Download

1 / 73

760 likes | 944 Views

2. Product Costing Systems: Concepts and Design Issues. Learning Objective 1. The Meaning of Cost. The use of valuable resources, in order to achieve a stated purpose. In accounting, cost is reported in monetary terms. Product Costs

E N D

2 Product Costing Systems: Concepts and Design Issues

The Meaning of Cost The use of valuable resources, in order to achieve a stated purpose. In accounting, cost is reported in monetary terms. • Product Costs • Related to the purchase or manufacture of goods for resale. • Assigned to inventory and cost of goods sold. • Period Costs • Related to selling and administrative operations. • Recognized as expenses in the same time period.

Retailers . . . Buy finished goods. Sell finished goods. Manufacturers . . . Buy raw materials. Produce and sell finished goods. MegaLoMart Comparing Service, Retail and Manufacturing Companies Service firms . . . Provide a service that is consumed when produced. Have no inventories.

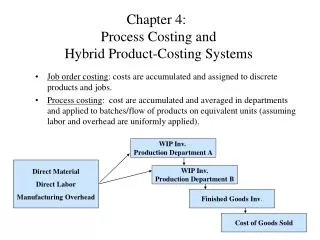

Manufacturing Companies The 3 major categories of manufacturing costs: Direct Materials Raw materials, components, and other parts that can be traced to a specific product. Direct Labor Payments and benefits for those employees who convert direct materials into finished product. Manufacturing Overhead Indirect material Indirect labor Other overhead

Manufacturing Companies Prime Costs include: Direct Materials Direct Labor Manufacturing Overhead

Manufacturing Companies Conversion Costs include: Direct Materials Direct Labor Manufacturing Overhead

Stages of Production and the Flow of Costs - Example Axel Electronics makes toasters. On February 1, Axel has $15,000 of raw material on hand. Axel’s purchase and transfers to the production floor are indicated below. What is Ending Inventory in February?

Stages of Production and the Flow of Costs - Example Axel Electronics makes toasters. On February 1, Axel has $15,000 of raw material on hand. Axel’s purchase and transfers to the production floor are indicated below. Now let’s look at Work-in-Process.

Stages of Production and the Flow of Costs - Example On February 1, Axel had WIP of $30,000 on the factory floor. During February, Axel paid $92,000 in direct labor wages. Overhead is applied at 150% of direct labor. On 2/28, $22,000 is still in WIP. What is the amount of cost transferred to Finished Goods in February?

150 % of $92,000 Stages of Production and the Flow of Costs - Example On February 1, Axel had WIP of $30,000 on the factory floor. During February, Axel paid $92,000 in direct labor wages. Overhead is applied at 150% of direct labor. On 2/28, $22,000 is still in WIP. Now let’s look at Finished Goods. Transferred to Finished Goods

Stages of Production and the Flow of Costs - Example On February 1, Axel had Finished Goods of $125,000 on hand. At the end of February, a physical inventory count revealed $96,000 in Finished Goods still on hand. What was Cost of Goods Sold for February?

Cost of goods sold Stages of Production and the Flow of Costs - Example On February 1, Axel had Finished Goods of $125,000 on hand. At the end of February, a physical inventory count revealed $96,000 in Finished Goods still on hand. What was Cost of Goods Sold for February?

Let’s look at aSchedule of Cost ofGoods Manufactured forCollegePak Company. Schedule of Cost of Goods Manufactured

Schedule of Cost of Goods Manufactured Include all direct labor costs incurred during the current period.

Schedule of Cost of Goods Manufactured Beginning work-in-process inventoryis carried over from the prior period.

Schedule of Cost of Goods Manufactured Ending work-in-process inventory contains the cost of unfinished goods, and is reported in the current assets section of the balance sheet.

Now let’s look at an income statement for CollegePak. Income Statement for a Manufacturer

Production Costs in the Service Sector • A service provider cannot “inventory” its services. • The costs of providing the service can be identified and measured, just as occurs in manufacturing industries. • Managing and tracking the costs associated with value-chain activities can point to opportunities for improvement.

Cost Drivers An “activity” is any discrete task that an organization undertakes to make or deliver a good or service. Number ofcomputers made byDell in a day Number offlights by SouthwestAirlines in a given market A “cost driver” is some characteristic of the activity that causes costs to be incurred.

Cost Behavior Cost behavior means how a cost will react to changes in the level of business activity. • Totalvariable costschange when activity level changes. • Totalfixed costsremain unchanged when activity level changes.

Total Variable Cost Example Your total long distance telephone billis based on how many minutes you talk. Total Long DistanceTelephone Bill Minutes Talked

Variable Cost Per Unit Example The cost per long distance minute talked is constant. For example, 5 cents per minute. Per MinuteTelephone Charge Minutes Talked

Total Fixed Cost Example Your monthly basic telephone bill probably does not change when you make more local calls. Monthly Basic Telephone Bill Number of Local Calls

Fixed Cost Per Unit Example The average cost per local calldecreases as more local calls are made. Monthly Basic Telephone Bill per Local Call Number of Local Calls

Cost Hierarchy Directly traceable to the decision to produce the level of output Unit-level Costs Costs that are incurred for every unit of product manufactured or service produced. Includes direct material, direct labor, utilities to run equipment, other overhead directly related to the production process. All unit level costs are variable, but notall variable costs are unit level costs.

Cost Hierarchy Batch-level Costs Costs that are incurred for batch of product manufactured or service produced. Includes setup costs, material-handling costs related to delivering raw material to the production line, etc.

Cost Hierarchy Product-level Costs Costs that are incurred for each line of product or service. Includes design costs for product lines and marketing costs for each product line.

Cost Hierarchy Facility-level Costs Costs that are incurred to maintain the organization’s overall facility and infrastructure. Includes production manager’s salary, plant depreciation, and insurance on the facility and equipment.

Committed and Discretionary Costs Committed Long-term obligations, difficult to change in the short term. Discretionary Easier to alter in the short term by current managerial decisions. Rental and/or Lease Financing of Buildings and equipment Advertising and Research and Development

Opportunity Costs The potential benefit that is given up whenone alternative is selected over another. If you were not attendingcollege, you could beearning $20,000 per year.Youropportunity costofattending college forone year is $20,000.

Sunk Costs Past payments for resources that cannot be changed by any current or future decision. Sunk costs should not be considered in decisions. Example:You bought an automobile for $12,000 two years ago. Whatever you do with the automobile in the future, you cannot nullify the original transaction. If it has a trade-in value, that value would become an opportunity cost in your future decisions.

Direct Costs Costs that can betraced easily and conveniently to a product or department. Example: Cost of paint in the paint department of an automobile assembly plant. Indirect Costs Costs that need to be allocated, before they can be assigned to a product or department. Example: Cost of national advertising for an airline is indirect to a given flight or route. Traceability of Resources

Product Absorption (Full) Costing A system of accounting for costs in which both fixed and variable production costs are included in product costs. Fixed Costs Variable Costs

Variable Costing A system of cost accounting that assigns only the variable cost of production to products. Fixed Costs Product Variable Costs

Absorption and Variable Costing Let’s see what we can learn about the differences between absorption and variable costing by looking at a numerical example.

Howell, Inc. produces a single product with a sales price of $40 and the following cost information: Absorption Costing vs. Variable Costing - Example