Download

1 / 61

610 likes | 723 Views

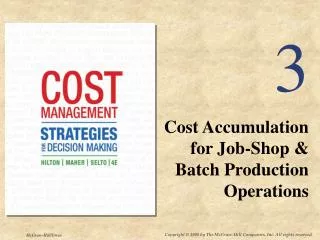

3. Cost Accumulation for Job-Shop & Batch Production Operations. Learning Objective 1. Evaluating Major Types of Product-Costing Systems. Job Costing. Process Costing. vs. Units of output are distinctive (individual jobs, special orders). Each unit has a relatively high value.

E N D

3 Cost Accumulation for Job-Shop & Batch Production Operations

Evaluating Major Types of Product-Costing Systems Job Costing Process Costing vs. Units of output are distinctive (individual jobs, special orders). Each unit has a relatively high value. Costs can be traced feasibly to the units. Units of output are homogeneous (mass production). Each unit has a very low value. Not feasible to trace costs to units.

Evaluating Major Types of Product-Costing Systems Job Costing Process Costing vs. Costs are traced to the process. Then an average cost per unit is calculated for the process. Operation Costing is a hybrid often used for batches of similar products with different types of materials. Costs are traced or assigned to individual jobs.

The Basic Cost Flow Model The model can be used to control use of resources, helping to ensure that goals and objectives are met.

Managing and Using Cost Flow Information - Example Boss, Co. began May with $1,000 of costs in Work-in-Process (WIP) Inventory and $2,000 of completed units in Finished Goods Inventory. During May, Boss incurred $68,000 of production costs. Goods costing $62,000 were sent to Finished Goods during the month. Also, during May, goods costing $60,000 were sold. Using the Cost Flow Model, compute the ending inventory amounts for WIP Inventory and Finished Goods Inventory.

From Job Cost Records Cost of Goods Sold Managing and Using Cost Flow Information - Example

Managing and Using Cost Flow Information Manufacturingoverhead (OH) Applied to eachjob using apredeterminedrate Directmaterials Traced directly to each job THE JOB Traced directly to each job Direct labor

Job Cost Record Managing and Using Cost Flow Information The sum of all the costs in active jobs (unfinished jobs) = A record of all production-related resources used on individual jobs. Work in process inventory

Work-in-Process Inventory Managing and Using Cost Flow Information As individual jobs are completed, their costs are shifted to . . . Represents the cost of all the unfinished (in-process) jobs. Finished goods inventory

Basic Job-Cost Flows Job-cost accounting systems record cost flows systematically. Transactions are journalized. Info is posted to ledger accounts.

Basic Job-Cost Flows Accounts related to particular jobs are posted to those Job Work-in- Process (WIP) accounts.

How Production Overhead is Assigned to Jobs We can determine Direct Materials Cost and Direct Labor Cost for a Job as we do the work. But we won’t know actual Overhead Cost until the end of the accounting period, so we apply overhead to the job using a Predetermined Overhead Rate.

Identify the items to be included as indirect overhead costs. Estimate the costs for each of the indirect overhead items. Select the cost-driver. Estimate the amount of the cost-driver. Compute the predetermined overhead rate (POHR). ÷ Use of Predetermined Overhead Rates

Budgeted total manufacturingoverhead cost for the coming year POHR = Budgeted total units in theallocation base for the coming period Use of Predetermined Overhead Rates The predetermined overhead rate (POHR) used to apply overhead to jobs is determined before the period begins. Ideally, the allocation base is a cost driver that causes overhead.

Overhead applied = POHR × Actual activity Use of Predetermined Overhead Rates Based onestimates and determined before the period begins. Actualamount of thecost driversuch as units produced, direct labor hours, or machine hours incurred during the period.

Use of Predetermined Overhead Rates Using a predetermined rate makes itpossible toestimatetotal job costs sooner. Actual overheadfor the period is notknown until the end of the period. $

Use of Predetermined Overhead Rates Glass Creations applies overhead based on direct labor hours. Totalestimatedoverhead for the year is $360,000. Totalestimatedlabor hours are 12,000.What is Glass Creations’ predetermined overhead rate per hour?

Budgeted total manufacturingoverhead cost for the coming period POHR = Budgeted total units in theallocation base for the coming period $360,000 POHR = 12,000 direct labor hours (DLH) Use of Predetermined Overhead Rates POHR = $30.00 per DLH For each direct labor hour worked on a job, $30.00 of manufacturing overhead will be applied to the job.

Job-Order Cost Flows Let’s examine the cost flows in a job-order costing system. We will use T-accounts and start withmaterials.

Job-Order Cost Flows Raw Materials Work in Process • Direct Materials • Direct Materials • Material Purchases • Indirect Materials Mfg. Overhead Actual Applied • Other Mfg. OH • Indirect Materials

Job-Order Cost Flows Next let’s addlabor costs andapplied manufacturing overhead to the job-order cost flows.

Job-Order Cost Flows Salaries and Wages Payable Work in Process • Direct Labor • Direct Materials • IndirectLabor • Direct Labor • Overhead Applied Mfg. Overhead Actual Applied If actual and applied manufacturing overheadare not equal, a year-end adjustment is required. • Other Mfg. OH • OverheadApplied to Work inProcess • Indirect Materials • IndirectLabor

Job-Order Cost Flows Now let’s complete the goods and sell them.

Job-Order Cost Flows Finished Goods Work in Process • Direct Materials • Cost ofGoodsMfd. • Cost ofGoodsMfd. • Cost ofGoodsSold • Direct Labor • Overhead Applied Cost of Goods Sold • Cost ofGoodsSold

Job-Order Costing Document Flow Summary Let’s summarize the document flow we have been discussing.

Materials usedmay be eitherdirect orindirect. Job-Order Costing Document Flow Summary Direct materials Jobs MaterialsRequisition Manufacturing Overhead Account Indirect materials

An employee’stime may be eitherdirect or indirect. Job-Order Costing Document Flow Summary Direct Labor Jobs Employee Time Ticket Manufacturing Overhead Account Indirect Labor

FinishedGoods Cost of GoodsSold Job-Order Costing Document Flow Summary Direct Materials Indirect FactoryOverhead Work in Process Apply Indirect Direct Labor

Assigning Overhead to Jobs - Summary . . Credit When overhead costs are actually incurred, debit the Manufacturing Overhead account and credit the appropriate account. Debit

Assigning Overhead to Jobs - Summary . . Credit Each time we apply overhead to a job, we debit the job and credit the Manufacturing Overhead account. Debit

Assigning Overhead to Jobs - Summary The difference between actual overhead for the period and applied overhead for the period is called the OVERHEAD VARIANCE.

Overhead Variance Actual > Applied Overhead is UNDERAPPLIED We compare the Actual Overhead to Applied Overhead Actual < Applied Overhead is OVERAPPLIED

Overhead Variance Let’s return to Glass Creations and see what we should do if actual and applied overhead are not equal.

Overhead Variance Assume Glass Creations’ actual overhead for the year was $370,000 for a total of 13,000 direct labor hours. How much total overhead was applied to jobs during the year? Use Glass Creations’ predetermined overhead rate of $30.00 per direct labor hour. SOLUTION Applied Overhead = POHR × Actual Direct Labor Hours Applied Overhead = $30.00 per DLH × 13,000 DLH =$390,000

Overhead Variance Assume Glass Creations’ actual overhead for the year was $370,000 for a total of 13,000 direct labor hours. How much total overhead was applied to jobs during the year? Use Glass Creations’ predetermined overhead rate of $30.00 per direct labor hour. Overhead isoverappliedfor the year by$20,000. What willGlass Creations do? SOLUTION Applied Overhead = POHR × Actual Direct Labor Hours Applied Overhead = $30.00 per DLH × 13,000 DLH =$390,000

Overhead Variance Glass Creations’ Method $20,000may be allocatedto these accounts. $20,000 may beclosed directly to cost of goods sold. OR Work inProcess FinishedGoods Cost of Goods Sold Cost of Goods Sold

$20,000 $20,000 Overhead Variance Glass Creations’Manuf. Overhead Glass Creations’Cost of Goods Sold Unadjusted Balance Actualoverheadcosts $370,000 OverheadAppliedto jobs $390,000 AdjustedBalance $20,000 overapplied

Overhead Variance Glass Creations’ Method

Actual Costing, Normal Costing and Standard Costing Actual Costing? Normal Costing? Standard Costing? Actual direct costs (material and labor) are assigned to jobs as incurred. Manufacturing overhead is assigned to jobs when the actual overhead amounts are known. Actual direct costs (material and labor) are assigned to jobs as incurred. Manufacturing overhead is applied to jobs by using predetermined overhead rates. Standard direct costs (material and labor) are assigned to jobs using pre-determined rates. Manufacturing overhead is applied by using predeter-mined (standard) overhead rates.

Job Order Costing in Service Organizations • Similar to costing • for manufacturing. • Most costs are • related to labor • and overhead. • Standard costing is • used in preparing bids.

Job-order costing emphasizes production in the value chain.We must remember that the other components are alsoimportant contributors to profitability. Job-Order Costing andthe Value Chain Value of products and services R&D Design Supply Production Marketing Distri- bution Customer service

Job and Project Management Complex jobs require scheduling and progress evaluations. • Progress evaluationscompare: • budgeted and • actual costs • actual time and estimated time • during the life • of the project. Gantt chartsare used for scheduling major activities.