Download

1 / 40

420 likes | 592 Views

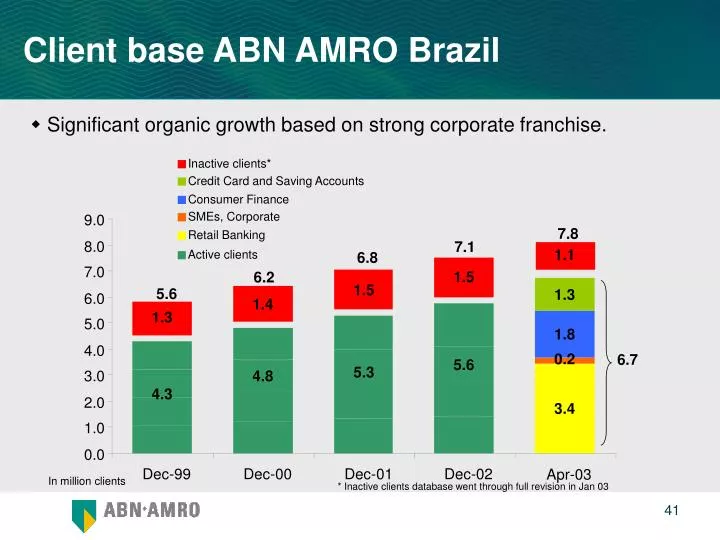

Client base ABN AMRO Brazil. Inactive clients*. Credit Card and Saving Accounts. Consumer Finance. SMEs, Corporate. 9.0. 7.8. Retail Banking. 8.0. 7.1. 1.1. Active clients. 6.8. 7.0. 1.5. 6.2. 1.5. 5.6. 1.3. 6.0. 1.4. 1.3. 5.0. 1.8. 4.0. 0.2. 6.7. 5.6. 5.3. 3.0. 4.8.

E N D

Client base ABN AMRO Brazil Inactive clients* Credit Card and Saving Accounts Consumer Finance SMEs, Corporate 9.0 7.8 Retail Banking 8.0 7.1 1.1 Active clients 6.8 7.0 1.5 6.2 1.5 5.6 1.3 6.0 1.4 1.3 5.0 1.8 4.0 0.2 6.7 5.6 5.3 3.0 4.8 4.3 2.0 3.4 1.0 0.0 Dec-99 Dec-00 Dec-01 Dec-02 Apr-03 In million clients • Significant organic growth based on strong corporate franchise. * Inactive clients database went through full revision in Jan 03

Client base - integrated approach • Synergies currently realised between Retail and Corporate/WCS are significant. Retail: acquisition mix 2002 (%new clients) Revenue synergies: largely realised • Front office: • Increased benefit from SME platform • Payroll product offer to Corporate/WCS clients: • 6,240 payroll relationships; 920,000 individual clients • Important improvements through co-ordinated selection criteria and pricing • Acquisition of Retail clients through corporate relationships (Payroll/PAB): • 48% of new retail clients acquired through corporate relationships • Improvements in retail client mix through co-ordinated selection criteria • Potential growth through supply-chain banking initiatives

Client segmentation • Monthly Income • Premium Clients: > R$4,000 • Special Clients: R$4,000 - R$1,200 • Classic Clients: < R$1,200 Breakdown of Active Checking Accounts (2003) Breakdown by Affinity Group (2003)

Client segmentation • Client segmentation currently being implemented is based on each segment revenue potential and is focused in: • Providing products and services in-line with customer expectations • Strengthening relationship management capabilities Average account revenue per segment Index: Avg Classic revenue = 100

Client loyalty vs results Source: Gallup, 2002

Client loyalty vs relationship approach Source: Gallup, 2002

Client loyalty • Around 34% of clients are totally satisfied with Banco Real. The evolution in Special and Premium segments is expressive. Source: Gallup, 2002

Client loyalty L3 L3 Satisfaction 34% Satisfaction 32% Continue 33% Continue 35% Recommend 34% Recommend 39% • Besides “overall satisfaction”, clients from segments Special and Premium intend to keep the relationship with Banco Real and would probably recommend the Bank to others, which reflects their Loyalty Jun/2002 ________ L3 = 15% Nov/2002 ________ L3 = 17% Source: Gallup, 2002

Our focus region • ABN AMRO Brazil focus region for organic growth: the marked area, the States’ capitals and Brazil’s main cities.

Sudameris - The rationale • The consolidation in the Brazilian banking market is continuing. Since Dec/01, Bradesco has acquired Banco Mercantil de São Paulo, Banco Cidade (SMEs), Banco do Estado do Amazonas, Banco Ford and BBVA Brazilian operation, whilst Itaú acquired Banco Fiat and Banco BBA. • Considering size of portfolio, excellent client reach and high concentration of branches in the state of São Paulo (the wealthiest state of Brazil where Banco Real had historically lower market share), Sudameris was the best option to fit ABN AMRO’s growth and strategic goals. • Sudameris improves ABN AMRO’s market share immediately, especially in some specific segments like SMEs and upscale clients. • The integration of Sudameris operations will enhance ABN AMRO’s competitive positioning.

Sudameris - The Final Agreement • ABN AMRO finalized the terms of the agreement with Intesa, last June 13th, to buy its 94.57% of the total share capital of Banco Sudameris Brasil S.A.. The proposal valued Intesa’s stake at R$ 2.3bln. The acquisition will be phased over three years and fully funded in Brazil. • Banco ABN AMRO Real S.A (“AAR”) will pay R$526mln in cash and proceed with a share swap with shares of AAR. In this structure Intesa will become circa 12.89% shareholder of AAR (to be confirmed at closing). The exit for Intesa can be summarised as follows: • Intesa will have the right to swap their shares in AAR for shares of ABN AMRO Holding N.V. (“AA Holding”) in three annual installments. Intesa’s price for the put right : the book value of Intesa’s stake in AAR, multiplied by 1.82 • ABN AMRO Participações Financeiras S.A. (“AA Part”, the Brazilian holding company of AAR) will have the right to call Intesa’s shares in AAR at anytime. AA Part’s price for the call right: equivalent to Intesa’s put right, however ABN AMRO call can be exercized at anytime.

Clients and Branch Network • Sudameris has approximately 500,000 clients (380,000 current accounts), concentrated in our Focus Region (especially in São Paulo). Sudameris’ clients are mainly upscale and the bank is known for its focus on SME’s. • 34% of ABN AMRO Brazil’s retail branch network and 53% of Sudameris’ branch network are concentrated in São Paulo state. Focus Region

Branch network expansion • Growth focused in the most economically developed regions of the country • Presence in all state capitals • Although acquisitions such as Bandepe and Paraiban are focused on client acquisition, they also contribute to increase the number of branches. Expected Evolution in Number of Branches (excluding PABs)

Non-traditional distribution channels • Non-branch transactions are growing regularly, reducing costs and increasing client convenience. *Non Branches include transactions through direct channels and operational centres

Infrastructure and ATM network • Investments made since 1998 created competitive infrastructure to Banco Real, which will be key to integrate Sudameris. Number of ATM’s

Call center • Call center implemented in Brazil in 1985 • 7 days X 24 hours • Full service • Inbound and proactive outbound activities • 450 workstations • 1,290 people • 14 million calls per month • Part of Call center transactions are migrating to Real Internet Banking *Calls answered within 20 seconds **Assisted calls

Internet banking • Real Internet Banking was started on February 2000. Since then, nearly 30% of Real’s current account clients have become users of this service. Number of Transactions done through internet (in mln) Number of Real Internet Bkg users (in thd)

Corporate internet banking • Real Internet Empresa (Banco Real’s office bank through internet) was launched on August 2000. More than 95 thousand corporate and SME clients of Real are users of this service. Number of companies using Real Internet Empresa

Brazil: contribution to Global C&CC • Brazil accounted for 9% of C&CC’s global result in 1Q03. C&CC Pre-Tax Profit (1Q03)

C&CC Brazil: gross revenues Evolution total C&CC Brazil gross revenues (NIR + fees) R$ million

C&CC Brazil: fee income retail Evolution fee income Retail C&CC Brazil R$ million

C&CC Brazil: total expenses Evolution total expenses C&CC Brazil R$ million

C&CC Brazil: risk management • Sustainable growth in a controlled environment Credit scoring : Reducing manual approvals of credit limits # of monthly approvals in thd

C&CC Brazil: risk management • Sustainable growth in a controlled environment Actions taken have avoided further deterioration of the credit portfolio despite the 2002 adverse economic scenario... (past due loans > 15 days, % of total credit portfolio)

C&CC Brazil: risk management • Sustainable growth in a controlled environment ...The effective credit losses (total credit expenses) are under control & the C&CC runs with sound spread (amounts in R$ million) Qtrly evolution of total credit expense and revenue as percentage of loans Qtrly total credit expenses and revenues evolution

Appendix 1 Background

Appendix 2 Sudameris Acquisition

Sudameris - Background • On 4Q01 ABN AMRO approached Intesa showing interest in Sudameris. • On December 2001, Intesa and Banco Itaú entered into an agreement for the purchase of Sudameris. • On November 2002, the parties broke up the negotiations since they could not reach a satisfactory agreement in connection with the purchase price adjustment. • ABN AMRO approached Intesa again on December 2002. • Further to subsequent discussions with Intesa, a new proposal has evolved and finally an agreement was reached on April 16th.

Sudameris Financials R$ mln R$ mln

Appendix 3 C&CC Brazil - Financial Performance