Download

1 / 5

50 likes | 56 Views

u201cExtension of time lines for filing of Income-tax returns (Audit /Non-Audit cases both and Furnishing of belated/revised Return of Income for the Assessment Year 2021-22) and various reports of audit including Tax Audit/ Transfer Pricing Audit for the Assessment Year 2021-22 by the Central Board of Direct Taxes (CBDT)u201d<br>Read more at https://taxguru.in/income-tax/extended-due-dates-income-tax-return-tax-audit-tp-audit.html<br><br>

E N D

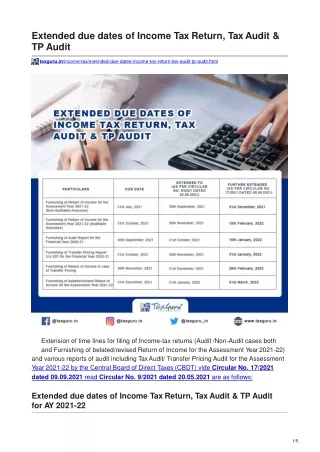

Extended due dates of Income Tax Return, Tax Audit & TPAudit taxguru.in/income-tax/extended-due-dates-income-tax-return-tax-audit-tp-audit.html Extension of time lines for filing of Income-tax returns (Audit /Non-Audit cases both and Furnishing of belated/revised Return of Income for the Assessment Year2021-22) and various reports of audit including Tax Audit/ Transfer Pricing Audit for the Assessment Year 2021-22 by the Central Board of Direct Taxes (CBDT) vide Circular No.17/2021 dated 09.09.2021read Circular No. 9/2021 dated 20.05.2021are asfollows: Extended due dates of Income Tax Return, Tax Audit & TP Audit for AY2021-22

31st October, 2021 Furnishing of Return ofIncome for the Assessment Year2021- 22 (AuditableAssessee) 30th November, 2021 15thFebruary, 2022 30th September, 2021 Furnishing of Audit Reportfor the Financial Year2020-21 31st October, 2021 15th January,2022 31st October, 2021 Furnishing of TransferPricing Report U/s 92E forthe Financial Year2020-21 30th November, 2021 31st January,2022 30th November, 2021 Furnishing of Return ofIncome in case of TransferPricing 31st December, 2021 28thFebruary, 2022 31st December, 2021 Furnishing ofbelated/revised Return of Income for the Assessment Year2021-22 31st January, 2022 31st March,2022 Clarification 1: Circular No. 09/2021and 17/2021shall not apply to Explanation 1 to section 234A of Income Tax Act, 1961 for furnishing of Return of Income U/s 139 (1) of the Act, in cases where the amount of tax on the total income as reduced by theamount as specified in clauses (i) to (vi) of Sec 139 (1) exceeds one lakhrupees. Clarification 2: Tax paid U/s 140A of the Act within the due date (without extensionunder Circular No. 9/2021 dated 20.05.2021and 17/2021 dated 09.09.2021) provided in that Act, shall be deemed to be the advancetax. Extract of the Explanation 1 to section 234A: In this section, “due date” means the date specified in sub-section (1) of section 139as applicable in the case of theassessee…… Extract of Sec 139(1) Return ofincome. 139. (1) Everyperson,— (a) being a company or a firm; or

(b) being a person other than a company or a firm, if his total income or the totalincome of any other person in respect of which he is assessable under this Act during the previous year exceeded the maximum amount which is not chargeable toincome-tax, shall, on or before the due date, furnish a return of his income or the income of suchother person during the previous year, in the prescribed38 form and verified in theprescribed manner and setting forth such other particulars as may be prescribed: Provided that a person referred to in clause (b), who is not required to furnish a return under this sub-section and residing in such area as may be specified by the Board inthis behalf by notification in the Official Gazette, and who during the previous year incurs an expenditure of fifty thousand rupees or more towards consumption of electricity or at any time during the previous year fulfils any one of the following conditions, namely:— is in occupation of an immovable property exceeding a specified floor area,whether by way of ownership, tenancy or otherwise, as may be specified by the Board in this behalf;or is the owner or the lessee of a motor vehicle other than a two-wheeled motorvehicle, whether having any detachable side car having extra wheel attached to suchtwo- wheeled motor vehicle or not;or [***] has incurred expenditure for himself or any other person on travel to anyforeign country;or is the holder of a credit card, not being an “add-on” card, issued by any bankor institution;or is a member of a club where entrance fee charged is twenty-five thousand rupeesor more,…… Kindly Refer to Privacy Policy & Complete Terms of Use andDisclaimer. AuthorBio

Name: Chandni Garg Qualification: CA in Job / Business Company: N/A Location: New Delhi, Delhi, India Member Since: 01 Jul 2021 | Total Posts:4 View Full Profile My PublishedPosts Latest Provisions related to E-Invoicing and QR Code underGST Late Fee & Interest under CGST Act, 2017 with latestAmendments GST Audit applicability for the Financial Year2020-21 View More Published Posts Join Taxguru’s Network for Latest updates on Income Tax, GST, Company Law, Corporate Laws and other related subjects. Join Taxguru Group onTelegram TELEGRAM GROUPLINK More Under IncomeTax «Previous Article

Next Article » OneComment Leave aComment Your email address will not be published. Required fields are marked*