding of Depreciable Assets Journal entries:

Illustration • Assume that a machinery was purchased at RM30,000 and that the accumulated depreciation at the time of discarding of the machinery was RM28,000. Net book value at that time is RM2,000.

Sale of depreciable fixed asset • Suppose that a machine was purchased on 1st January 2003 for RM60,000. Sold on 31st December 2005 and a cheque for RM30,000 was received. Straight line method of depreciation was used. On 31st Dec. 2005, accumulated depreciation of the machine had a balance of RM24,000

Example :Disposal of asset • Assume that on 1 January 1995 Jingga Sdn Bhd purchased a machinery at an acquisition cost of RM65,000. The useful life is expected to be 6 years and the residual value is expected to be RM5,000. The depreciation method used is straight line. The machine was disposed on 30th June 2000.

Example :Disposal of asset • a. What is the annual depreciation charge? • b. What is the book value of the machinery as of 30th June? • c. Assume that the machinery was abandoned. Prepare the relevant journal entries to record the disposal of the machinery. • D. Assume that the machinery was sold for cash at a price of (i)RM12,000 and (ii) RM8,000. Prepare the relevant journal entries to record the sale of the machinery

Journal entries for (c ) Journal entries for d (i)

Trade in • Exchange of old asset with similar new asset • Trade in allowance given • Example: Old machinery trade in with new machinery. The price of the new machinery was RM 80,000. Trade in allowance given RM15,000. • Gain/loss on trade in : Book value –Trade in allowance

Trade in • Gain on trade in • =Book value (RM10,000) – Trade in allowance (RM15,000) • =RM5,000