Download

1 / 1

10 likes | 13 Views

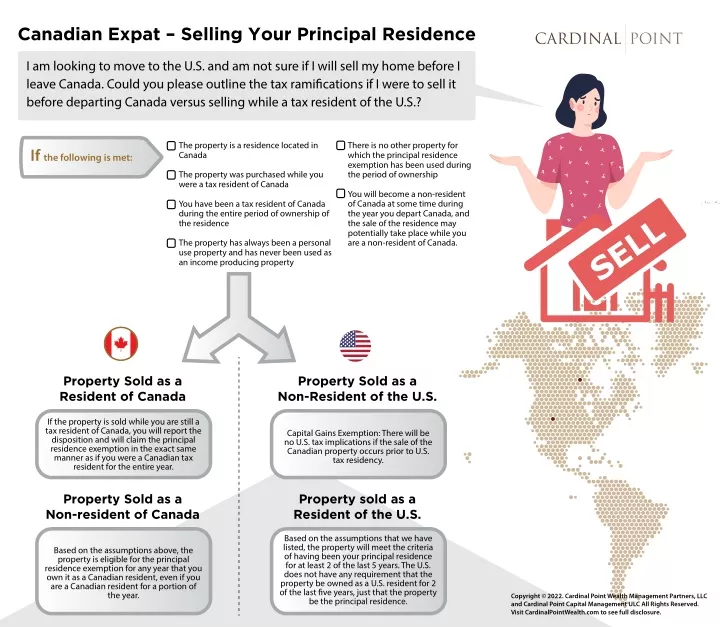

For individuals moving from Canada to the U. S. and planning to sell their Canadian home, there are different Canadian and U.S. tax implications. To avoid or minimize tax liability, specific criteria need to be met around the questions of whether tax residency is in Canada or U.S. when the sale occurs and if the home qualifies as a principal residence. If sold while still a Canadian tax resident, a status that can be maintained for a period beyond the moving date, exemptions apply. Additional compliance requirements need to be met when the property is sold

E N D

Canadian Expat – Selling Your Principal Residence I am looking to move to the U.S. and am not sure if I will sell my home before I leave Canada. Could you please outline the tax ramifcations if I were to sell it before departing Canada versus selling while a tax resident of the U.S.? There is no other property for which the principal residence exemption has been used during the period of ownership The property is a residence located in Canada If the following is met: The property was purchased while you were a tax resident of Canada You will become a non-resident of Canada at some time during the year you depart Canada, and the sale of the residence may potentially take place while you are a non-resident of Canada. You have been a tax resident of Canada during the entire period of ownership of the residence The property has always been a personal use property and has never been used as an income producing property Property Sold as a Resident of Canada Property Sold as a Non-Resident of the U.S. If the property is sold while you are still a tax resident of Canada, you will report the disposition and will claim the principal residence exemption in the exact same manner as if you were a Canadian tax resident for the entire year. Capital Gains Exemption: There will be no U.S. tax implications if the sale of the Canadian property occurs prior to U.S. tax residency. Property Sold as a Non-resident of Canada Property sold as a Resident of the U.S. Based on the assumptions that we have listed, the property will meet the criteria of having been your principal residence for at least 2 of the last 5 years. The U.S. does not have any requirement that the property be owned as a U.S. resident for 2 of the last fve years, just that the property be the principal residence. Based on the assumptions above, the property is eligible for the principal residence exemption for any year that you own it as a Canadian resident, even if you are a Canadian resident for a portion of the year. Copyright © 2022. Cardinal Point Wealth Management Partners, LLC and Cardinal Point Capital Management ULC All Rights Reserved. Visit CardinalPointWealth.com to see full disclosure.