Download

1 / 11

190 likes | 347 Views

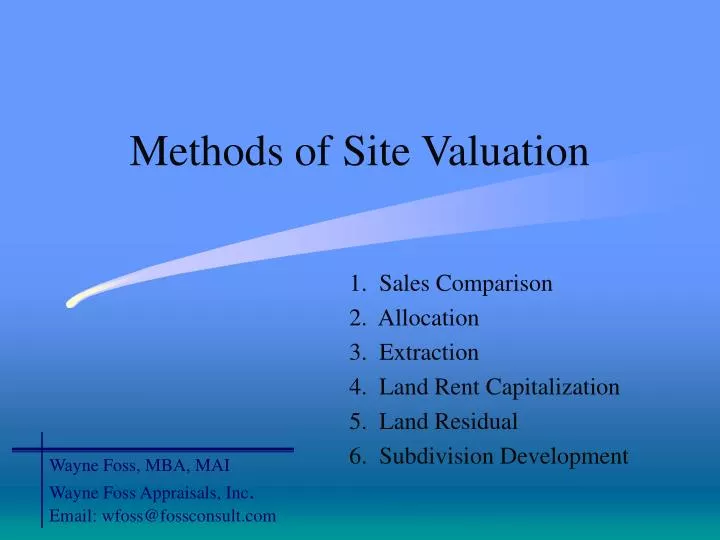

Methods of Site Valuation. 1. Sales Comparison 2. Allocation 3. Extraction 4. Land Rent Capitalization 5. Land Residual 6. Subdivision Development. Wayne Foss, MBA, MAI Wayne Foss Appraisals, Inc . Email: wfoss@fossconsult.com. Underlying ideas.

E N D

Methods of Site Valuation 1. Sales Comparison 2. Allocation 3. Extraction 4. Land Rent Capitalization 5. Land Residual 6. Subdivision Development Wayne Foss, MBA, MAI Wayne Foss Appraisals, Inc. Email: wfoss@fossconsult.com

Underlying ideas • Site is valued as though vacant and ready for its legal optimum, of highest and best, use • Appraisal techniques, numbers and formulas may be used to provide a foundation for judgement; but never a substitute for judgement • The market decides how much a site is worth or market value; “The market talks and the appraiser listens!”

1. Sales Comparison Approach • Based on idea that value is indicated by actual sales prices of similar sites. • Accomplished by comparing the appraised site to other similar, competitive, comparable sites which have recently sold. • Comparison adjustments are made to the price for differences; • positive (+) when subject is superior • negative (-) when subject is inferior

2. Allocation (%) • Investigate market standard ratio; what % that site represents of the total price • Example: from the market typically find: • Total Property 100% • less (-) improvements 80% • equal (=) site 20% • Then apply the site % to the total property values typical of subject type and location to find estimated contribution of the site.

3. Extraction • Estimate of site value based on deducting the estimated contribution of improvements from total property sales prices • Example: from the market typically find: • Sale of Similar property $10,000 • less (-) improvements contribution 6,000 • equal (=) site contribution $ 4,000 • This is done for several properties similar to subject situation to provide the site value estimate.

4. Land Rent Capitalization • Used when a property is producing fair market income under a ‘land lease’ and a market capitalization rate can be derived from the market (sales of land leased at time of sale) • Example: subject is under land lease with fair market rent: • Annual Income to owner after all expenses (such as insurance and real property tax): $10,000 • Capitalization Rate (RL) from market: 10% • Indicated Land Value = I/R or: $10,000 0.10 = $100,000

5. Land Residual • Used when a total property total market net income is known or estimated, and land and building capitalization rates may be found in the market. • For example: if we find a 2% recapture, or “return of” rate and 8% “return on” investment in the market, and … • Net Operating Income: $100,000 • Less income to the Building: 35,000 (if building value $350,000 x 10% bldg. capn’ rate(RB)) • Residual to the land: $ 65,000 • Land Value: (V=I/RL); $65,000 0.08 = $812,500

6. Subdivision Development • Used for land with near-term subdivision potential. Finding how much a developer would pay for the land considering potential revenue from development, less allowance for direct and indirect outlays, profit, and time delay. • Example: (oversimplified) • Revenue: 100 lots @ $5,000 = $500,000 • Less Development expense & Profit incentive: $400,000 • Net to the Land: $100,000 • Present worth @ xx% for # years: $ 65,000 • Note: time delay & profit must be included! • General layout is a discounted cash flow analysis

Key Points: • A site is valued as though vacant and ready for its highest and best use, or legal optimum use. • Sales Comparison approach is normally preferred; it works best if there is sufficient recent comparable sales data • Sales should be similar location, size, financing, amenities, AND have the same highest and best use as the subject. • Data should always be confirmed to find motivations, financing impact, and other details.

Key Points, continued ... • Comparison adjustment amounts must be from market information • Selection of unit-of-comparison must be based on market standards • Formulas and tables to adjust for items such as corner influence and depth are usually too abstract and simply don’t relate sufficiently to use. • Appraisal techniques provide a basis, not a substitute, for judgement in the final conclusion.

There are several ways to estimate the market value of a site as though vacant Are there any Questions? Wayne Foss, MBA, MAI, Fullerton, CA USA Phone: (714) 871-3585 Fax: (714) 871-8123 Email: wfoss@fossconsult.com