Download

1 / 5

50 likes | 229 Views

A Framework for Financial Stability Contrasts between Price and Financial Stability. In standard forecasts, assume shock (X) is zero. In simulation/stress tests, assume shock non-zero, and try to study outcomes (Y), as a function of shock (X), i.e. Y = f(X)

E N D

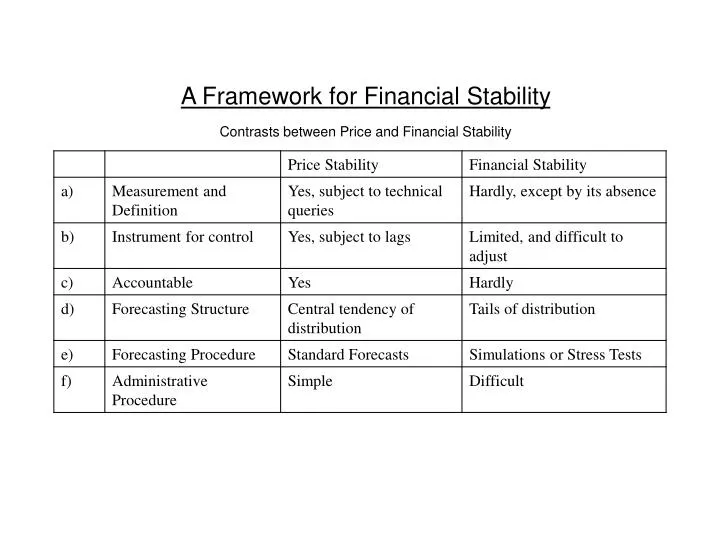

A Framework for Financial Stability Contrasts between Price and Financial Stability

In standard forecasts, assume shock (X) is zero. In simulation/stress tests, assume shock non-zero, and try to study outcomes (Y), as a function of shock (X), i.e. Y = f(X) Easier to observe Y, than X, so usual measure of stability is outcome, e.g. variance of asset prices, credit flows, etc., whereas the key question is the amplitude of multiplier linking outcome with initial shock.

Stress tests are usually macro/micro, i.e. Yi = f(X), independently of interactions within sector, (i.e. banking sector), and between sectors. Also economic context of specific shocks often left vague. Also speed of shock important (Argentina/Russia). Obviously limited, and unsatisfactory for a FSD. Is it possible to design macro/macro stress tests:- 1) By models? 2) Empirically? Can it be done by looking at:- a) the main individual agents; b) each sector in aggregate; c) `the weakest link’. Each no doubt has its advantages/disadvantages.

Is it possible 1) to rank relative importance of shock, a function of:- a) probability b) impact c) speed; 2) to assess macro-level effect; 3) to consider prior (contingency) plans?

Measures:- 1) Structure of Markets, (problem of innovations) 2) Capital Requirements 3) Liquidity