Download

1 / 21

210 likes | 309 Views

This comprehensive guide covers the disposal of fixed assets, policies for managing fixed assets, journal entries, and detailed examples for calculating depreciation using straight-line and written-down value methods.

E N D

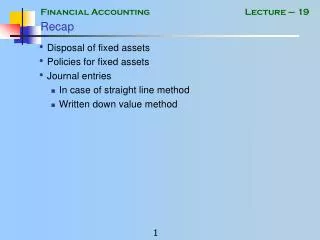

Recap • Disposal of fixed assets • Policies for fixed assets • Journal entries • In case of straight line method • Written down value method

In case an asset is not complete at the time preparing the balance sheet then the costs incurred on that asset till the date of balance sheet are shown in “Capital Work In Progress Account”

“Capital Work In Progress Account” is shown as a separate head in the balance sheet.

At the time of completion all the costs are transferred to fixed assets account from capital work in progress account. • Journal entry • Debit Fixed Asset (relevant account) • Credit Capital Work in Progress Account

All costs incurred on the asset until it is brought to the state of its intended use are included in its cost. • These costs may include: • Freight • Cost of assembling • Financial costs • Legal cost

Example 1 • A machine costs Rs. 500,000. • Its useful life is five years. • At the end of five years its residual value is expected to be Rs. 30,000. • At the end of four year the machine was sold for Rs. 31,000. • Depreciation is charged on the basis of use. • Required. • Show the calculations of depreciation for the four years using both reducing balance and straight line method. • For WDV assume depreciation rate to be 50% • Calculate the profit / loss on disposal in both cases

Straight Line Method Depreciable Amount = 500,000 – 30,000 = 470,000 Annual Depreciation = 470,000 / 4 = 117,500 Annual Depreciation = 470,000 / 5 = 94,000

Example 2 • Following information is available for Machinery Account in Year 4: • One machine purchased on Jul 1, Year 1 for Rs. 50,000 • One machine purchased on Jan 1, Year 2 for Rs. 75,000 • One machine purchased on Apr 1, Year 3 for Rs. 100,000 • Machine 1 is disposed off on Sep 30, Yr 4. • Depreciation is charged at 25% reducing balance method.

Example 2 • Show the calculations of depreciation on machinery for the four years, applying following policies: • (1) Depreciation is charged on the basis of use • (2) Full depreciation on the year of purchase and no depreciation in the year of disposal.

Year 1: One machine purchased on Jul 1, Year 1 for Rs. 50,000 • Policy 1 WDV Opening Balance 0 Purchase of Machine 50,000 50,000 Depreciation (50,000 x 25%) x 6/12 (6,250) WDV Closing Balance 43,750

Year 2: One machine purchased on Jan 1, Year 2 for Rs. 75,000 • Policy 1 WDV Opening Balance 43,750 Purchase of Machine 75,000 118,750 Depreciation (118,750 x 25%) (29,688) WDV Closing Balance 89,062

Year 3: One machine purchased on Apr 1, Year 3 for Rs. 100,000 • Policy 1 WDV Opening Balance 89,062 Purchase 100,000 189,062 Depreciation (89,062 x 25%) (22,265) Depreciation (100,000 x 25%) x 9 / 12 (18,750) WDV Closing Balance 148,047

Year 4: Machine 1 is disposed off on Sep 30, Year 4 • Policy 1 WDV Opening Balance 148,047 Dep. Machine 1 (4,614) Dep. Others (148,047 – 24,609) x 25% (30,860) 112,573 WDV of Asset Disposed (19,995) WDV Closing Balance 92,578

WDV of machine sold in Year 4: Cost Year 1 50,000 Dep. Year 1 (50000 x 25 %) 6/12 6,250 WDV Year 1 43,750 Dep. Year 2 (43750 x25%) 10,938 WDV Year 2 32,812 Dep. Year 3 (32,812 x 25%) 8,203 WDV Year3 24,609 Dep. Year 4 (24,609 x 25%) x 9 / 12 4,614 WDV Year4 19,995

Year 1: One machine purchased on July 1, Year 1 for Rs. 50,000 • Policy 2 WDV Opening Balance 0 Purchase Cost 50,000 50,000 Dep. (50,000 x 25%) (12,500) WDV Closing Balance 37,500

Year 2: One machine purchased on Jan 1, Year 2 for Rs. 75,000 • Policy 2 WDV Opening Balance 37,500 Purchase Cost 75,000 112,500 Dep. (112,500 x 25%) (28,125) WDV Closing Balance 84,375

Year 3: One machine purchased on Apr 1, Year 3 for Rs. 100,000 • Policy 2 WDV Opening Balance 84,375 Purchase Cost 100,000 184,375 Dep. (184,375 x 25%) (46,094) WDV Closing Balance 138,281

Year 4: Machine 1 is disposed off on Sep 30, Year 4 • Policy 2 WDV Opening Balance 138,281 WDV of Disposed Off Machine (21,094) 117,187 Dep. (117,187 x 25%) (29,297) WDV Closing Balance 87,890

Machine Disposed Off in Year 4 Cost Year 1 50,000 Dep. Year 1 (50000 x 25 %) 12,500 WDV Year 1 37,500 Dep. Year 2 (37500 x25%) 9,375 WDV Year 2 28,125 Dep. Year 3 (28,125 x 25%) 7,031 WDV Year 3 21,094