Job Order Costing

Job Order Costing. Chapter 19. © 2009 The McGraw-Hill Companies, Inc. Job Order Costing.

Job Order Costing

E N D

Presentation Transcript

Job Order Costing Chapter 19 © 2009 The McGraw-Hill Companies, Inc.

Job Order Costing Job order costing is used by companies that offer customized or unique products or services. Many different products are produced each period and each individual job is treated as a separate unit of output. The unique nature of each order requires tracing or allocating costs to each job, and maintaining cost records for each job. Companies and products using job order costing1. Toll Brothers (custom homes) 2. Trump Industries (skyscrapers) 3. Boeing Aircraft (jet planes) 4. Disney (movies)

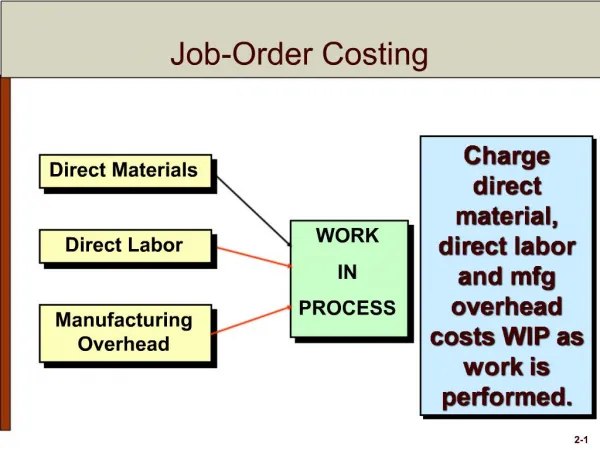

Assignment of Manufacturing Costs to Jobs Source Documents used to Assign Direct Costs to Jobs Material Requisition Form DirectMaterials Job Cost Sheet for Simpson Home Job# 2719 Labor Time Ticket DirectLabor Allocation Base is used to Assign Indirect Costs to Jobs ManufacturingOverhead Cost Driver/Allocation Base Predetermined Overhead Rate

Predetermined Overhead Rates Manufacturing overhead is applied to jobs that are in process. An allocation base, such as direct labor hours, direct labor dollars, or machine hours, is used to assign manufacturing overhead to individual jobs. • We use an allocation base to apply manufacturing overhead because: • It is impossible or difficult to trace overhead costs to particular jobs. • Manufacturing overhead consists of many different items ranging from the grease used in machines to a production manager’s salary. • Actual overhead for the period may not be known until the end of the period.

Estimated TotalManufacturing Overhead Cost POHR = Estimated Units in theAllocation Base Predetermined Overhead Rates The predetermined overhead rate (POHR) used to apply overhead to jobs is determined before the period begins using estimates. Ideally, the allocation base is a cost driver that causes overhead.

$750,000 POHR = 10,000 direct labor hours (DLH) Predetermined Overhead Rates Because home building is a labor intensive business, Toll Brothers uses direct labor hours as the overhead allocation base. Toll Brothers estimates the total manufacturing overhead cost for the year to be $750,000, while direct labor hours are estimated to be 10,000. What is Toll Brothers predetermined overhead rate? POHR = $75.00 per DLH For each direct labor hour worked on a job, $75.00 of manufacturing overhead will be applied to the job.

Journal Entries for Job Order Costing Raw MaterialPurchases Direct Labor Work in Process Cost of GoodsSold RawMaterials Inventory FinishedGoodsInventory DirectMaterials Job101 Job102 Job103 IndirectMaterials Manufacturing Overhead ActualCostsIncurred AppliedToWIP IndirectLabor EquipmentDepreciation

$10,000 Recording the Purchase and Issue of Materials Raw Materials Work in Process Issued to Production Purchases$150,000 DirectMaterials $140,000 IndirectMaterials Mfg. Overhead Job#2719Direct Materials$100,000 Job#3335Direct Materials$40,000 Actual Applied

$5,000 Recording Labor Costs Labor Costs Work in Process DirectLabor $50,000 $55,000 IndirectLabor Mfg. Overhead Job#2719Direct Labor$30,000 Job#3335Direct Labor $20,000 Actual Applied

Recording Actual and Applied Manufacturing Overhead Mfg. Overhead Work in Process Applied AppliedMOH Actual $60,000 $60,000 IndirectMaterials $10,000 IndirectLabor 5,000 OtherMfg. OH 48,000 Job#2719Applied MOH$45,000 Job#3335Applied MOH $15,000 $63,000 Actual Applied MOH MOH / = The difference is closed to cost of goods sold.

Transferring Costs to Finished Goods Inventory and Cost of Goods Sold Finished Goods Work in Process DirectMaterials $140,000 When Job isCompleted$175,000 Cost of GoodsCompleted$175,000 When Jobis Sold$175,000 Job #2719 DirectLabor 50,000 AppliedMfg. OH 60,000 Job #2719 Balance $ 75,000 Cost of Goods Sold $175,000

Calculating Overapplied andUnderapplied Overhead Manufacturing Overhead Applied Actual IndirectMaterials $10,000 800 Actual DL Hours × $75 Predetermined Rate $60,000 Applied Overhead IndirectLabor 5,000 OtherMfg. OH 48,000 Actual TotalMfg. OH 63,000 Underapplied Manufacturing Overhead Balance $3,000

Disposing of Overapplied and Underapplied Overhead Adjusting Cost of Goods Sold for underapplied or overapplied overhead

Summary of Recorded Manufacturing and Nonmanufacturing Costs Finished Goods Raw Materials Work in Process When Jobis Sold$175,000 Cost of GoodsManufactured$175,000 When Job isCompleted$175,000 Issued$150,000 DirectMaterials $140,000 Purchased$150,000 DirectLabor 50,000 AppliedMfg. OH 60,000 Balance $ 75,000 Cost of Goods Sold $175,000 $3,000 Manufacturing Overhead $178,000 Actual Applied Indirect Materials $10,000 Applied Overhead $60,000 Indirect Labor 5,000 Other Mfg. OH 48,000 Nonmanufacturing(Period) Expenses $3,000 Adjusted to COGS Underapplied $3,000 Sales Revenue $275,000 $35,000

Calculating the Cost of Goods Manufactured and Cost of Goods Sold

Calculating the Cost of Goods Manufactured and Cost of Goods Sold Exh. 18-16

End of Chapter 19 © 2009 The McGraw-Hill Companies, Inc.