Download

1 / 39

420 likes | 880 Views

Chapter 13 Cost of Capital. Capital Structure. A firm’s Capital Structure its mix of the three components of long term funding Debt Preferred stock Equity Target Capital Structure Raising Money in the Proportions of the Capital Structure. The Purpose of the Cost of Capital.

E N D

Capital Structure • A firm’s Capital Structure its mix of the three components of long term funding • Debt • Preferred stock • Equity • Target Capital Structure • Raising Money in the Proportions of the Capital Structure

The Purpose of the Cost of Capital • The cost of capital is the average rate paid for the use of the firm’s capital funds • Capital is money acquired for use over long periods • The cost of capital provides a benchmark against which to evaluate investments • Projects should not be undertaken unless they return more than the cost of the funds invested in them => the cost of capital. • Rule is equivalent to • Project IRR exceeds the cost of capital • Project NPV > 0 when calculated at the cost of capital

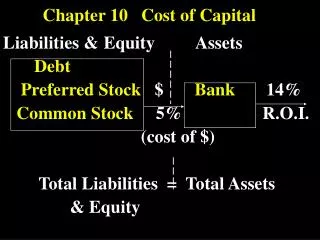

Capital Components and Structure • A firm’s Capital Components are • Debt • Preferred stock • Common equity • Capital structure is the mix of the three capital components - generally expressed in percentages

Capital Structure Concepts • Target Capital Structure • A mix of components that management considers optimal and strives to maintain • Raising Money in the Proportions of the Capital Structure • In cost of capital calculations, we assume money is raised in a constant proportion of debt, preferred and common equity

Returns on Investments and the Costs of Capital Components • Investors provide capital by purchasing the firm’s securities • Returns paid to investors adjusted for taxes and administrative expenses are the firm’s costs • The risk of securities to investors differ • Equity: riskiest investment, highest investor return, highest cost to company • Debt: safest investment, earns lowest return, costs firm least • Preferred stock: intermediate risk, return, and cost

The Weighted Average Calculation (WACC) • A firm’s cost of capital is a weighted average of the costs of the three capital components where the weights reflect the $ amounts of each component in use • Referred to in two ways • k, the cost of capital • WACC, for weighted average cost of capital

Concept Connection Example 13-1 WACC Calculations Calculate the WACC for the Zodiac Company given the following information about its capital structure.

Concept Connection Example 13-1 WACC Calculations First calculate the capital structure weights based on the values given. For example the weight of debt is $60,000 $200,000 = 30%. Next, each component’s cost is multiplied by its weight and the results are summed as shown:

Capital Structure and CostBook Versus Market Value • WACC can be calculated using either book or market values of capital components • WACC used to evaluate next year’s projects • Supported by capital raised next year • Book values - capital raised and spent years ago • Current market values are best estimate of next year’s capital market conditions • Market values are the appropriate basis for WACC calculations

Capital Structure Customary Approach • Structure: Assume the firm will either • Maintain present capital structure based on the current market prices of its securities • Or strive to achieve some target structure also based on current market prices. • Costs: Always use market-based component costs to develop the WACC.

Calculating the WACC • Step 1: Develop a market-value-based capital structure • Step 2: Adjust market returns on the underlying securities to reflect the costs of the underlying capital components Step 3: Combine in calculating the WACC

Concept Connection Example 13-2 Market-Value-Based Capital Structure The Wachusett Corporation has the following capital situation. Debt:2,000 30-year, $1,000 face value, 12% coupon bonds issued 5 years ago. Now selling to yield 10%. Preferred stock:4,000 shares of preferred are outstanding, each share pays an annual dividend of $7.50. Originally sold to yield 15% of $50 face value. Now yielding 13%. Equity:200,000 shares of common stock are selling at $15. Develop Wachusett's market-value-based capital structure.

Concept Connection Example 13-2 Market-Value-Based Capital Structure The market value of each capital component is the current price of each security multiplied by the number outstanding. Debt: Multiply by 2,000 bonds outstanding for the the market value of debt $1,182.55 x 2,000 = $2,365,100 Pb = PMT[PVFAk,n] + FV[PVFk,n] = $60[PVFA5,50] + $1,000[PVF5,50] = $60(18.2559) + $1,000(0.0872) = $1,182.55

Concept Connection Example 13-2 Market Value-Based Capital Structure Preferredstock PP = $7.50 / .13 = $57.69 Multiply by 4,000 for market value of preferred $57.69 x 4,000 = $230,760 Equity At $15 the market value of equity is $15 x 200,000 shares = $3,000,000 Summarize and calculate the component weights:

Calculating Component Costs of Capital • Begin with the market return received by new investors in each capital component, kd, kp, and ke • Make adjustments for the effects of taxes and transaction costs to arrive at cost to the issuing firm

Calculating Component Costs of Capital • Tax adjustment applies only to debt (Tax rate is T) • Interest is tax deductible to the paying firm • Cost of debt = kd (1 – T) • Debt made even cheaper by tax adjustment • Flotation costs: percentage of security’s price (f) • Apply to preferred and new sales of common • Increases effective cost • Cost of component = kp / (1 – f) or ke / (1 – f)

Concept Connection Example 13-3 Cost of Debt • Blackstone has 12% coupon bonds yielding 8% to investors buying them now. Blackstone’s marginal tax rate is 37%. What is Blackstone’s cost of debt? Cost of debt = kd(1 - T) = 8%(1 - .37) = 5.04%

Concept Connection Example 13-4 Cost of Preferred Stock • Francis issued preferred paying 6% of its $100 par value. Flotation costs are 11%. • a. What is Francis’s cost of preferred if similar issues yield 9% • b. Calculate the cost of preferred if the shares are selling for $75.

Concept Connection Example 13-4 Cost of Preferred Stock • Solution: • a. cost of preferred = = kP / (1-f) = 9% / (1-.11) = 10.1% • b. cost of preferred = = DP / (1-f)PP = $6 / (1-.11) $75 = 9.0%

The Cost of Common Equity • The cost of common equity is not precise due to the uncertainty of future equity cash flows • The market return on common equity is estimated • CAPM • Constant Growth model • Risk premium • The sources of new common equity include • Retained earnings • Newly sold stock

The Cost of Retained Earnings • Retained earnings (RE) are not free • Reinvested earnings that belong to stockholders • Stockholders could have spent if paid as dividends • No adjustments to return on RE necessary • Payments to stockholders not tax deductible • No new securities so no flotation costs • Investor return = Component cost of RE • Three ways to estimate • CAPM, Gordon Model, and Risk Premium

The CAPM Approach • Estimate using usingthe CAPM’s SML: • kx= kRF + (kM - kRF) bX

Concept Connection Example 13-5 Cost of Retained Earnings – SML Strand Corp’s beta is 1.8. The return on the S&P 500 is 12%. Treasury bills are yielding 6.5%. Estimate Strand’s cost of retained earningsusing the CAPM’s SML: cost of RE = kX = kRF + (kM - kRF)bX = 6.5% (12% 6.5%)1.8 = 16.4%

Solve for ke, which represents expected return. The Dividend Growth (Gordon Model) Approach The Gordon model is usually used to estimate intrinsic value. However, it can also be solved for return by substituting the stock’s current price. Use actual price

The Dividend Growth (Gordon Model) Approach Example 13-6 Periwinkle stock sells for $33.60, paid a dividend of $1.65 and will grow at 7.5%. Estimate its cost of retained earnings. Solution:

The Risk Premium Approach • Difference between debt and equity risks is fairly constant. • Estimate return on equity by adding 3% to 5% to the return on its debt: ke= kd + rpe • Example 13-7 • Carter’s bonds yield 12% • ke = kd + rpe = 12% + 4% = 16%

The Cost of New Common Stock • Firms often need to raise more equity than that generated by retained earnings • Equity from new stock is just like equity from RE, except it involves flotation costs • Market return estimates for RE must be adjusted for flotation costs to determine the cost of issuing new common stock • Use the Gordon model • Insert (1 ─ f) to recognize flotation cost

The Cost of New Common Stock Example 13-8 Periwinkle of Example 13-6 needs to raise money beyond RE. Estimate its cost of new equity from stock if floatation costs are 12% Solution:

The Marginal Cost of Capital (MCC) • WACC not independent of amount of capital raised • WACC typically rises as more capital is raised • The Marginal Cost of Capital (MCC) is a graph of the WACC showing increases as larger amounts are raised during a planning period

The Break in MCC When Retained Earnings Run Out • Breaks (jumps) in the MCC occur when cheap sources of financing are used up • First increase in MCC usually occurs when the firm runs out of RE and starts raising external equity by selling stock • Locating the Break is important

Concept Connection Example 13-9 The MCC Solution:Calculate the WACC using the cost of retained earnings and the cost of new equity.

Example 13-9 Locating the Break In Brighton’s MCC Schedule • Business plan projects RE of $3M • Capital structure is 60% equity • Capital is raised in the proportions of the capital structure we ask • $3M is 60% of what number? • $3M / .6 = $5M (WACC Break)

Other Breaks in the MCC Schedule • Other Breaks in the MCC Schedule occur when the cost of borrowing increases • As debt increases firm becomes riskier so lenders require higher interest rates • Causes further upward breaks in the MCC

Combining the MCC and IOS • The investment opportunity schedule (IOS) is a plot of the IRRs of available projects arranged in descending order • The MCC and IOS plotted together show which projects should be undertaken • Interpreting the MCC • The firm's WACC for the planning period is at intersection of the MCC and the IOS

Figure 13-2 MCC Schedule and IOS Projects A, B and C should be undertaken because their expected returns exceed the expected costs.

A Potential Mistake—Handling Separately Funded Projects • If a project is funded entirely by a single capital source • Should the cost of capital used to evaluate that project be the cost of the single source, or the firm's WACC? • It should be the WACC because firms cannot continue to raise capital at the single source rate indefinitely