Download

1 / 78

800 likes | 1.16k Views

Chapter 3 – Demand, Supply and the Market. Prepared by : Takesh Luckho. What is a Market?. A market is a mechanism through which buyers comes in contact with sellers in order to complete a transaction. Market can take the form of

E N D

Chapter 3 – Demand, Supply and the Market Prepared by : Takesh Luckho

What is a Market? • A market is a mechanism through which buyers comes in contact with sellers in order to complete a transaction. • Market can take the form of • Any geographical location (for example Portobello Road Market in London) • Telecommunication Networks or Computer Networks (e.g Forex Markets or Stocks Markets)

Actual and Effective Demand • Actual Demand and Effective Demand • Actual demand is what you want (your ends) • Effective demand is what you want and this is backed by the desire/willingness to pay for it. • Hence in Economics when you talk about demand it mean the effective demand

Types of Demands • Individual Demand – Demand of goods and services by an individual/household • Joint demand – demand for goods that are jointly consumed (e.g Car and Petrol) • Competitive demand – demand competing goods that can provide the same satisfaction (e.g Tea and coffee) • Derived Demand – demand subjective to the demand of the final product (demand for factors like labour are derived demands) • Market Demand – Demand for all Individuals/ households

Types of Demands • Non Durable and Durable Good demand • Non-durable good – goods that are perishable (like vegetables, milk) • Durable good – goods that can last for long (furniture, electronics) • Company demand and Industry demand • Company demand – demand of a single firm • Industry demand – demand of all firms in the industry • Demand for consumer goods (consumed immediately) and producer goods (capital goods) • Short-Run and Long-Run demand

Demand: Definition • The demand for a good/service is the quantity that a household wants to buy during a period of time at a given price, providing this want is backed by the ability and willingness to pay. • From these information we can write a mathematical function to represent demand • Qxd = f (Px, Py, Pz, Y, Climate, Taste, Preferences, Expectations, Population,Etc..) • X is the good, Y is a substitute • Z is a complement and Y is household income

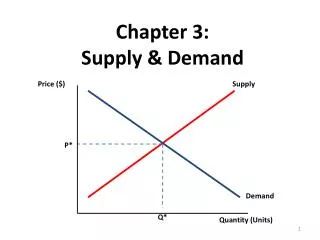

The Law of Demand • law of demand: Assuming Ceteris paribus Condition (all other things remain equal), as price of a good or service rises, its quantity demanded falls or as the price of a good or service falls, its quantity demanded increases. == > There is an inverse relationship between the price of a good and the quantity demanded of that good • Demand Function = Qdx = f(Px) i.e: Qdx = α - β Px • P Q or P Q

What can explain the downwards sloping shape of the demand curve? • Law of diminishing marginal utility • Income effect • Assuming that the price of a good goes down, you need to spend less money to buy the same amount of that good • Your real income goes up and with the same money in the pocket you can buy more of the good • Substitution effect • When price of a good falls, it becomes cheaper relative to its other competitors • A rational consumers will shift to the cheaper substitute

Exceptions to the law of demand • Giffen goods – a special type of inferior good that does not respect the law of demand. As price goes up, quantity also goes up. E.g Discounted products • Conspicuous consumption – like art or diamonds (bought by the rich). Its only when the price goes up that people buy such product • Expectation of a future rise in prices • Emergencies – like in war time period

Demand Curve Also known as the inverse demand curve as the diagram is the inverse of the demand function Qx =f(P) The demand curve has a negative slope, consistent with the law of demand. D

Effect of Changes in the Determinants of Demand: Movements and Shifts

Movement: Expansion of demand (Due to a fall in price) A B D

Movement: Contraction of Demand (due to a rise in Price) A B D

Shift in the Demand Curve • A change in any variable other than price that influences quantity demanded produces a shift in the demand curve. • Factors that shift the demand curve include: • Change in consumer incomes • Taste • Climate • Expectations • Population • Prices of related Complements and Substitutes

Prices of related goods • Complements - an increase in the price of a complement reduces the demand of the good, thus shifting the demand curve to the left. • Substitutes - an increase in the price of a substitute increases the demand of the good, shifting the demand curve to the right. • Income - an increase in income shifts the demand curve of normal goods to the right. • Number of potential buyers - an increase in population or market size shifts the demand curve to the right.

Demand curve shifts to the right This demand curve has shifted to the right. Quantity demanded is now higher at any given price. D

Demand curve shifts to the left This demand curve has shifted to the left. Quantity demanded is now lower at any given price. D

Important to Remember • A quick recap on Movement and Shift in the demand curve • A change in the price of the good will cause a movement along the demand curve • A change in any other variable will lead to a shift in the demand curve

Market Demand To get the Market Demand: Horizontal Summation across the individual Demand Curves

Consumer Surplus Price D • Consumer surplus is the difference between the maximum price a consumer is willing to pay and the actual price he do pay when buying the product • CS = Total Willing to pay – Actual Payment = 0DEQ – OPEQ = DEP Consumer Surplus E P Actual Expenditure O Q Qty

Supply: Definition • The supply of a good/service is the quantity that a firm will offer for sale during a period of time at a given price. • From these information we can write a mathematical function to represent supply • Qxs = f (Px, Po, Pf, T, Govt, Scale, Objectives, Expectations, Etc..) • X is the good, O is the price of other goods (rival or jointly supplied) • f are the factors of production, T is technology • Govt = Taxes or subsidy

The Law of Supply • law of supply: Assuming Ceteris Paribus Condition (other things remaining constant), as the price of a good rises, its quantity supplied will rise, and as the price of a good falls, its quantity supplied will fall. ===>There is a direct relationship between the price of the good and the quantity supplied of that good • In algebra, Qxs = f (Px) i.e, Qxs = α + βPx

The Law of Supply - cond • Why do producers produce more output when prices rise? • They make higher profits • Exception to the law of Supply • Non-profit maximising firms • Subsistence farming – as price rises farmer can sell less of the product to get the same revenue and keep the excess balance for their own consumption • Calculate market supply in the same way that we get market demand – sum of supply from all individual firm

Supply Curve The supply curve has a positive slope, consistent with the law of supply. S

Market Equilibrium: Determination Market Price • In economics, an equilibrium is a situation in which unconstraint variable do not tend/want to change - that is they are in a state of rest. • Hence, market equilibrium occurs where the free market price has no tendency to change, assuming ceteris paribus. • Let show Market Equilibrium on a demand and supply diagram and find the market price

At $ 35, Qty Demanded: 170 Qty Supply: 300 Excess supply (surplus in production) of 130 unit To much of the good on the market will cause the price to fall. Demand will expand, supply will contract until both reach 200 unit. At $30, neither demand nor supply want to change (they have reached a state of rest Market Equilibrium: Case of a Surplus The Market clearing process Price of tomatoes (dollars per kg.) 40 Supply Excess supply Case 1 35 1 2 3 30 Market equilibrium 25 Demand 0 200 170 300 Hence 200 unit is said to be the equilibrium quantity and the market (equilibrium) price is said to be 30

At $ 25, Qty Demanded: 220 Qty Supply: 100 Excess demand (shortage in production) of 120 Shortage of the good on the market will cause the price to rise. Demand will contact, supply will expand until both reach 200 unit. At $30, neither demand nor supply want to change (they have reached a state of rest Market Equilibrium: Case of a Shortage The Market clearing process Price of tomatoes (dollars per kg.) 40 Supply 35 30 Market equilibrium 5 4 6 Case 2 25 Excess demand Demand 0 100 200 220 Hence 200 unit is said to be the equilibrium quantity and the market (equilibrium) price is said to be 30

WHAT IS AN ELASTICITY? • An elasticity is a measure of the sensitivity of demand or supply to changes in their determinants. • In other words elasticity are said to be measuring the responsiveness of one variable (i.e one determinant) to changes in the quantity of the good being demanded/supplied. • The higher the value of elasticity, the greater will be the responsiveness of consumers to a change in the determinant. • Elasticities are often used to show the steepness/flatness of the demand or supply curve

Elasticity 3 basic types of demand elasticities: • Price elasticity of demand • Income elasticity of demand • Cross elasticityof demand

Price Elasticity of Demand (PED) • Price elasticity of demandmeasures the responsiveness of the quantity demanded of a good to a change in price of that good, assuming ceteris paribus conditions. • That is, it measures the rapidity and volume of the change in the quantity demand of that good as a response to change in its selling price.

Computing the Price Elasticity of Demand • The price elasticity of demand is obtained by dividing the percentage change in quantity demanded by the percentage change in prices.

Examples of Own Price Demand Elasticities • When the price of gasoline rises by 1% the quantity demanded falls by 0.2%, so gasoline demand is not very price sensitive. • Price elasticity of demand is -0.2 . • When the price of gold jewelry rises by 1% the quantity demanded falls by 2.6%, so jewelry demand is very price sensitive. • Price elasticity of demand is -2.6 .

Sign of Price Elasticity • According to the law of demand, whenever the price rises, the quantity demanded falls. Thus the price elasticity of demand is always negative. • Because PED is always negative, economists usually state the value without the sign. • Range of PED: - ∞≤ PED ≤ 0 or 0 ≤ PED ≤∞

Classifying Demand and Supply as Elastic or Inelastic • Demand is said to be elastic if the percentage change in quantity is greater than the percentage change in price. (i.e E < -1 or E > 1) • This means that the change in the quantity demanded is more than proportionate to the change in the price level • Demand is inelastic if the percentage change in quantity is less than the percentage change in price. (i.e E > -1 or E < 1) • This means that the change in the quantity demanded is less than proportionate to the change in the price level • An Inelastic Demand curve is steeper than an Elastic Demand Curve.

$5 1. A 25% increase in price... $4 50 100 2. ...leads to a 50% decrease in quantity. Elastic Demand- Elasticity is less than -1 Price Quantity

$5 1. A 25% increase in price... $4 90 100 2. ...leads to a 10% decrease in quantity. Inelastic Demand- Elasticity is greater than -1 Price Quantity

Special cases of Demand Curves • Perfectly Inelastic: PED = 0 • Quantity demanded does not respond to price changes. • Perfectly Elastic: PED = - ∞ • Quantity demanded changes infinitely with any change in price. • Unit Elastic: PED = - 1 • Quantity demanded changes by the same percentage as the price.

Demand $5 1. An increase in price... 4 100 Perfectly Inelastic Demand- Elasticity equals 0 Price Quantity 2. ...leaves the quantity demanded unchanged.

Demand $4 Perfectly Elastic Demand- Elasticity equals minus infinity Price At any price above $4, quantity demanded is zero. At a price of $4, quantity demanded is infinite. Quantity

$5 1. A 25% increase in price... $4 Demand 75 100 2. ...leads to a 25% decrease in quantity. Unit Elastic Demand (Rectangular Hyperbola)- Elasticity equals 1 Price Quantity

Income Elasticity of Demand (YED) • Income elasticity of demand measures the responsiveness of demand to a change in income. That is,how much the quantity demanded of a good responds to a change in consumers’ income. • It is computed as the percentage change in the quantity demanded of a good divided by the percentage change in household/individual income.

Computing Income Elasticity • If YED > 1 demand is income elastic (Luxury/Superior) • If YED > 0 and < 1 demand is income inelastic

Income Elasticity- Types of Goods - • Normal Goods (YED > 0) • Income Elasticity is positive. • YED > 1 Luxury Good • YED = between 0 and 1 Necessity • Inferior Goods (YED < 0) • Income Elasticity is negative. • Higher incomeraises the quantity demanded fornormal goodsbut lowers the quantity demanded forinferior goods.

Determinants of Income Elasticity • Goods consumers regard as necessities tend to be income inelastic • Examples include food, fuel, clothing, utilities, and medical services. • Goods consumers regard as luxuries tend to be income elastic. • Examples include sports cars, furs, and expensive foods. • Level of Income the consumer wants to spend on the good

Cross Elasticity of Demand (XED) • A measure of the degree of responsiveness of the demand for one good (X) to a change in the price of another good (Y)

Computing Cross Price Elasticity Of Demand Between Good X And Good Y

Goods which are complements: • Cross Elasticity will have negative sign (inverse relationship between the two) • Goods which are substitutes: • Cross Elasticity will have a positive sign (positive relationship between the two) Question: How would you interpret an Xed = 0 ? Any example you have in mind?

How to calculate Elasticities from a given Equation?? • If the demand for A is given by: QA = 100 - 2PA +PB + 0.5Y • Where PA = 15, PB = 5, Y = 100, Find whether demand is elastic or not. • Step 1: Calculate the Value of QA QA = 100 – 2(15) + 5 + 0.5 (100) = 125 • Step 2:Recall: PED = %Change in Qty A/ % Change in Price A • But when facing an equation, we can rewrite the formula as follows: PED = (dQA/QA) / (dPA/PA) = dQA/dPA . PA/QA • Step 3: dQA/dPA = the gradient w.r.t Price A = -2 • Hence, PED = dQA/dPA . PA/QA = -2 . (15/125) = -0.24Demand is inelastic Question: Find the Income and Cross Elasticity of Demand and say what it means??