Download

1 / 34

340 likes | 480 Views

Retirement Challenges, Rewards, and the Roth IRA. Producer Name Producer Address License No. Retirement Challenges. Living past your life expectancy. Increased expenses in retirement. Decreased earnings potential in retirement. Impact of taxes. Things To Consider. Longevity.

E N D

Retirement Challenges, Rewards, and the Roth IRA Producer Name Producer Address License No.

Retirement Challenges Living past your life expectancy. Increased expenses in retirement. Decreased earnings potential in retirement. Impact of taxes.

Things To Consider • Longevity. • People are living longer. • Expenses. • Expenses are going up. • Earnings potential. • Do you plan on working in retirement? • Taxes. • Do you believe you could be in a higher tax bracket during retirement?

Cost of Living in 1965 Source: http://www.1960sflashback.com/1965/Economy.asp. • New home: • $21,500. • First-class stamp: • $0.05. • Gallon of regular gas: • $0.31. • Dozen eggs: • $0.53. • Gallon of milk: • $0.95.

Cost of Living Today • Based on average new home price. U.S. Census Bureau News, “New Residential Sales in November 2009,” (December 23, 2009). • United States Postal Service as of December 31, 2009. • Based on Bureau of Labor Statistics data extracted on December 31, 2009. • New home:1 • $280,300. • First-class stamp:2 • $0.44. • Gallon of regular gas:3 • $2.60. • Dozen eggs:3 • $1.70. • Gallon of milk:3 • $3.03.

“In retirement, your paycheck might go away, but taxes won’t.” David Pitt, Associated Press, “Your Money: More Roth IRA Conversions Allowed” (November 9, 2009).

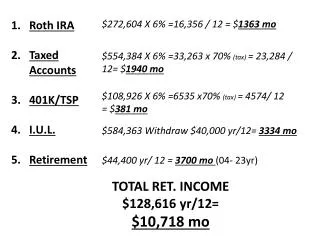

The Statistics * Assumes work from age 20 to 65 and two pay periods per month. ** Assumes 20 years of retirement (age 65 to 85) and two “pay periods” per month. • Average number of paychecks during working years vs. number of paychecks in retirement: • 1,080 pay periods to get to retirement.* • 480 pay periods during retirement.** • What will your retirement paycheck look like?

Retirement Traffic Light • Red light = taxable. • Yellow light = taxdeferred. • Green light = taxfree.

Stop Stop building a fully taxable retirement strategy.

Slow Down Slowly build tax-deferred retirement assets.

Go Ahead! Go ahead with strategies that offer potentially tax-free retirement income.

Tax Bracket Increase? Michael Miller, Dallas Morning News Expert Financial Advice Blog, “2010 Roth IRA Conversion, New Rules, and Tax Strategy” (November 3, 2009) http://www.house.gov/list/press/tx05_hensarling/rsc/020608TaxManCometh.html. “Unless Congress passes new legislation, the top four federal tax brackets will revert from the current 25%, 28%, 33%, and 35% levels to their pre-2001 levels of 28%, 31%, 36%, and 39.6%.” This is scheduled to occur in 2011.

History of Federal Tax Brackets Sources: IRS and taxfoundation.org.

Social Security TaxationWhat does it mean to you? If you move to a 31% federal tax bracket from a 28% bracket, you may owe as much as 57 cents in taxes on every dollar you take from your retirement assets.

28% Example • For each additional dollar withdrawn from your traditional IRA: $1.00 in income from traditional IRA. + $0.85 of your Social Security is taxed. = $1.85 of taxable income! = $0.52 in federal income taxes.

31% Example • For each additional dollar withdrawn from your traditional IRA: $1.00 in income from traditional IRA. + $0.85 of your Social Security is taxed. = $1.85 of taxable income! = $0.57 in federal income taxes.

Ask Yourself… “Would you rather pay taxes on the seed or the harvest?” –Douglas R. Andrew

What Is a Roth IRA? An individual retirement account in which a person can set aside after-tax income up to a specified amount each year. Earnings on the account are tax free, and tax-free withdrawals may be made after age 59½.

“Since their creation more than a decade ago, Roth IRAs have been among the best tax breaks available.” Ed Slott, “Roth Conversion Planning for 2009 and 2010,” Ed Slott’s IRA Advisor(July 2009).

Funding a Roth IRA Roth IRAs can be funded with a variety of accounts such as annuities, mutual funds, certificates of deposit, and more.

Converting to a Roth IRA Might Help You… * Not all states waive the penalty on conversions. Reduce your future state and federal income taxes.* Reduce the amount of your Social Security income included as taxable income. Avoid taking required minimum distributions you may not need. Provide your beneficiaries with a lifetime of income tax-free distributions.

Why This May Be the Right Time for a Roth IRA Under a new law effective January 1, 2010, anyone, regardless of income, can convert from a traditional IRA to a Roth IRA starting in 2010. The value of your traditional IRA has likely declined over the past months; years; and, even for some, over the past decade. Do you think that the market may head back up? You will likely spend less in taxes by converting now, while your Roth IRA grows tax free.

Would You Rather Pay Uncle Sam $25K Now or Close to $88K Later?

Caution! Source: http://www.rothirarules.net/. “The Roth is not appropriate for everyone, although most people in the middle income bracket will likely find it to their advantage.”

Ask Yourself… Are taxes expected to increase? Has the value of my IRA decreased? Do I need to live on my IRA in the next few years? Do I need access to my IRA before age 59½? Will I still be working at age 70½? Do I want to keep adding to my IRA account assets after age 70½? Do I have the money to pay the taxes on conversion?

Something To Think About… Does partial tax-free retirement make more sense?

What Is Your Retirement Reality? Many who have retired from their primary occupation continue to work in some capacity during their early retirement years. Supplementing that income with Roth distributions keeps taxes lower. Taxable retirement funds can be drawn later when taxable income is lower.

Roth IRAs • Great advantages: • Tax-free growth of earnings. • Tax-free withdrawals. • No required minimum distributions at age 70½ . • Tax-free inheritance for beneficiaries. • Contributions permitted after age 70½. • Doesn’t impact Social Security taxation. • Great opportunities for many Americans.

Disclosures This presentation is not intended as an invitation to purchase any particular insurance product or fixed annuity, nor is it intended as an endorsement of any particular product or company. It is merely intended to provide you with general information about Roth IRAs and fixed annuities, to assist you in making an informed choice about financial service products currently available to you and to help you determine what products may be best suited for you. Fixed annuities, including Roth IRA annuities, may be useful retirement tools for some people. However, fixed annuities may not be suitable for all. Please consult a licensed insurance agent regarding your age, health, financial objectives, short- and long-term financial goals, liquidity needs, risk tolerance, tax status, and overall financial situation to determine if one is right for you. You should thoroughly review all brochures, specimen contracts, buyer’s guides, and disclosure forms before purchasing any fixed annuity or any other financial services product. Please refer to IRS Publication 590 for more information on Roth IRAs.

Disclosures (cont’d) Fixed annuity earnings are tax deferred until withdrawn. Use of annuities with qualified-type plans [401(k), IRA, 403(b)] may not provide any additional tax benefits above those you already receive in such a plan. Withdrawals may be subject to income tax and a 10% federal income tax penalty if taken before age 59½. Surrender charges may apply if you withdraw more than the penalty-free amount in a year. Fixed annuities generally guarantee a minimum interest rate on all or a percentage of each contribution over the life of the contract, less any withdrawals and/or deductions and early surrender charges. Guarantees are based on the claims-paying ability of the insurer. Insurance agents do not give legal, investment, or tax advice. Please consult your attorney, accountant, or other qualified professional regarding annuity taxation as it applies to you.