Download

1 / 75

750 likes | 1.06k Views

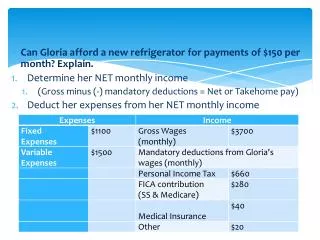

Can Gloria afford a new refrigerator for payments of $150 per month? Explain. Determine her NET monthly income (Gross minus (-) mandatory deductions = Net or Takehome pay) Deduct her expenses from her NET monthly income. Can Gloria afford a new refrigerator for payments of $150 per month?

E N D

Can Gloria afford a new refrigerator for payments of $150 per month? Explain. • Determine her NET monthly income • (Gross minus (-) mandatory deductions = Net or Takehome pay) • Deduct her expenses from her NET monthly income

Can Gloria afford a new refrigerator for payments of $150 per month? Determine her NET monthly income (Gross-mandatory deductions) $3700-$660-$280-$40-$20= $2700 Deduct her expenses from her NET monthly income $2700-1100-1500 = $100 YES, She can afford the fridge if she reduces her VARIABLE EXPENSES by $50

3 Fixed Expenses • Rent/mortgage • Car payment • ? • 3 Variable Expenses • Groceries • Entertainment • ?

Which one would you buy? • If you only have $3 to spend on breakfast, this is the RATIONAL DECISION • If you have $4 to spend on breakfast this is the RATIONAL DECISION because it is less expensive per ounce

Econ Unit3-Personal Finance Lesson 1: Rational Decision Making

Rational Decision Making - making consumer decisions based on opportunity cost and analyzing all possible solutions against ranked criteria Positive Incentive – something that motivates an individual Negative Incentive –discourages behavior

1. Individuals save their money in financial institutions. Savings helps individuals and the economy. 2. Financial institutions loan money to businesses. 4. More individuals have more money from wages and dividends. 3. Businesses use borrowed money to increase production, hire more workers, and pay more dividends.

Let P = $1,000 be an initial deposit into a savings account with annual interest rate of r = 0.05 (5%). What is the amount in the account after 1 year if the account (i) compounds annually, (ii) quarterly, (iii) monthly, (iv) weekly, (v) daily? Solution: (i) Compounded annually: $1,050.00 (ii) Compounded quarterly: $1,050.95 (iii) Compounded monthly: $1,051.16 (iv) Compounded weekly:$1,051.25 (v) Compounded daily:$1,051.27

Stocks • part ownership in a corporation • (high) you can lose everything if stock value drops • (high) no limit to how high stock values can go

Bonds • certificate from a company or the govt. in exchange for money • (low) company/govt. defaults on loan; you lose everything • (low) good chance you get your $$$ with small profit from interest

Mutual Funds • company pools $$$ for different investments • shorter term = higher risk • diversification ($$$ in many different areas)

Roth IRA • Individual Retirement Account. • You can put in $3,000/yr. • (low) can’t deduct contribution from taxes • (mid) interest is tax-free, no taxes when you use it after retirement.

Risk ManagementFIVE WAYS TO HANDLE RISK Avoid Risk: You risk losing money if you play the lottery. You can avoidthis risk by not buying lottery tickets. Retain Risk: You acceptthe risk of doing poorly on a test because you didn’t study. Reduce Risk: You risk developing lung cancer if you smoke cigarettes. You reducethis risk if you don’t smoke cigarettes. Transfer Risk: You risk embarrassing yourself if you give a presentation in front of the entire school. You transferthe risk by asking someone else to give the presentation. Share Risk: You risk making an unpopular choice if you select a DJ for the school dance by yourself. You sharethe risk if you ask others to join a committee to select the disc jockey.

a rise in prices over time OR a decrease in the value of $$$ Inflation is…

Causes for inflation too much money in the economy demand for goods and services exceeds existing supplies cost of producing goods and services rise and that cost gets passed on to the consumer through higher prices

Monetary v Fiscal Policy INFLATION IS CONTROLLED BY Monetary policy (Federal Reserve) = change in the rate of growth of the money supply to affect the amount of credit & the economy TAXES ARE CONTROLLED BY Fiscal Policy (Congress) = change in the amount of taxes and spending

Inflation is… Former Chairman of the Federal Reserve Alan Greenspan

Inflation is… Interest rate

Hyperinflation is… a situation where the price increases are so out of control that the concept of inflation is meaningless occurs when there is a large increase in the money supply not supported by gross domestic product (GDP) growth, resulting in an imbalance in the supply and demand for the money left unchecked this causes prices to increase, as the currency loses its value

Unanticipated Inflation • borrowers with fixed interest rate • people with COLA (Cost of Living Adjustment) income • speculators (lots of big loans) • lenders with fixed rate • retired with fixed income • business owners • savers (value drops) • consumers (costs rise) • borrowers w/ARM (Adjustable Rate Mortgage)

Progressive Tax a tax rate that increases as income increases (the wealthy pay a higher percentage of their earnings than people less financially well-off) US Federal Income Tax