Download

1 / 30

300 likes | 373 Views

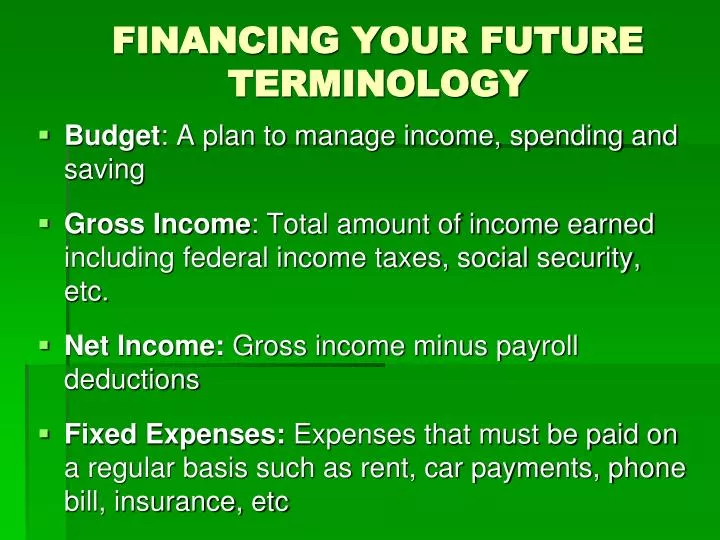

FINANCING YOUR FUTURE TERMINOLOGY. Budget : A plan to manage income, spending and saving Gross Income : Total amount of income earned including federal income taxes, social security, etc. Net Income: Gross income minus payroll deductions

E N D

FINANCING YOUR FUTURETERMINOLOGY • Budget: A plan to manage income, spending and saving • Gross Income: Total amount of income earned including federal income taxes, social security, etc. • Net Income: Gross income minus payroll deductions • Fixed Expenses: Expenses that must be paid on a regular basis such as rent, car payments, phone bill, insurance, etc

FINANCING YOUR FUTURETERMINOLOGY • Variable Expenses: Expenses that change due to price and willingness and desire to purchase items such as food, clothing, entertainment • Liabilities: Financial obligations that must be paid • Assets: Possessions that have economic value • Net Worth: Assets minus liabilities

FINANCING YOUR FUTURETERMINOLOGY • Dividend: A payment of a portion of a company’s net profits, which is periodically made to stockholders • Liquidity : The ease with which a financial asset can be turned into cash • Compound Interest: Interest paid on the principle and on the interest earned in an account

FINANCING YOUR FUTURETERMINOLOGY FICO Score: A number applied to a person’s credit history to assess the person’s reliability to repay borrowed funds.

Table of FICO Credit Scores % of Population Credit Score • 2% 300 – 499 • 5% 500 – 549 • 8% 550 – 599 • 12% 600 – 649 • 15% 650 – 699 • 18% 700 – 749 • 27% 750 – 799 • 13% 800 – 850 The Higher your FICO Score, The lower your interest rate on a loan

How to get a Credit Report • To obtain a free credit report • Online: www.annualcreditreport.com • Toll free call: (877) 322-8228 • Request by mail: Annual Credit Report Request Service P.O. Box 105281 Atlanta, GA 30348-5281

FINANCING YOUR FUTURETERMINOLOGY • Minimum Payment: The smallest payment a person is required to make in a given month on a credit account (Credit card companies love it when you do this)

FINANCING YOUR FUTURETERMINOLOGY • Human Capital: Knowledge and skills that a person obtains to better their future – Example is College, Trade School, or Military • Annual Percentage Rate (APR): The interest rate charged, expressed as a percent per year, for the use of credit • Credit Bureau: An organization that tracks the bill-paying habits of consumers

FINANCING YOUR FUTURETERMINOLOGY • Credit Report: A written record collected by a credit agency that tracks a borrower’s bill-paying habits • Revolving Credit: An open-ended account with a limit to how much one can borrow but no time limit for repayment: EXAMPLE is credit cards • Installment plan: A closed-end loan for a specific product such as furniture or appliances

FINANCING YOUR FUTURETERMINOLOGY • Capital Gains: A profit realized from the sale of property, stocks or other investments • Rule of 72: Divide the annual interest rate you expect to earn into 72 to know approx. how many years to double your money • Principal: The original amount borrowed • Federal Income Tax – Taxes subtracted from your paycheck to help fund the federal government

Understanding Credit Cards Avoiding and Eliminating Credit Card Debt

Credit Card Facts The Fed • American credit card debt averaged over $9,000 per card holder in 2008. • Total American consumer debt reached $2.45 trillion in March, 2010. • American households charged $855 billion to credit cards in 2010 - $69 billion past due

Credit Card Facts • Approx. 181 million Americans have at least one credit card – 1.5 billion cards were issued • U.S. Pop. In 2008 = Approx. 300 million • Of those 181 million consumers with credit cards, 2.3 million U.S. households filed for bankruptcy in 2009 • On average, the typical credit card purchase is 50-112% higher than if using cash

College Students and Credit Cards • In 2009, 78% of undergraduate college students had at least one credit card • 32% of students had 4 or more credit cards • As of 2008, the average college student graduated with 4 credit cards and one in seven owes more than $15,000

College Students and Credit Cards • The typical college student has $2,700 in credit card debt • ½ of students who drop out of school do so because of debt • Federal Reserve Report Shows Credit Card Companies Paid Colleges $83 Million to market credit cards to students

How much does credit cost? • If you bought a TV for $700.00 at 14.74% (average credit card interest rate) interest on a 36 month note, you would pay $872.33 for that television.

Credit Card Costs • If you took a credit card payment of $218 a month, and instead you invested in a growth mutual fund that averaged 12% APR, you could retire in 25 years with $1,354,930 saved. • Your credit card payment is not only costing you thousands in interest, but is prohibiting you from saving for your retirement.

Credit Does Matter and It Is Relevant to YOU • Credit cards give us freedom to buy what we want now and pay for it later • When it is used properly, it can be a powerful tool; when it’s abused, it can be destructive

Why learn about credit? • To help you prepare for the future • So you understand interest rates, credit cards, and how to control credit spending • To help you understand how to build credit without abusing it • You Will receive credit card applications in the mail—you need to know what the fine print means before you sign on

Advantages of Credit Cards • Convenience • Protection under Consumer Credit Act • Incentive Benefits • Credit limit

Disadvantages of Credit Cards • Excess consumer debt—use of a credit card is a loan • Too many—temptation to use increases • Credit limit

More Disadvantages of Credit Cards • Card companies charge huge interest rates • Average consumer credit card rate, overall market: 14.94% • Fees – Annual, Late fees, foreign fees for use outside the U.S. • Hidden rules in small print – Fixed rates can go up after one year

Even More Disadvantages of Credit Cards • Low minimum payment requirements • Encourages impulse buying • Increases your spending – Remember up to 112% more than with cash • Incentives cause you to spend more

Tucker’s Solution • PAY Cash

Another Tucker’s Solution • Quit doing what everyone else is doing – let them go broke while you make money

Establish Credit Without Cards • Rent • Cable bill • Phone bill • Insurance • Utility bills • Payment Reporting Builds Credit

What’s the Average Millionaire Look Like – The Millionaire Next Door • Most are college graduates • Most drive Fords, Chryslers or Chevrolets • Few millionaires lease cars • Only 17% attended a private school • Only 19% receive money from a trust fund • Most wear inexpensive clothes • Most are homeowners

How to Become a Millionaire • Start saving Immediately • Pay Cash • Go to College • Spend less than you earn • Create a budget with savings and investments • Start an emergency fund and use it ONLY for emergencies • Do not use Credit Cards (Tucker’s Rule) • Shop for nice looking but inexpensive clothes

How to Become a Millionaire • Save to pay cash for a used car and work your way up to pay cash for a new one • Beware of leasing a car • Don’t worry what others think of your financial actions – they will be in debt when you are a debt-free millionaire • Start saving NOW! • Start saving NOW! • Start saving NOW!

How to Become a Millionaire • MOST IMPORTANT • “If you will live like no one else, later you can live like no one else” Dave Ramsey