Download

1 / 13

130 likes | 321 Views

Accurate AVM Values Help Monitor Subprime Appraisal Risk Doug Gordon Director—Collateral Risk Management Freddie Mac. MBA Subprime Lending Conference May 13, 2004. Subprime Collateral Risk. With subprime loans, risk of Appraisal bias is higher. 3 legs of risk management stool:

E N D

Accurate AVM Values Help Monitor Subprime Appraisal RiskDoug Gordon Director—Collateral Risk Management Freddie Mac MBA Subprime Lending Conference May 13, 2004

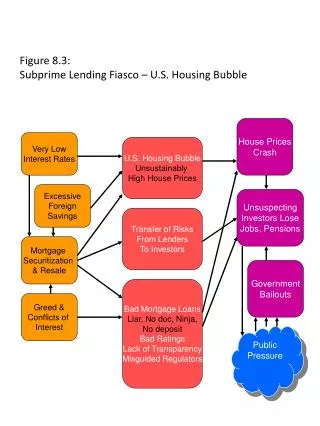

Subprime Collateral Risk • With subprime loans, risk of Appraisal bias is higher. • 3 legs of risk management stool: credit, capacity, collateral. 1. Credit: Borrowers typically have lower credit quality. 2. Capacity: Borrowers are raising their loan size, absolutely and relative to income. 3. Collateral: Loan amounts are rising. If appraisal doesn’t support higher loan amount, loan isn’t made.

Subprime Collateral Risk – continued • Weak credit and capacity mean that collateral value becomes essential for the deal. • Pressure on appraisers to upwardly bias property value so that loan can be made. • We observe that risk of appraisal bias rises with the risk of the loan transaction. For subprime there is high risk of bias.

Monitoring and mitigating collateral value risk • Some subprime lenders require a second appraisal and take the lower of the two for subprime lending decisions. • Some subprime lenders look at AVM values to confirm or refute the original appraisal. • Some lenders now use tools that combine AVM values with other property and loan information, such as Home Value Calibrator, to assess the risk that the appraisal is inflated.

An accurate AVM helps identify appraisal risk • One can estimate $175,000 for every home in the US. This will be correct on average, but far off on each individual estimate. • Knowing the accuracy of each model estimate is as important as knowing the estimated value itself. • Not only accuracy, expected accuracy is crucial. • If your AVM provides a Forecasted Standard Deviation (FSD) with each estimate, you know how accurate that estimate is. You can calculate the size of the risk that the appraisal being reviewed is inflated.

Value of Precision The curve for 10% Forecast Standard Deviation (FSD) is applied to the LTV cost curve, and centered at 80 LTV to provide a weighted average cost for an 80 LTV loan. Next, the 16% distribution is applied to the LTV cost curve, also centered at 80 LTV. The results are the points for 10% and 16% in Figure 3 below.

Forecast Standard Deviation Assessed 70 LTV Assessed 80 LTV Assessed 90 LTV 10% $0 $0 $0 11% $8 $23 $31 12% $18 $47 $63 13% $29 $74 $102 14% $42 $101 $144 15% $55 $129 $186 16% $67 $156 $228 17% $81 $183 $272 18% $94 $209 $316 19% $107 $233 $356 20% $119 $256 $397 Value of Precision Extra Cost of additional percentage of imprecision at different LTVs for a $200,000 property • The dollar costs are the extra costs of the particular level of imprecision beyond the risk cost when the true market value is known within 10% FSD. • The costs are taken from a generic version of a mortgage cost curve. Additional cost per loan at estimated 80 LTV $129 - $23 = $106

Tying Confidence Scores to Performance:Example using HVE • HVE now provides Forecast Standard Deviation (FSD) with each value estimate. HVE continues to provide confidence scores that tie directly to FSD. • High – at least as accurate/typically more accurate than average appraisal. FSD in use <=13%. • Medium – comparable to somewhat less accurate than average appraisal. FSD in use >13 – 20%. • Low – Less accurate than average appraisal (more common for rural and diverse housing types). FSD in use > 20%.

Another Way to Evaluate Subprime Appraisal Risk: Home Value Calibrator • A quality control tool that assigns loans a score indicating the risk of inflated appraisal, valuation, or borrower’s stated value. • Automated Valuation Model Combined with Statistical Scoring Model. • Generates a property value risk score that may be used to prioritize workflow or additional review. • Aggregates results to identify sources of bad values or other trends.

Interpreting Calibrator Scores • Similar to other industry scoring ranges. • Lower scores indicate a higher risk that property valuation is inflated. • Risk of inflated valuation is more than doubled with every one-hundred point decline in scores.

Using your AVM to Monitor Risk Example using HVE. • Appraisal value is 200,000. • HVE value is 175,000, Forecast Standard Deviation (FSD) is .08. • Pr(market value >=200,000) < .05, relatively high risk that the appraisal is inflated. Example using Calibrator. • Appraisal value is 200,000. • HVE value going into Calibrator is 175,000. Neighborhood values are around 170,000. Loan is higher LTV subprime. • Calibrator score is 545. Indicates relatively high risk that the appraisal is significantly inflated (about 3-4 times average risk).

Quality Control Uses of AVMs • AVM coverage, hit rate, and accuracy help with prefunding analysis and when evaluating your portfolio. • Combination of AVM and statistical scoring to identify the risk of inflated appraisal (Calibrator or HVE with FSD). • Evaluate pools of mortgages or mortgages originated by third-parties. • Monitor collateral risk of your nonperforming loans.

Review Appraisals Confirm Risk Identified by Automated Property Tool • AVMs provide an independent read on property value from the original appraisal. • If the AVM model value or property risk measure indicates property value risk, a field review appraiser is called to determine value. • Review can be done pre-funding or post-funding. • Field review appraisals are much preferred to desk reviews, as property condition and marketability may well be issues as well as relationship to comps.