Download

1 / 10

100 likes | 192 Views

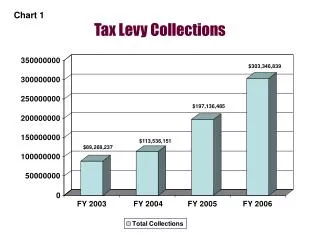

Tax Collections, Exemptions, and Reform. Thomas Baunsgaard Presentation to the DPG Main January 15, 2013. Part I. Tax revenue improvement: Providing fiscal space. Source: Tanzania Revenue Authority and IMF estimates. Part II. Increase in exemptions outpaced revenue …signs of a turnaround?.

E N D

Tax Collections, Exemptions, and Reform Thomas Baunsgaard Presentation to the DPG Main January 15, 2013

Part I. Tax revenue improvement: Providing fiscal space Source: Tanzania Revenue Authority and IMF estimates

Part II. Increase in exemptions outpaced revenue …signs of a turnaround? Source: Tanzania Revenue Authority and IMF estimates

Exemption creep in domestic VAT Source: Tanzania Revenue Authority and IMF estimates

Two-thirds of exemptions from VAT on imports and domestic transactions Source: Tanzania Revenue Authority

Other tax exemption ratios Source: Tanzania Revenue Authority and IMF estimates

Part III. VAT Reform • The Government target of a gradual reduction in tax exemptions to 1 percent of GDP (GBS PAF)… • …can only be achieved by reducing VAT exemptions • Minister Mgimwa announced a review of the VAT “to conform to international best practice” (Budget speech, June 2012) • IMF missions on VAT policy in 2011 and 2012; legal expert is working with the government on a draft VAT bill

Goal for VAT redrafting To reform the VAT into a more equal and equitable tax that is: ¶ more revenue productive ¶ easier to comply with and to administer, and ¶ provides a more business and investment friendly climate A modern broad-based VAT: Single rate; broad tax base; destination based General tax on consumption by taxing value added with credits/refunds of input tax

Aim: Rationalization of exemptions Goal: Replace extensive zero-rating and exemption schedules with simpler regime. Limit zero-rating to exports Why exempt? • On equity grounds • Basic needs (some food items) • Health & education • Land, residential property (except sales of new residential property) • Non-commercial supplies by approved non-profits • Non-commercial activities of government entities • On technical, practical grounds • Financial services, except if provided for an explicit fee

Aim: Rationalization of exemptions (cont’d) • Import exemptions • Goods for which the supply would be exempt • Goods in transshipment, containers • Donations, disaster relief goods • Imports under international agreements (treaties, financing agreements); refunds for VAT incurred domestically • To counter exemption creep, need improved VAT refund mechanism • Exemptions only through legislation – reduce discretion