Download

1 / 19

190 likes | 305 Views

Legal forms Detailed information. School Year 2008/2009. How to set up a company? Five major steps. Prepare a business plan Enter into a partnership agreement if necessary

E N D

Legal forms Detailed information School Year 2008/2009

How to set up a company?Five major steps • Prepare a business plan • Enter into a partnership agreement if necessary • Register your company with the trade office. They will pass your registration on to tax office, IHK (Chamber of Commerce and Industry), employment center, and employers' liability insurance association • Have your company entered in the register of companies if applicable • Check if you must meet specific prerequisites (e.g., permit from building authorities)

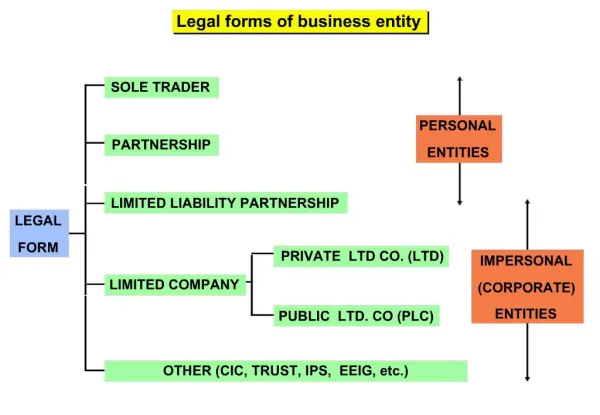

Which legal forms are there? Sole proprietorship General partnerships Corporations Sole proprietor GbR OHG KG (GmbH & Co. KG) GmbH AG (Small AG)

Sole proprietorship Advantages of sole proprietorship Drawbacks of sole proprietorship Prerequisites • Owner-managers (people running a small business, tradesmen, service providers, liberal professions) • To be entered in register of companies as "Istkaufmann" • Is automatically created unless you choose a different legal form • For merchants: may enter a fancy name in the register of companies (not possible for people running a small business) • No minimum capital required • No partnership agreement required • Owner-managers are fully liable with their entire (personal) assets + – + + +

! GbR (Gesellschaft bürgerlichen Rechts)—civil law association Prerequisites Advantages of a GbR Drawbacks of a GbR • Informal partnership agreement involving at least two persons • Must have a specific purpose … • … with each partner to the agreement promising to pursue this purpose • GbR norms are subsidiarily applicable, i.e., other legal structures under general partnership law must not be applicable • Oral agreement would do (not advisable) • No minimum capital required • Much room for the individual partners' competences • No formalities required • Each business partnership can be a GbR (e.g., liberal professions, physician partnerships, etc.) • As regards the company's debts vis-à-vis creditors, the partners are jointly and severally liable with their entire business and personal assets • Much room for the individual partners' competences • Liability extends five years beyond the time when a partner leaves + – + + + – + –

OHG (offene Handelsgesellschaft)—general partnership Prerequisites Advantages of an OHG Drawbacks of an OHG • For merchants only • Informal partnership agreement involving at least two persons • To be entered in register of companies • Purpose must be to run a commercial business under a joint name(= name of the company) • The partners must not limit their liability in the partnership agreement • Informal partnership agreement will do • No minimum capital required • Due to personal liability, a better image with banks and business partners than a GmbH • As regards the company's debts vis-à-vis creditors, the partners are jointly and severally liable with their entire business and personal assets • Liability extends five years beyond the time when a partner leaves • New partner is fully liable for debts incurred before (s)he entered the company + – + + – –

KG (Kommanditgesellschaft)—limited partnership Prerequisites Advantages of a KG Drawbacks of a KG • Applicable on top of the prerequisites for OHGs • One or more general partners • One or more limited partners • Advantages on top of those of OHGs • Limited partner: noliability beyond capital contribution, when capital contribution has been made • Personal liability does not apply when capital contribution has been made • Instead of applying for a loan, it's easier to raise capital via capital contributions from (limited) partners • As regards debts vis-à-vis creditors, general partner is liable with entire personal assets • Limited partner's liability does not extend beyond his/her capital contribution (personal liability does not apply when capital contribution has been made) – + – + +

GmbH (limited liability company) Prerequisites Advantages of a GmbH Drawbacks of a GmbH • At least 1 partner • €25,000 equity capital (50% cash or non-cash contribution when the company is founded) • Setup must be notarized • Partnership agreement must be notarized • To be entered into register of companies by notary public • Registration as business • At least 1 managing director • Only one person needed to set up a GmbH • No liability beyondcapital contribution, hence • no personal liability of the partners • Non-cash contribution to equity capital also possible (special conditions) • High equity capital • Cost of notary public • Changes require notarization • Prior to entry into the register of companies, both partners and acting persons can be held liable • Dissolution of the GmbH is a complex process • Mandatory reporting and accounting + – – + – + – + – –

As regards a GmbH, please take note of the following Please note! • If half of the equity capital is lost, the partners must be informed • If all of the equity capital is lost, management must open insolvency proceedings against the GmbH's assets without undue delay • Any violation is punishable with imprisonment up to three years

GmbH legislation modernized with new law1 "Starter" version of GmbH(§ 5a GmbHG) Important changes • No minimum nominal capital for the establishment of a new business (1€ and up) • Simpler GmbH establishment with use of model articles of association • Cost savings • Faster registration with electronic application • Administrative headquarters may be transferred abroad • Limited liability entrepreneurial company • No minimum nominal capital needed, but consequently no full profit distribution • Minimum nominal capital for a GmbH (€25,000) must be gradually saved up 1. Act to Modernize the Law Governing Private Limited Companies and to Combat Abuses (Gesetz zur Modernisierung des GmbHRechts und zur Bekämpfung von Missbräuchen / MoMiG)

Addendum: GmbH & Co. KG Prerequisites Advantages Drawbacks • General partner = GmbH • At least one limited partner • Informal partnership agreement • To be entered into register of companies by notary public • Registration as business • Combines the advantages of GmbH and KG • Broad capital basis provided by limited partners when they make their capital contributions • GmbH needed to set up the GmbH & Co. KG • As a general partner, the GmbH is liable with all its assets • Requires high level of trust in general partner as he has sole powers of representation + – + – –

AG (corporation) Prerequisites Advantages of an AG Drawbacks of an AG • At least 1 shareholder • Equity capital of €50,000 • To be entered into register of companies • Partnership agreement to be notarized • Statutory report required • The process of setting up the AG is reviewed by board of directors, supervisory board, and an auditor or tax accountant (or by notary in case of formation of stock corporation by cash subscription) • Liability is limited to the corporation's assets • Entrepreneur can be sole shareholder and managing director • Shares easy to transfer • Marketable form of organization • High equity capital • High administrative effort to set up an AG • Transcription of the general assembly must be notarized • According to § 121 section 3 AktG, the invitation to the general assembly must be published as specified in the company's articles of incorporation • Very high current cost (audit, three bodies in parallel, namely board of directors, supervisory board, and general assembly) + – – + – + + – –

Addendum: the small AG1 Prerequisites Advantages of an AG Drawbacks of an AG • At least 1 shareholder • Equity capital of €50,000 • To be entered into register of companies • Statutes to be notarized • Liability is limited to the corporation's assets • Entrepreneur can be sole shareholder and managing director • Shares easy to transfer • Invitation to general assembly simply by registered mail as long as all shareholders are known to the company by name (§ 121 section 4 AktG) • High equity capital required • High administrative effort to set up a small AG + – + – + + 1. Small in this context means: "small " number of shareholders and not listed on the stock exchange

Tax basics Tax = tax rate ×base for tax tax burden • Taxes on income • E.g., income tax, corporate tax, or trade tax • Depending on income produced • Excise taxes • E.g., sales tax, petroleum tax, or electricity tax • Property taxes • E.g., land tax

Most important taxes for companies Income tax Trade tax Corporate tax • Depending on personal income, between 15% and max. 45% • May vary from community to community, ca. 14% on average in Germany • Sole proprietorship and general partnership are subject to trade tax only when their business is a trade and their trade income exceeds €24,500 (tax allowance: only the amount exceeding the allowance is taxable) • No tax allowance for corporations • Only corporations (i.e., GmbH or AG) • No tax allowance • Since 2008: 15% Companies must also pay a solidarity surcharge of 5.5% on income and corporate taxes

Tax comparison for different kinds of companies The tax system is highly complex and frequently changed, it is hence advisable to check again on the Internet

Corporation 2009 Profit 100.00 - trade tax (400%) 14.00 = profit after trade tax 86.00 - corp. tax (15%) 15.00 - so. surcharge (5.5%) 0.83 = after-tax profit 70.17 Tax burden: 29.83 Dividend 70.17 - income tax (25%) 17.54 - so. surcharge (5.5%) 0.96 After-tax earnings 51.67 Tax burden: 48.33 Tax burden: 48.30 Tax burden: 29.77 A partnership and a corporation in comparison Partnership 2009 Profit 100.00 - trade tax (400%) 14.00 = profit after trade tax 86.00 - income tax In (28.25%) 28.25 + trade tax credit (380%) 13.30 - so. surcharge (5.5%) 0.82 = after-tax profit 70.23 Profit withdrawal 70.23 - income tax (25%) 17.56 - so. surcharge (5.5%) 0.97 After-tax earnings 51.70

What's a trade? • A trade … • … is a legally recognized, independent entity with a visible business activity • … is designed to generate profit • … is pursued on a regular basis and for a certain period of time • … does not belong in the liberal professions (e.g., doctors, lawyers, artists, most UAS/university degrees) • … is subject to the HGB • A small trade … • … is a trade producing sales of less than €17,500 (incl. sales tax) in the firstyear … • … and reporting sales of less than €50,000 in the year under review and less than €17,500 in the preceding year (incl. sales tax) • … is not subject to the HGB in the beginning