Download

1 / 15

150 likes | 174 Views

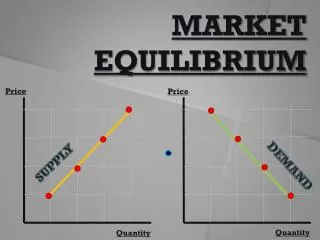

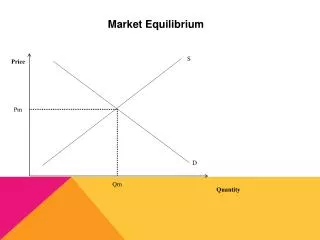

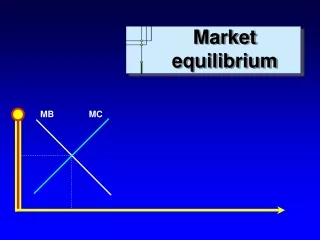

CNANGES IN MARKET EQUILIBRIUM. Economists say that a market will tend toward equilibrium. Why? There are two forces that can push a market into disequilibrium: A shift in demand A shift in supply. CHANGE IN PRICE. A shift of the supply curve will change the equilibrium price and quantity.

E N D

CNANGES IN MARKET EQUILIBRIUM Economists say that a market will tend toward equilibrium. Why? There are two forces that can push a market into disequilibrium: A shift in demand A shift in supply

CHANGE IN PRICE • A shift of the supply curve will change the equilibrium price and quantity. • Shift in supply is caused by many factors technology, taxes, subsidies, price of raw materials, and labor

SHIFTS IN DEMAND • An increase in market demand will affect the equilibrium in that market. • Shifts in demand cause problems • Shortages • Search costs • Excess supply

THE ROLE OF PRICES • Prices are a key element of equilibrium. Price changes can move markets back toward equilibrium and solve the problem of excess demand and excess supply. • Prices in a free market are a tool to distribute goods and resources

PRICES IN THE FREE MARKET • Prices serve a vital role in a free market economy. • Prices help move land, labor, and capital into the hands of producers. • They help put finished goods into the hands of consumers.

ADVANTAGES OF PRICES • Prices provide a language for buyers and sellers. Without them a supplier would have no consistent and accurate way to measure demand for a good. • Price as an incentive • Both buyers and sellers look at prices to find information on a goods demand and supply • Prices are a signal that tell a consumer or producer how to adjust • Prices communicate to both buyers and sellers whether a good is in short supply or readily available.

ADVANTAGES OF PRICES CONT. • Prices as Signals • High prices are a signal to producers that a good is in demand and that they should produce more • Low prices are a signal to producers that a good is being overproduced and that they should use there resources to produce another good that would make them more profits. • Low prices tell consumers to buy more low opportunity cost • High prices tell consumers to buy less

ADVANTAGES OF PRICE CONT. • Flexibility • When supply or demand shifts the equilibrium in that market is changed and quantity supplied and price need to change to rebalance the market. • Prices are easily increased or decreased to solve excess demand or excess supply. • Output levels are not flexible • Supply shock sudden shortage • Rationing

ADVANTAGES OF PRICES CONT • PRICE SYSTEM IS “FREE” • Distribution of goods in a free market system based on prices costs nothing to administer unlike a centrally planned economy. • Free market system pricing distributes goods through millions of decisions made every day by producers and consumers.

WIDE CHOICE OF GOODS • A benefit of a market-based economy is the diversity of goods and services a consumer can buy. • Prices give producers a way to allow consumers to choose similar products • Prices provide an easy way for a consumer to narrow their choices to a certain price range • Prices allow producers to target the audience they want with the products that will sell the best to that group.

WIDE CHOICE OF GOODS CONT. • Rationing • Government controls the distribution of goods Why do it? • Shortages • Black Market • When people do business without regard for government controls on price of quantity. • It allows consumers to pay more so they can buy a good when rationing makes a good otherwise unavailable.

EFFICIENT RESOURCE ALLOCATION • All of the advantages of a free market system allows prices to allocate resources efficiently. • The economic resources land, labor, and capital will be used for their most valuable purposes. • A market system, with its freely changing prices, ensures that resources go to the uses that consumers value most. • A price based system also ensures that resources use will adjust to the changing demands of consumers. • All of these changes take place without any government control because people who own the resources look for the largest profit. • How do people who earn the largest profit?

PRICES AND THE PROFIT INCENTIVE • What would happen if a hot summer was predicted? • What would consumers do? • What would power companies do? • What would happen to prices? • What would producers do? • The rise in prices would have given the incentive to producers to meet these needs

THE WEALTH OF NATIONS • Adam Smith explained that producers do not provide goods because of charity but instead they provide goods because prices are such that they will profit by provide those goods. • Market Problems • There are some exceptions to the idea that markets lead to an efficient allocation of resources. • Imperfect competition it can affect prices and higher prices affect consumer decisions (few producers not enough competition higher prices) • Spillover costs (externalities) Producers do not pay these cost so they will produce more than the equilibrium quantity. Extra cost past on to consumer • Imperfect information if buyers and sellers do not have enough information to make informed choices about a product leads to bad choices.