Download

1 / 107

1.13k likes | 1.64k Views

第一章 策略成本管理概論 Introduction to strategy, cost management, and cost systems. 本章大綱. 1.1 現代管理會計的功能 1.2 財務會計、管理會計與成本會計之 比較 1.3 新製造環境與管理會計 1.4 成本效益之考量 1.5 企業組織結構與管理會計人員 1.6 會計專業組織與職業道德. Strategy and the Strategic Role of Cost Management.

E N D

第一章 策略成本管理概論 Introduction to strategy, cost management, and cost systems

本章大綱 1.1 現代管理會計的功能 1.2 財務會計、管理會計與成本會計之 比較 1.3 新製造環境與管理會計 1.4 成本效益之考量 1.5 企業組織結構與管理會計人員 1.6 會計專業組織與職業道德

Strategy and the Strategic Role of Cost Management • As a framework for the integration of strategy throughout this lecture, the Michael Porter model of competitive strategy is used. • This model explains that an organization succeeds either by pursuing a cost leadership strategy or a differentiation strategy. The cost leader succeeds by providing the lowest cost product or service to the consumer, while the differentiated organization succeeds by providing products and services with features, quality, and innovation that draw the consumer to these products and services.

The Five Steps for Strategic Decision Making • The first step is to determine the strategic issues surrounding the problem, because the solution of any problem must fit the organization’s strategy. A good decision is one that makes the organization more competitive and successful. By starting with the strategic issues, we ensure that the decision fits the organization’s strategic goals. • 1. Determine the Strategic Issues Surrounding the Problem. • Fuel costs are critical to Wal-Mart because it competes on low cost and low prices. So this problem will get close management attention. • 2. Identify the Alternative Actions: • In one alternative, Wal-Mart considers the use of smaller and more fuel-efficient trucks together with a relocation of its warehouses, to reduce travel time and fuel usage. Another option would be to outsource all of Wal-Mart’s delivery needs to other trucking firms.

The Five Steps for Strategic Decision Making • 3. Obtain Information and Conduct Analyses of the Alternatives • Wal-Mart collects relevant cost information and calculates the expected cost of each alternative and finds that the use of other truckers would provide significantly lower total fuel cost. Considering the problem strategically, Wal-Mart projects on the one hand that it can more effectively compete with Target by providing more rapid delivery of fast-moving items to its stores. On the other hand, Wal-Mart also knows that it competes on cost and that lower cost is critical to its success. • 4. Based on Strategy and Analysis, Choose and Implement the Desired Alternative • After considering the options, Wal-Mart chooses to outsource the delivery function to other trucking firms, in order to maintain or perhaps improve its low cost position. • 5. Provide an On-going Evaluation of the Effectiveness of implementation in Step 4. • To provide an on-going review of delivery costs, Wal-Mart top management instructs operational managers in the firm to present an updated review of the decision to top management once every quarter. In this way, changes in costs or strategic objectives will be reviewed on a regular basis.

Strategic Management and Strategic Cost Management • Overall, cost management's traditional role has changed to encompass a much more strategic emphasis. Changes is the business environment have made cost management much more critical to the firm's success, as well as more dynamic. Therefore, this lecture focuses on the strategic aspects of cost management, such as anticipating change, being more flexible, and thinking creatively. Along with this strategic focus has come a greater emphasis on cross-functional teams and cooperation among different members of an organization. • Strategic Focus on Cost Management: realizing, anticipating, and reacting to changes in the business environment, the modern cost manager is now more concerned with strategic thinking. Also, cost management has a greater focus on identifying costs and measures that a critical to the firm’s success. Generally speaking, the role of management accounting can be seen as having traveled through different phases, from a simple measurement and transaction-recording role, to more of a strategic business partner that helps identify and monitor a firm’s critical success factors (aspects of a firm’s performance that are essential to its competitive advantage and success).

Developing a Competitive Strategy: Strategic Positioning • 1. Cost Leadership. Cost leadership is a strategy in which a firm outperforms competitors in producing products or services at the lowest cost. The cost leader normally has a relatively large market share and tends to market segments by using the price advantage to attract a large portion of the broad market. Cost advantages usually result from productivity in the manufacturing process, in distribution, or in overall administration. • 2. Differentiation. The differentiation strategy is implemented by creating a perception among consumers that the product or service is unique in some important way, usually by being higher quality. This perception allows firms to charge higher prices and outperform the competition in profits without reducing costs significantly. • 3. Other Strategic Issues. While most firms will have a dominant strategy, recognize that many firms are likely to employee both of the strategies at the same time. However, a firm following both strategies is likely to succeed only if it achieves one of them significantly; otherwise, it could face the problem of “getting stuck in the middle.” A firm stuck in the middle is not able to sustain a competitive advantage. A common way for a firm to get stuck in the middle arises from its normal progression from one type of strategy to another.

The Contemporary Business Environment • Many of the changes in the role of cost management have been the result of changes in the current business environment. • 1. The Global Business Environment. • A key factor that drives the changes in the contemporary business environment is the growth of international markets and trade. The growing number of international organizations (NAFTA, EU, and WTO) as well as the increase in multinational alliances and firms indicates that significant opportunities for growth and profitability lie in international markets. The increasing competitiveness of the global business environment means that cost management information will continue to be an important tool in the struggle to remain competitive. • 2. Manufacturing and Information Technologies. • As a result of the new global focus, several new manufacturing and information technologies have been created (just-in-time, quality teams, statistical cost control, and speed-to-market). Another recent change has been the gradual increase in facilities costs relative to materials and labor costs; firms are now placing a greater emphasis of controlling large facilities costs than they have in the past.

The Contemporary Business Environment • 3. The New Economy: Use of Information Technology, the Internet, and E-Commerce. • These technologies have fostered the growing strategic focus of cost management by reducing the time required for record keeping and expanding the individual manager’s access to information within the firm, the industry, and the international business environment. • 4. Focus on the Customer. • As a result of an increased focus on consumer expectations regarding product use and quality, product life cycles have begun to shorten. This shortened life cycle forces companies to think in more strategic terms, as they begin to find their prior competitive advantages slipping away. Today many firms’ critical success factors are all customer related. Cost management information has also adapted by starting to provide more nonfinancial information regarding customer satisfaction and preferences.

The Contemporary Business Environment • 5. Management Organization. • In order to address this changing business environment more quickly and effectively, many firms have moved away from the traditional hierarchy of organization structure. Many firms are now promoting a more flexible structure and more cross-functional interaction, in order to meet consumers changing demands. • 6. Social, Political, and Cultural Considerations. • While changes in culture and politics vary between countries, there have been some distinguishable trends. Specifically, they include a more diverse workforce, a greater sense of ethical responsibility, and an increased deregulation. Overall, the changing business environment has forced companies to think in broader terms, focusing beyond the production of its product or service, and more on the global consumer and society as a whole.

1.1 現代管理會計的功能 規劃(Planning)的功能 組織(Organizing)的功能 決策(Decision making)的功能 控制(Controlling) 的功能 激勵(Motivating)的功能

The Four Functions of Management • The cost accountant fills several different roles, as well as provides a wealth of knowledge to the CFO and other company managers. • a. Strategic Management. Strategic Management is the development if a sustainable competitive position in which the firm’s competitive advantage provides continued success. In order to accomplish this goal, the management account must implement a strategy, or a set of goals and specific actions plans that provide the desired competitive advantage. • b. Planning and Decision Making. The management accountant is also responsible for budgeting and profit planning, cash flow management, and decisions relating to the firm’s operations. • c. Management and Operational Control. These responsibilities included managing and monitoring the actions of employees. Specifically, management control refers to upper-level employees evaluating mid-level employees, while operational control is used when operating-level employees are monitored by mid-level employees. • d. Preparation of Financial Statements. The management accountant must also prepare financial statements, which must comply with reporting requirements of different external groups and agencies. Because of their relevant information, financial statements can also be used in any of the other management functions.

1.3 新製造環境與成本會計(1/3) 新產業結構下之成本會計 高科技生產技術下之成本會計 及時化 (Just-in-time) 系統下之成本會計 作業基礎成本制 (Activity-based costing)與作業基礎管理 (Activity-based management)

1.3 新製造環境與成本會計(2/3) 全面品質管理 (Total Quality management (TQM)) 標竿制度 (Benchmarking) 平衡計分卡與策略地圖 (Balanced scorecard and Strategy Map) 委外代工 (Outsourcing) 16

1.3 新製造環境與成本會計(3/3) The Value Chain Business Intelligence (BI) (also called business analytics or predictive analytics) Target Costing: Target costing determines the desired cost for a product on the basis of a given competitive price so that the product will earn a desired profit. Life Cycle Costing Business Process Improvement The Theory of Constraints (TOC) Enterprise Risk Management Sustainability: Sustainability means the balancing of the organization’s short and long term goals in all three dimensions of performance – social, environmental, and financial. 17

及時化下的成本會計 Just In Time (JIT) 需求拉動生產 持續性改進 零存貨、零瑕疵 消除浪費 及時反應市場需求

作業基礎成本制 Activity-Based Costing (ABC) 自動化、彈性製造系統下 從各作業的資源投入,透過成本動因(Cost Driver),將成本正確的分攤到產品上

標竿制度係指藉由標竿(benchmark)的確認及設定,來進行成本控制及提昇作業效率的一種管理程序標竿制度係指藉由標竿(benchmark)的確認及設定,來進行成本控制及提昇作業效率的一種管理程序 如產品成本標竿之設定、存貨之管理,以及應收帳款之催收等等作業 標竿制度 (Benchmarking)

平衡式計分卡(Balanced scorecard) 平衡式計分卡乃是彙整表達企業用以衡量其經營績效之指標的一種管理會計報告 其內含之績效指標係根據企業經營策略及目標,分別由財務、顧客、內部流程及學習成長等四個構面所組成 這些績效指標兼顧財務性與非財務性,以及內部性與外部性績效之衡量及報導,故以「平衡式」名之,惟實際上之運用,並非各構面指標之「相對權數」均相等,而是隨著企業處境的變動不斷加以調整

委外代工(Outsourcing) 委外代工或稱外包,係指將產品的設計、製造或勞務提供之某些程序委託外面的協力廠商、團體或是個人代為處理的一種生產方式。委外代工的主要考量在於成本抑減

1.4 成本效益之考量 管理需要資訊,資訊之取得必須支付相對的代價,此代價即為資訊之取得成本,其高低往往取決於所需資訊內涵之多寡及品質 隨策略方案的性質而異,我們卻可以透過成本效益分析來尋求解決 例如,某公司在決定應否花費鉅資建立一套新的成本會計制度時,經過成本效益之考量,如果管理當局認為這套制度能夠提昇成本控制成效,並使節省下來的支出超過其成本,則此一新制度即值得建立

1.5 企業組織的結構與管理會計人員 企業組織結構 依部門職能區分 依營業區域分 依產能(服務項目)類別分 直線與幕僚之職能 會計長、財務長與內部稽核

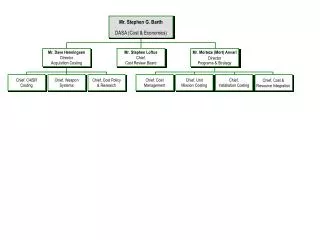

總裁 生產部副總裁 行銷部副總裁 財務部副總裁 工廠廠長 內銷部 外銷部 會計長 財務長 機械課 裝配課 成本控制 內部稽核 會計資訊系統 圖1-2:某製造業之部份組織系統圖 企業組織結構

會計長 財務長 內部稽核 • 有提出對外及對內的相關會計報表之責任 • 提供管理階層執行規劃、控制、評估績效、以及制定決策所須之會計資料,並監督企業之內部控制制度 • 管理公司的現金、有價證券、授信及帳款催收等事項。財務長必須經常與金融機構打交道,同時也要多注意該公司股票(及債券)之市場價格的動態 • 提供各種內部稽核及諮詢服務,包括稽核內部控制制度及提供管理用途之成本資訊,並協助外界之會計師審核其對外發布之財務報表

1.6 會計專業組織與職業道德 成本管理的專業環境(The Professional Environment of Cost Management) Internal Revenue Service (IRS) Federal Trade Commission (FTC) Securities and Exchange Commission (SEC) Cost Accounting Standards Board’s (CASB) 美國會計師協會(American Institute of Certificated Public Accountants,簡稱AICPA) Public Company Accounting Oversight Board (PCAOB) (July 2002) 管理會計師協會(Institute of Management Accountants,簡稱IMA) 內部稽核師協會(Institute of Internal Auditors,簡稱IIA)

職業道德 能力 保密 正直 客觀

能 力 (適 任) 持續充實本身之知識與技能,以維持適任的專業能力 配合相關法規及技術準則,以履行專業職責 在適切分析攸關與可信的資訊後,編製完整且清晰的報告與建議

保 密 拒絕揭露在工作過程中所獲悉的機密資訊,但得到授權或法律另有規定者不在此限 告知所屬人員保守工作過程中所獲悉的機密,並監督他們的行動,以確保資訊的機密性 避免使用由工作中所獲悉的機密資訊,向其他個人或第三者,換取不道德或非法的利益

正 直(1/2) 避免實質或明顯的利益衝突,並知會任何具潛在衝突之團體 避免參與任何會損及職業道德之所有活動 拒絕任何會影響或可能影響其行為之禮物、利益或招待 避免主動或被動地破壞組織達成合法或道德目標之情事

正 直(2/2) • 應對會妨礙公正判斷或有效執行活動之專業限制或其他限制進行瞭解並溝通 • 應公布有利或不利的資訊,以及專業之判斷或意見 • 應避免從事或支持任何會破壞專業形象之活動

客觀 公正且客觀地表達資訊 充分揭露預期會影響使用者對報告、意見及建議事項之理解的攸關資訊

第二章 成本觀念與習性分析

本章大綱 2.1 介紹成本的觀念 2.2 探討產品成本與期間成本 2.3 討論管理上經常使用之成本類別 2.4 說明成本的習性及分析成本習性時 之主要假設 2.5 探討混合成本分析 2.6 介紹貢獻式損益表 附錄 介紹迴歸分析及相關分析

成本標的(cost object) 成本標的之辨認及選擇,是成本會計最基本的工作要項 管理人員為了決策之需,必須知悉某事物(object)的成本 會計人員將此「某事物」稱之為成本標的,泛指用來衡量、累積及報導成本的任何單位、作業或活動 成本標的即成本歸屬的終點 例如:一種產品、一項服務、一位顧客、一張訂單、一紙合約、一個作業、或是一個部門等

成本累積(cost accumulation) 指經由成本會計制度,以有系統的方式蒐集及彙總成本資料之過程

成本歸屬(cost assignment) 將所累積之實際成本歸屬至成本標的之程序 成本歸屬的方法 隨著成本與成本標的間之可追溯性的高低而不同 先依特定的成本標的將成本區分為直接成本與間接成本,而後再採行適當的方式將成本追溯(trace)或分攤(allocate)到成本標的 直接成本係指可按合理的經濟方法直接追溯至成本標的之成本 間接成本則是指無法按合理的經濟方法直接追溯,必須經由分攤程序分攤至成本標的之成本

成本累積或成本標的 成本累積 成本標的 成本歸屬 成本歸屬 部門甲 成本項目A 產品X 部門乙 成本項目B 作業丙 產品Y 作業丁 圖2-2 成本累積、成本歸屬與成本標的之關係

2.2 產品成本與期間成本 產品成本(product cost) 是指可以歸屬到最終產品之成本,如進貨成本或生產線員工薪資 產品出售後即轉為銷貨成本(cost of goods sold) 未售出部份則予以遞延列為存貨 期間成本(period cost)係指與產品生產活動較無關聯,但比較容易歸屬於某特定會計期間之成本 應列為綜合損益表之營業費用項目,例如辦公室租金及保險費、銷售人員薪資,以及廣告費等

買賣業之產品成本 買賣業者之產品成本,除了進貨價格之外,還包括相關的運費、保險稅捐及驗收成本等等。舉例而言,基隆服飾店本月份購進學生制服100套,總價為$100,000,運費$5,000,運送保險費$3,000,則其產品(學生制服)成本可計算如下: 制服之總價 $100,000 制服運費 5,000 運送保險費 3,000 總 成 本 $108,000 單位成本(每套制服) $1,080

製造業之產品成本 製造成本(manufacturing cost)或 生產成本(production cost) 直接原料成本(direct material cost) 直接人工成本(direct labor cost) 製造費用(manufacturing overhead)

製造成本 直接 人工 直接原料 製造費用

原料成本 直接原料成本(direct material cost) 或稱原料成本(raw material cost),乃構成成本標的(如製成品)之主要部份,且可直接計入成本標的(如產品)之所有原料的成本 間接原料成本(indirect material cost) 為製造費用的一部分 如黏合桌子用的膠劑,為產品成本的一部份,基於成本效益之考量,將之歸為間接原料

人工成本 直接人工成本(direct labor cost) 指將直接原料轉變為製成品所耗用,且易於直接歸屬到成本標的(如產品)的人力資源成本。 如汽車廠內機器操作員及裝配線工人的工資,及其員工之福利(fringe benefits)支出,如保險費、退休金及休假給付等等,均為直接人工成本。 間接人工成本(indirect labor cost) 為製造費用的一部分 如加班津貼通常計入製造費用,因為加班大多導因於生產排程的更動

製造費用(manufacturing overhead) 廠房費用(factory overhead) 間接製造成本 (indirect manufacturing cost) 廠房負擔(factory burden) 由於製造費用無法直接歸屬到最終產品,必須經過某些程序進行分攤 如動力費可按機器小時數分攤到各產品

製造成本 直接材料 主要成本 直接材料 直接人工 加工(轉換)成本 製造費用 製造費用 產品成本