Download

1 / 43

450 likes | 789 Views

Closing Balances and the Trial Balance. hink Corner. uiz Corner. What’s Inside ?. Learning Objectives. Balancing the account. Trial Balance. Balancing the account. Trial Balance. Learning Objectives. After reading this chapter, you will be able to:. .

E N D

Closing Balances and the Trial Balance

hink Corner uiz Corner What’s Inside ? Learning Objectives Balancing the account Trial Balance Balancing the account Trial Balance

Learning Objectives After reading this chapter, you will be able to: Close accounts at the end of a month. Close accounts at the end of a financial year. Prepare accounts using the running balance method. Prepare a trial balance and state its uses and disadvantages.

hink Corner nswer Up to this stage, all you see from the account is a list of entries. Take the bank account as an example, after entering ten debit entries and twenty credit entries in the account, do you know how much is left in the bank? No. We need to find the difference between the debit side and the credit side to see how much is left. This procedure is called closing the accounts and the difference is called the balance. There are two stages of account closing: 1. Month-end closing 2. Year-end closing

Month-end closing Firms need to monitor their accounts regularly to see if there is any problem. For example, owners need to know whether they have enough cash in the bank, whether debtors are slow making payments or whether they owe creditors too much. Because of the above reasons, firms usually close the accounts at the end of each _____. After closing the accounts, the owners know the ______ of each account and they can make decisions accordingly. month balance

Bank 20X7 $ 20X7 $ Nov 1 Capital 200,000 Nov 3 Motor vehicles 60,000 “ 25 Cash 30,000 “ 14 Rent 10,000 “ 22 Purchases 40,000 Month-end closing Take a bank account as an example. Shown below is how the account is closed at the end of a month: $110,000 $230,000 Add up the debit side and the credit side separately. Step 1 If the total of the debit side and the total of the credit side differ, the difference is the balance of the account. Step 2

Bank 20X7 $ 20X7 $ Nov 1 Capital 200,000 Nov 3 Motor vehicles 60,000 “ 25 Cash 30,000 “ 14 Rent 10,000 “ 22 Purchases 40,000 Month-end closing Take a bank account as an example. Shown below is how the account is closed at the end of a month: $110,000 $230,000 Difference between the debit side and the credit side = $230,000 –$110,000 = $120,000

Bank 20X7 $ 20X7 $ Nov 1 Capital 200,000 Nov 3 Motor vehicles 60,000 “ 25 Cash 30,000 “ 14 Rent 10,000 “ 22 Purchases 40,000 Month-end closing Take a bank account as an example. Shown below is how the account is closed at the end of a month: Closing balance “ 30 Balance c/d 120,000 Put this balance on the side with the smaller total. This closing balance is called the balance carried down (abbreviated as balance c/d). Step 3

Bank 20X7 $ 20X7 $ Nov 1 Capital 200,000 Nov 3 Motor vehicles 60,000 “ 25 Cash 30,000 “ 14 Rent 10,000 “ 22 Purchases 40,000 “ 30 Balance c/d 120,000 230,000 230,000 Month-end closing Take a bank account as an example. Shown below is how the account is closed at the end of a month: Enter the totals on both sides at the same level. Now the debit-side total equals the credit-side total. Step 4

Bank 20X7 $ 20X7 $ Nov 1 Capital 200,000 Nov 3 Motor vehicles 60,000 “ 25 Cash 30,000 “ 14 Rent 10,000 “ 22 Purchases 40,000 “ 30 Balance c/d 120,000 230,000 230,000 Month-end closing Take a bank account as an example. Shown below is how the account is closed at the end of a month: Opening balance Dec 1 Balance b/d 120,000 The closing balance of the current month is the opening balance of the next month. This is called the balance brought down (abbreviated as balance b/d). Step 5

Bank 20X7 $ 20X7 $ Nov 1 Capital 200,000 Nov 3 Motor vehicles 60,000 “ 25 Cash 30,000 “ 14 Rent 10,000 “ 22 Purchases 40,000 “ 30 Balance c/d 120,000 230,000 230,000 Dec 1 Balance b/d 120,000 Month-end closing Take a bank account as an example. Shown below is how the account is closed at the end of a month: The balance of $120,000 means that there is $120,000 left in the bank at the end of November. At the beginning of December, the bank account will start with $120,000.

Month-end closing From the above example, the balance c/d is on the credit side of the bank account. This means that the debit total is greater than the credit total. We call this balance a ___________. debit balance $ $ When the credit total is greater than the debit total, the balance c/d would be on the debit side. This is a ___________. credit balance $ $

Month-end closing When the debit total is equal to the credit total, there would be no balance c/d. This is a __________. zero balance $ $ Note: Assets and expenses accounts usually have debit balances. Capital, liabilities and revenues accounts usually have credit balances. Learning Objectives uiz Corner

Year-end closing At the end of a financial year, businesses will close the accounts and prepare the ___________, including the ____________________________ and the ___________. final accounts trading and profit and loss account balance sheet Final accounts Trading and profit and loss account Balance sheet This allows owners to find out whether there is a profit or loss. This allows owners to know the financial situation of the business.

Year-end closing The method of closing the accounts at the year end is the same as that for the month end, except that some accounts will be _____ at the year end and their balances will not be _____________ to the next financial year. closed carried forward ______, _______ and ______ accounts will still have their balances carried forward to the next accounting year, and their balances will also appear on the ___________. Assets liabilities capital balance sheet _______ and _______ accounts will be closed at the year end. Balances will not be carried forward to the next accounting period. They will be transferred to the ____________________________. Revenues expenses trading and profit and loss account

Year-end closing Year-end closing for revenues and expenses At the year end, the sales and purchases accounts will be closed and their balances will be transferred to the _____________, while other revenues and expenses accounts will be closed and their balances transferred to the __________________. trading account profit and loss account Example 1: JC Company’s financial year ended on 31 December 20X8. The sales account and the electricity account on that date would appear as:

Sales 20X8 $ 20X8 $ Dec 1 Balance b/f 150,000 Electricity 20X8 $ 20X8 $ Dec 1 Balance b/f 40,000 “ 21 Bank 20,000 60,000 60,000 Year-end closing Dec 31 Trading 150,000 Dec 31 Profit and loss 60,000 You can see that the only difference between month-end closing and year-end closing is that the balances in the revenues and expenses accounts at the year end are ___ carried forward to the next period but are transferred to the ____________ or the ___________________. not trading account profit and loss account Learning Objectives

Sally Tong 20X7 $ 20X7 $ Sep 15 Bank 15,000 Sep 1 Purchases 10,000 “ 18 Returns outwards 5,000 “ 7 Purchases 20,000 “ 30 Balance c/f 20,000 “ 25 Purchases 10,000 40,000 40,000 Computerised account When accounting records are kept on computers, the accounts are usually drawn up in three columns instead of in T form: one column for ___________, one for _____ ______, and the last one for the ______. debit entries credit entries balance Using this kind of account, the balance is calculated after each entry. Therefore, it is called the _____________ ______. running balance method Example:

Sally Tong 20X7 Debit Credit Balance $ $ $ Computerised account The running balance method will appear as: Sep 1 Purchases 10,000 10,000 Cr “ 7 Purchases 20,000 30,000 Cr “ 15 Bank 15,000 15,000 Cr “ 18 Returns outwards 5,000 10,000 Cr “ 25 Purchases 10,000 20,000 Cr The balance will be ________ using either method. the same Learning Objectives

hink Corner nswer After the year-end closing, businesses will prepare their final accounts. Should we do this immediately after closing the accounts? Or should we do something else before preparing the final accounts? We should prepare a trial balance after closing the accounts at the year end and before preparing the final accounts. A trial balance is a list of all debit balances and credit balances in the books. It is used to check the accuracy of entries in the accounts and identify errors in the books.

Trial balance We can use a trial balance to check whether any _____ has been made in the accounts by comparing the ________________ and the _________________. error total debit balances total credit balances Recall the accounting equation, Assets = Capital + Liabilities. We have mentioned that assets usually have ____________, while capital and liabilities usually have ____________. To have the accounting equation remain in balance, total debit balances should be ______ total credit balances. debit balances credit balances equal to Assets = Capital + Liabilities Total debit balances = Total credit balances

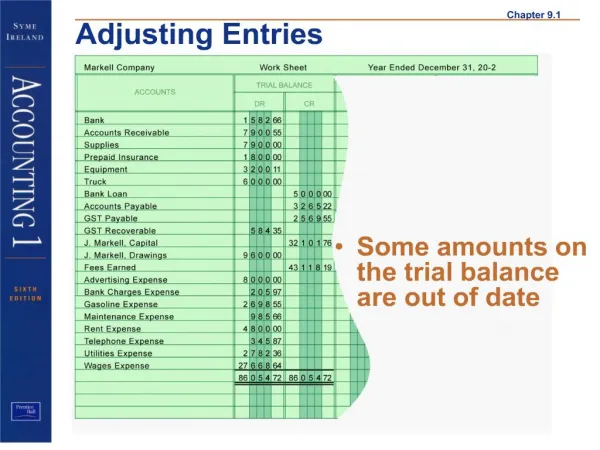

Trial balance Example: Record the following transactions of Margaret Wong for the month of June 20X8. Balance off the accounts at the end of the month, and then extract a trial balance as at 30 June 20X8. Jun 1 Margaret Wong started business with $100,000 cash and $200,000 in the bank. “ 2 Bought goods on credit from Nicolas Tam for $50,000. “ 4 Bought a van by cheque for $60,000. “ 6 Returned defective goods worth $1,000 to Nicolas Tam. “ 9 Sold goods on credit to Benson Chow for $80,000. “ 11 Bought another van by cheque for $40,000. “ 15 Received a cheque from Benson Chow for $80,000. “ 18 Paid rent of $20,000 in cash. “ 22 Bought goods with cash for $40,000. “ 25 Sold goods on credit to Daniel Ng for $60,000. “ 27 Daniel returned goods totalling $3,000 to Margaret. “ 30 Margaret took goods worth $1,000 as a birthday gift for her husband.

Capital 20X8 $ 20X8 $ Cash Bank 20X8 $ 20X8 $ 20X8 $ 20X8 $ Trial balance Jun 1 Cash 100,000 “ 1 Bank 200,000 Jun 1 Capital 100,000 Jun 1 Capital 200,000

Purchases 20X8 $ 20X8 $ Nicolas Tam 20X8 $ 20X8 $ Trial balance Jun 2 Nicolas Tam 50,000 Jun 2 Purchases 50,000

Bank 20X8 $ 20X8 $ Jun 1 Capital 200,000 Van 20X8 $ 20X8 $ Trial balance Jun 4 Van 60,000 Jun 4 Bank 60,000

Returns Outwards Nicolas Tam 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 2 Purchases 50,000 Trial balance Jun 6 Returns outwards 1,000 Jun 6 Nicolas Tam 1,000

Benson Chow Sales 20X8 $ 20X8 $ 20X8 $ 20X8 $ Trial balance Jun 9 Benson Chow 80,000 Jun 9 Sales 80,000

Bank 20X8 $ 20X8 $ Jun 1 Capital 200,000 Jun 4 Van 60,000 Van 20X8 $ 20X8 $ Jun 4 Bank 60,000 Trial balance “ 11 Van 40,000 “ 11 Bank 40,000

Benson Chow Bank 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 1 Capital 200,000 Jun 4 Van 60,000 “ 11 Van 40,000 Jun 9 Sales 80,000 Trial balance “ 15 Benson Chow 80,000 Jun 15 Bank 80,000

Rent Cash 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 1 Capital 100,000 Trial balance Jun 18 Rent 20,000 Jun 18 Cash 20,000

Cash 20X8 $ 20X8 $ Jun 1 Capital 100,000 Jun 18 Rent 20,000 Purchases 20X8 $ 20X8 $ Jun 2 Nicolas Tam 50,000 Trial balance “ 22 Purchases 40,000 “ 22 Cash 40,000

Sales 20X8 $ 20X8 $ Jun 9 Benson Chow 80,000 Daniel Ng 20X8 $ 20X8 $ Trial balance “ 25 Daniel Ng 60,000 Jun 25 Sales 60,000

Returns Inwards Daniel Ng 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 25 Sales 60,000 Trial balance Jun 27 Returns inwards 3,000 Jun 27 Daniel Ng 3,000

Drawings Purchases 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 2 Nicolas Tam 50,000 “ 22 Cash 40,000 Trial balance Jun 30 Drawings 1,000 Jun 30 Purchases 1,000 Step 1 Balance off all the accounts.

Capital 20X8 $ 20X8 $ Jun 1 Cash 100,000 “ 1 Bank 200,000 300,000 300,000 Cash 20X8 $ 20X8 $ Jun 1 Capital 100,000 Jun 18 Rent 20,000 “ 22 Purchases 40,000 100,000 100,000 Trial balance Jun 30 Balance c/f 300,000 Credit balance: $300,000 “ 30 Balance c/f 40,000 Debit balance: $40,000

Jun 1 Capital 200,000 Jun 4 Van 60,000 “ 15 Benson Chow 80,000 “ 11 Van 40,000 280,000 280,000 Bank Purchases 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 2 Nicolas Tam 50,000 Jun 30 Drawings 1,000 “ 22 Cash 40,000 90,000 90,000 Trial balance “ 30 Balance c/f 180,000 Debit balance: $180,000 “ 30 Balance c/f 89,000 Debit balance: $89,000

Jun 6 Returns outwards 1,000 Jun 2 Purchases 50,000 50,000 50,000 Nicolas Tam Van 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 4 Bank 60,000 “ 11 Bank 40,000 100,000 100,000 Trial balance “ 30 Balance c/f 49,000 Crebit balance: $49,000 Jun 30 Balance c/f 100,000 Debit balance: $100,000

Returns Outwards 20X8 $ 20X8 $ Jun 6 Nicolas Tam 1,000 Sales Jun 9 Benson Chow 80,000 “ 25 Daniel Ng 60,000 20X8 $ 20X8 $ 140,000 140,000 Trial balance Jun 30 Balance c/f 1,000 Crebit balance: $1,000 Jun 30 Balance c/f 140,000 Crebit balance: $140,000

Benson Chow Returns Inwards Rent 20X8 $ 20X8 $ 20X8 $ 20X8 $ 20X8 $ 20X8 $ Jun 9 Sales 80,000 Jun 15 Bank 80,000 Jun 18 Cash 20,000 Jun 27 Daniel Ng 3,000 Trial balance Zero balance Jun 30 Balance c/f 20,000 Debit balance: $20,000 Jun 30 Balance c/f 3,000 Debit balance: $3,000

Drawings 20X8 $ 20X8 $ Jun 25 Sales 60,000 Jun 27 Returns inwards 3,000 60,000 60,000 Daniel Ng 20X8 $ 20X8 $ Jun 30 Purchases 1,000 Trial balance “ 30 Balance c/f 57,000 Debit balance: $57,000 Jun 30 Balance c/f 1,000 Debit balance: $1,000

Margaret Wong Trial Balance as at 30 June 20X8 Dr Cr $ $ Trial balance List all debit balances and credit balances separately. Step 2 Capital 300,000 Cash 40,000 Bank 180,000 Purchases 89,000 Nicolas Tam 49,000 Van 100,000 Returns outwards 1,000 Sales 140,000 Rent 20,000 Daniel Ng 57,000 Returns inwards 3,000 Drawings 1,000

Margaret Wong Trial Balance as at 30 June 20X8 Dr Cr $ $ Capital 300,000 Cash 40,000 Bank 180,000 Purchases 89,000 Nicolas Tam 49,000 Van 100,000 Returns outwards 1,000 Sales 140,000 Rent 20,000 Daniel Ng 57,000 Returns inwards 3,000 Drawings 1,000 490,000 490,000 Trial balance Find the total of debit balances and the total of credit balances and see if they are equal. Step 3

Trial balance Uses of a trial balance: 1. As a basis from which the final accounts are prepared. 2. To identify error(s) in the books. 3. To check whether the total debit balances and the total credit balances are equal. Disadvantage of a trial balance: Some errors may still exist even if the trial balance agrees. uiz Corner