Download

1 / 41

410 likes | 691 Views

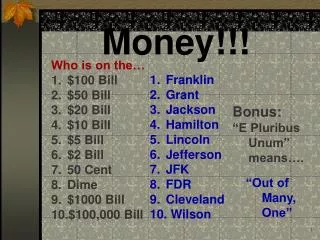

Money!!!. Franklin Grant Jackson Hamilton Lincoln Jefferson JFK FDR Cleveland Wilson. Who is on the… $100 Bill $50 Bill $20 Bill $10 Bill $5 Bill $2 Bill 50 Cent Dime $1000 Bill $100,000 Bill. Bonus: “E Pluribus Unum” means…. “Out of Many, One”. Why do we use money?.

E N D

Money!!! • Franklin • Grant • Jackson • Hamilton • Lincoln • Jefferson • JFK • FDR • Cleveland • Wilson • Who is on the… • $100 Bill • $50 Bill • $20 Bill • $10 Bill • $5 Bill • $2 Bill • 50 Cent • Dime • $1000 Bill • $100,000 Bill Bonus: “E Pluribus Unum” means…. “Out of Many, One”

Why do we use money? What would happen if we didn’t have money? The Barter System: goods and services are traded directly. There is no money exchanged. Every transaction would require a double coincidence of wants—the unlikely occurrence that two people each have a good the other wants.

Problems: • Before trade could occur, each trader had to have somethingtheother wanted. • Some goods cannot be split. If 1 goat is worth five chickens, how do you exchange if you only want 1 chicken?

What is Money? Anything that is generally accepted as final payment for goods and services Money is NOT the same as wealth or income Wealth is the total collection of assets that store value Income is a flow of earnings per unit of time

Commodity money • Money that takes the form of a commodity with intrinsic value • Intrinsic means that the item would have value even if it was not used as money

Fiat money • Money without intrinsic value that is used as money because of a government decree • That’s what fiat means….by order or decree

Liquidity- ease with which an asset can be accessed and converted into cash (liquidized) • M1( High Liquidity) = cash, travelers checks and checking account depositsM2 ( Medium Liquidity) = M1 + savings accounts & money market accounts

0 The Money Supply • The money supply (or money stock):the quantity of money available in the economy • What assets should be considered part of the money supply? Two candidates: • Currency: the paper bills and coins in the hands of the (non-bank) public • Demand deposits: balances in bank accounts that depositors can access on demand by writing a check

Credit vs. Debt Cards What is the difference between credit cards and debit cards? Are credit cards money? A credit card is NOT money. It is a short-term loan (usually with a higher than normal interest rate). Ex: You buy a shirt with a credit card, VISA pays the store, you pay VISA the price of the shirt plus interest and fees. Total credit cards in circulation in U.S: 576.4 million Average number of credit cards per cardholders: 3.5 Average credit card debt per household : $15,788

Medium of exchange: • Money can easily be used to buy goods and services with no complications of barter system.

Unit of account • Money measures the value of all goods and services. Money acts as a measurement of value. • 1 goat = $50 = 5 chickens OR 1 chicken = $10

Store of value • Money allows you to store purchasing power for the future. • Money doesn’t die or spoil.

What backs the money supply? There is no gold standard. Money is just an I.O.U. from the government “for all debts, public and private.” 14

What makes money effective? • Generally Accepted - Buyers and sellers have confidence that it IS legal tender. • Scarce - Money must not be easily reproduced. • Portable and Dividable - Money must be easily transported and divided. The Purchasing Power of money is the amount of goods and services an unit of money can buy.

The Structure of the Fed The Federal Reserve System consists of: Board of Governors(7 members), located in Washington, DC 12 regional Fed banks, located around the U.S. Federal Open Market Committee (FOMC), includes the Bd of Govs and presidents of some of the regional Fed banks The FOMC decides monetary policy. 0 Ben S. BernankeChair of FOMC, Feb 2006 – present

100% reserve banking • You deposit your money in the bank and the bank holds it in the vault until you come and take it out

Fractional Banking • You put your money in the bank. The banks holds a fraction of your deposit and loans out the rest. • Banks making loans increases the money supply. • The smaller the reserve requirement, the more money created by loans in the economy

Bank T-Account T-account: a simplified accounting statement that shows a bank’s assets & liabilities. Example: 0 • Banks’ liabilities include deposits, assets include loans & reserves. • In this example, notice that R = $10/$100 = 10%.

0 Banks and the Money Supply: An Example Suppose $100 of currency is in circulation. To determine banks’ impact on money supply, we calculate the money supply in 3 different cases: 1. No banking system 2. 100% reserve banking system: banks hold 100% of deposits as reserves, make no loans 3. Fractional reserve banking system

0 Banks and the Money Supply: An Example CASE 1: No banking system Public holds the $100 as currency. Money supply = $100.

0 Banks and the Money Supply: An Example CASE 2: 100% reserve banking system Public deposits the $100 at First National Bank (FNB). FNB holds 100% of deposit as reserves: Money supply = currency + deposits = $0 + $100 = $100 In a 100% reserve banking system, banks do not affect size of money supply.

0 Banks and the Money Supply: An Example Suppose R = 10%. FNB loans all but 10% of the deposit: CASE 3: Fractional reserve banking system 10 90 Depositors have $100 in deposits, borrowers have $90 in currency. Money supply = C + D = $90 + $100 = $190 (!!!)

0 Banks and the Money Supply: An Example CASE 3: Fractional reserve banking system How did the money supply suddenly grow? When banks make loans, they create money. The borrower gets • $90 in currency—an asset counted in the money supply • $90 in new debt—a liability that does not have an offsetting effect on the money supply A fractional reserve banking system creates money, but not wealth.

0 Banks and the Money Supply: An Example The process continues, and money is created with each new loan. CASE 3: Fractional reserve banking system In this example, $100 of reserves generates $1000 of money.

The Money Multiplier Money multiplier: the amount of money the banking system generates with each dollar of reserves The money multiplier equals 1/R. In our example, R = 10% money multiplier = 1/R = 10 $100 of reserves creates $1000 of money 0

The Fed’s Tools of Monetary Control money supply = money multiplier × bank reserves • The Fed can change the money supply by changing bank reserves or changing the money multiplier.

Monetary policies • decisions by the Federal Reserve System that lead to changes in the supply of money and the availability of credit. (banks and overall financial system) • Changes in the money supply can influence overall levels of spending, employment and prices in the economy by inducing changes in interest rates charged for credit and by affecting the levels of personal and business investment spending.

Tools of the Fed - discount rate • the rate charged by the central bank if individual banks wish to borrow funds. • A higher discount rate reduces the money supply while a lower discount rate increases the money supply.

The Fed makes loans to banks, increasing their reserves. • Traditional method: adjusting the discount rate—the interest rate on loans the Fed makes to banks—to influence the amount of reserves banks borrow • New method: Term Auction Facility—the Fed chooses the quantity of reserves it will loan, then banks bid against each other for these loans. • The more banks borrow, the more reserves they have for funding new loans and increasing the money supply.

Tools of the Fed - open market operations • most commonly used tool • buying and selling government bonds. • buys bonds - increases the amount of money in the economy • sells bonds - reduces the amount of money in the economy. • tries to influence the federal funds rate, which is the interest rate a bank charges when it lends excess reserves to another bank.

0 The Federal Funds Rate • On any given day, banks with insufficient reserves can borrow from banks with excess reserves. • The interest rate on these loans is the federal funds rate. • The FOMC uses OMOs to target the fed funds rate. • Changes in the fed funds rate cause changes in other rates and have a big impact on the economy.

Monetary Policy and the Fed Funds Rate To raise fed funds rate, Fed sells govt bonds (OMO). This removes reserves from the banking system, reduces supply of federal funds, causes rf to rise. rf Federal funds rate S2 S1 3.75% 3.50% D1 F F2 F1 Quantity of federal funds 0 The Federal Funds market

Tools of the Fed - reserve requirement • the percentage of deposits that banks are required to hold and not lend out. • A higher reserve requirement reduces the money supply by limiting bank lending • a lower reserve requirement increases the money supply by increasing bank lending.

How the Fed Influences the Reserve Ratio • Recall: reserve ratio = reserves/deposits,which inversely affects the money multiplier. • The Fed sets reserve requirements: regulations on the minimum amount of reserves banks must hold against deposits. Reducing reserve requirements would lower the reserve ratio and increase the money multiplier. • Since 10/2008, the Fed has paid interest on reserves banks keep in accounts at the Fed. Raising this interest rate would increase the reserve ratio and lower the money multiplier.

Economy is experiencing inflation • central bank officials will use contractionary monetary policy • raise interest rates by contracting (or reducing the rate of growth in) the money supply.

Lags are unpredictable • the Fed must exercise caution in using monetary policy, taking care not to implement too large a change in the money supply —one that could have adverse effects down the road

A More Realistic Balance Sheet • Assets: Besides reserves and loans, banks also hold securities. • Liabilities: Besides deposits, banks also obtain funds from issuing debt and equity. • Bank capital: the resources a bank obtains by issuing equity to its owners • Also: bank assets minus bank liabilities • Leverage: the use of borrowed funds to supplement existing funds for investment purposes

Economy is in a recession • central bank officials will use expansionary monetary policy • seeks to reduce interest rates by expanding the supply of money in the economy. • lower interest rates encourage additional aggregate demand for consumption and investment, shorten or end the recession.

Fiscal policies • decisions to change spending and tax levels by the federal government. • adopted to influence national levels of output, employment, and prices.