Download

1 / 26

260 likes | 480 Views

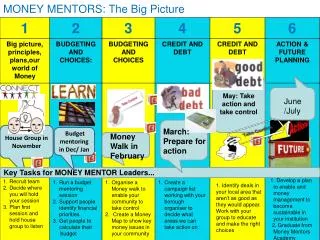

Money Mentors. Working together to enable optimum money management with individuals and across communities. Taking action – Feedback on May 2 nd. Where are we at with our work?. MONEY MENTORS: The Big Picture. May: Take action and take control. June/July. March: Prepare for action.

E N D

Money Mentors Working together to enable optimum money management with individuals and across communities

MONEY MENTORS: The Big Picture May: Take action and take control June/July March: Prepare for action House Group in November Budget mentoring in Dec/ Jan Money Walk in February Key Tasks for MONEY MENTOR Leaders... 1. Develop a plan to enable and money management to become sustainable in your institution 2. Graduate from Money Mentors Academy 1. Identify deals in your local area that aren’t as good as they would appear. Work with your group to educate and make the right choices

Aims of the session • Understand what a bank account is and what function it serves. • Distinguish between features of a bank account in order to make informed decisions. • Critically consider strengths and limitations of certain bank account features.

What is a bank account? Why can bank accounts be useful?

Name: • What does a bank account allow us to do – what functions does a bank account serve? • What bank account features do you think would be most important for (and why) • Alice: • Julian: • Tamar:

To pay bills regularly/easily and avoid getting into debt Access own money easily and safely Requirement by employer? Receive benefits, as well as money from friends and family Save money A facility to help you manage your everyday money Earn money Pay bills A healthy account can help us access other financial products/services Store money safely Cash cheques Budget money

Check this out!An Israeli woman's decision to keep her life savings in her mattress must have seemed like a wise one. But it came back to haunt her when her daughter threw the mattress out – along with $1m (£611,000) stuffed into the lining.

Overdraft: A facility allowing you to spend more money from your bank account than you have in it. The bank will usually charge you interest and sometimes other fees as well if you do this. Buffer zone: A small amount of credit/overdraft that a bank may give you. So you can get money from a cash machine even if you don’t have enough money in your account. Cheque book: A book of cheques which let you make a payment from your bank current account to someone else by writing a cheque in their favour. Telephone/online banking: Carrying out transactions on your bank account over the phone/over the internet. Direct debit: A way of paying bills from your current account. The money is taken directly from your account on specific dates. Counter service: A service which allows you to do your banking over the counter.

Julian is 30 on Wednesday, and it will be a double celebration because he has finished paying off all of his debts! Julian won’t be going too mad; he is still watching the pennies – he never wants to be in debt again! Tamar is a busy single parent to 6 year old Li. Tamar works full time, and organises for a special play scheme group to pick up Li from school each day. Tamar is currently saving to go on holiday. Alice is 72 and lives on her own. Her neighbour helps out regularly with shopping as Alice is partially sighted. Alice cant really see, so tries to avoid paper work at all costs.

Examples of those features of a bank account • Standing order: A way of paying bills from your current account. Your bank or building society pays the amounts on the agreed dates. The amount stays the same until you tell the bank or building society to change it. • Direct debit: A way of paying bills from your current account. The money is taken directly from your account on specific dates. • Cheque: A printed piece of paper used to make payments from your bank current account to someone else. You’ll get a supply of them in the form of a book. You’ll usually be sent a new book before you run out – see Cheque book. • Cheque book:A book of cheques which let you make a payment from your bank current account to someone else by writing a cheque in their favour. • Cheque guarantee card: Makes cheques up to the guarantee limit widely accepted, because the person you're paying is guaranteed to receive the money, whether or not you have enough in your account. • Cash card: Aplastic card that lets you get cash from your account through cash machines, at your bank or building society branch and by using cash back facilities at, for example, supermarket tills. You can also use it to make telephone or internet payments. • Debit card: A card issued by a bank or building society which you can use to withdraw cash or to pay for your shopping or services or to get ‘cash back’. The money is usually taken from your current account’s available balance.Interest:Interest refers to both the charge made by lenders on money you borrow from them and the amount earned by your savings. Interest can be variable (goes up or down) or be fixed. • Statements: A regular notification from your bank or credit card company that shows the payments in and out of your bank account or, for credit cards, shows what you've spent, what you owe, the minimum you must pay and the latest date you can pay it. • Online banking/Telephone banking: Carrying out transactions on your bank account over the phone/over the internet. • Buffer zone:A small amount of credit/overdraft that a bank may give you. So you can get money from a cash machine even if you don’t have enough money in your account. • Counter service: A service which allows you to do your banking over the counter. • Sharia-compliant: A bank account that runs in accordance with Islamic law and which offers a return on your money that is not interest. • Overdraft/overdrawn: A facility allowing you to spend more money from your bank account than you have in it. The bank will usually charge you interest and sometimes other fees as well if you do this. • Bank charges: A fee payable to banks for going overdrawn or for bouncing payments (Direct Debits, cheques or standing orders). The penalty amounts differ from bank to bank. • Automated credit transfer: Payment of wages, salary, benefits, pensions and tax credits directly into a bank or building society account (also known as direct credits).

Most people can obtain People with poor credit ratings First step towards a current account Don’t want to get into debt Basic bank accounts

NO cheque book. • Bank won’t bail you out for having a DD coming out when there is no money in account. • NO overdraft – but a buffer zone. • No interest on credit balances. • Most allow you to have online banking/telephone banking • Most will allow SO and DD to be set up • Some will allow a debit card • Most will allow a cash card

Current Accounts • ...also for managing your day-to-day money, but with more features than a basic bank account. • There are special accounts for students. • Some current accounts pay you interest if you are in credit, but a savings account will usually pay a higher rate

Many offer a cheque book, cash card, and cheque guarantee. • Many accounts allow direct debit and standing orders to be set up. • Can offer overdraft facilities. • Need to be aware of interest, fees and charges. • May be likely to offer an incentive for opening. • Can offer internet and phone banking.

Saving Account • for putting away money that you’d like to save, say for furniture, a holiday or emergencies. • It often pays a higher rate of interest than current accounts, so your money grows.

For putting away money that is not needed immediately, for safe keeping and to earn interest. • Good for saving for a holiday or emergencies. • Besides the fact that you will be less likely to spend it, putting your money in a savings account is safer because it is insured.

Saving Account Basic bank Account Current Account Packaged Current Account Post Office Account Accounts for Young People Credit Union Account

What happens when things go wrong?

Suggested steps include: Do your homework (reading and organisation of relevant documents) Communicate and complain to your bank or creditor. Log information and communication Time and patience The financial ombudsman

Useful contact information Financial Ombudsman It’s our job to sort out individual complaints that consumers and financial businesses haven't been able to resolve themselves. We were set up by parliament to do this – as independent experts – and our service is free to consumers. We can look at complaints about a wide range of financial matters – from insurance and mortgages to investments and credit. Each year we deal with almost a million enquiries and settle over 150,000 disputes. We’re completely independent and impartial. This means that when we decide a complaint, we look carefully at both sides of the story and weigh up all the facts. Phone: open 8am to 6pm, Monday to Friday 0800 023 4567free for people phoning from a "fixed line" (for example, a landline at home) 0300 123 9 123free for mobile-phone users who pay a monthly charge for calls to numbers starting 01 or 02 we'll be happy to phone you back, if you're worried about the cost of calling us Email: Complaint.info@financial-ombudsman.org.uk Write: The Financial Ombudsman ServiceSouth Quay Plaza183 Marsh WallLondon E14 9SR Other useful contacts: Consumer Credit Counselling Service (CCCS):The Foundation for Credit Counselling is the umbrella charity for Consumer Credit Counselling Service in the United Kingdom. Through its free national telephone service, ten regional centres and online CCCS Debt Remedy, CCCS is able to help people with debt problems wherever they live. Call 0800 138 1111 The National Debt Line:The helpline that provides free confidential and independent advice on how to deal with debt problems. Call 0808 808 4000. The Money Advice Service: Here to help everyone manage their money better. We do this by giving free, clear, unbiased money advice to help people make informed choices – this is done over the phone or in person. Check out our website at which included lots of information around banking! Moneyadviceservice.org.uk

NEXT STEPS: Complete final Money Mentor session on Bank Accounts: June 11th 2011 – Opportunity to hand in completed Portfolio of Learning and evaluate with London Citizens June 28th 2011 – Graduation Ceremony

Graduation ceremony Date: Tuesday 28th June Location: The Guildhall, Gresham Street, EC2V 7HH

EVIDENCE FOR YOUR PORTFOLIO Session 1 · Listening form from your house group · Photo of house group · Evaluation notes/ personal reflections on the house group · Feedback from organizer who attended your house group Session 2 • · Completed budget diaries • · Income and expenditure forms • · Evaluation notes/ personal reflections on budget mentoring • Session 3 • · Evidence of money mentor community walk • · Completion of money mentor walk eye-spy booklet (to be created) • Session 4 • · Photo of training session • · Evaluation notes/ personal reflections on the training session • · Feedback from organizer who attended your training session • Session 5 • · Photo of training session • · Evaluation notes/ personal reflections on the training session • · Feedback from organizer who attended your training session

Date to celebrate, evaluate and hand in portfolios! Saturday June 11th 2011 London Citizens Office 112 Cavell Street E1 2JA