Download

1 / 12

120 likes | 195 Views

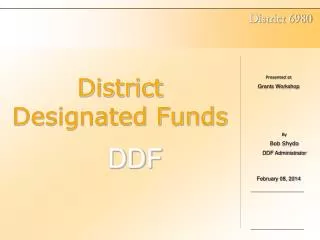

District Designated Funds. Presented at Foundation Seminar. By Bob Shydo DDF Administrator. DDF. September 10, 2011. Topics. District Designated Funds (DDF) How your club acquires DDF How your club can use DDF. DDF Allocation. DDF Funding Cycle.

E N D

District Designated Funds Presented at Foundation Seminar By Bob Shydo DDF Administrator DDF September 10, 2011

Topics • District Designated Funds (DDF) • How your club acquires DDF • How your club can use DDF

DDF Funding Cycle • Rotarians and clubs make contributions to the Annual Fund each year. • After 3 Years: • 50% of your club’s contributions goes to the World Fund • 50% of your club’s contributions comes back to the district as District Designated Funds (DDF) With Revenue Sharing • 80% of the District Designated Funds or 40% of your original contribution is allocated to your club by the district

DDF Allocation with Revenue Sharing $7,500 After 3 Years $3,750 $3,750DDF $3,000DDF 40% of original contribution $750DDF 10% of original contribution

Use of DDF With a DSG (District Simplified Grant) $100 Cash + $1,000DDF $500DDF $0 Matching Funds Total Funding - $1,600 DDF & Cash Club Out of Pocket Funding $1,600 Cash No Leveraging of Funds Grant DDF Funding Reimbursed

Use of DDF With A Matching Grant 3rd Year Allocation

DDF Allocation with Revenue Sharing $7,500 After 3 Years $3,7500 $3,000DDF $3,750DDF 40% of original contribution $750DDF 10% of original contribution

Use of DDF With A Matching Grant $100 Cash $500 Cash $3,000DDF $500 Cash $10,000DDF TOTAL $1,100 Cash $13,000DDF 3rd Year Allocation Matching Funds $550 Cash $13,000DDF Total Grant Funding $1,650 Cash $26,000DDF $27,650 TOTAL Leveraged Funding

DDF – Use it or Lose IT • If you have not allocated your clubs DDF to a Humanitarian Grant, Simplified Grant, GSE or Polio Plus by May 1, 2011 your club will forfeit its DDF and it will revert back to the District Use it or lose it.

Advantages of Annual Fund Contributions • YOUR Club can leverage its contributions • YOUR Club can control: • How • When & • Where contributions are used