Download

1 / 13

130 likes | 256 Views

‘The Transformation of AWB’ Andrew Lindberg, Managing Director. A tough industry: global wheat market realities. Volatile trade flows. ‘Flat’ global demand. World Wheat Prices Over Time. Global trade distorted. Australian growers disadvantaged.

E N D

‘The Transformation of AWB’ Andrew Lindberg, Managing Director

A tough industry: global wheat market realities Volatile trade flows ‘Flat’ global demand World Wheat Prices Over Time Global trade distorted

Australian growers disadvantaged Domestic Consumption As % Total Wheat Production: 1995-2000 (%) High Exposure To World Price Volatility Wheat Producer Subsidy Estimates: 1999-2001 (A$/tonne) Unprotected By Subsidies

Global wheat trends Source: USDA, May 2004

Australia’s competitive position in the world wheat markets Total wheat production for 2003-04(e) and 2004-05(f) Major exporters – estimated wheat market share for 2004-05(f) Source: USDA, May 2004

AWB Evolution 2003 Landmark acquisition “Shareholders’ equity has grown from around $600 million in 1999 to over $1 billion as at 31 March 2004”. 2001 Listed on ASX 1999 Privatised • - Wheat Industry Fund converted to B class shares • - A class shares issued to wheat growers • - Government guarantee of AWB borrowings removed 1998 Corporatised 1989 Domestic market deregulated and Wheat Industry Fund established 1939 Australian Wheat Board establishedas a statutory authority

Australian Wheat Board to AWB Limited FROM… • a statutory authority • government owned and backed • wheat marketing authority TO… • public company, listed in August 2001 • 75% grower owned; 25% institutional investors • grain company Market capitalisation: Approx. $1.7 billion Shares on issue: 338 million Shareholder’s equity: Approx. $1 billion Index inclusion: S&P/ASX 100 (75% IWF)

AWB's success - the 'differentiation' strategy Creating Origin-Specific Demand • Developing new markets for higher quality wheat Differentiating Products • Increased proportion of high quality wheat - without significant price spread decline Developing Market Access • Strong share in markets with freight advantage • Grown or maintained share of stable and high growth markets Improving Productivity • Reduced / contained supply chain costs

Grain Company to Australia’s Largest Agribusiness 100,000 customers Grain company $5-$6b revenue Merch $1.2b sales Fertiliser 1.2m tonnes Livestock 2.0m cattle 11m sheep Wool 600k bales Real Estate $800m sales Finance $2.0b loan book $300m on deposit Insurance $120m premium 2,500 employees 430 outlets

Grain Marketing and Handling Chartering Risk Manage- ment Financial Services Insurance Merchan- dise Agronomy Wool Livestock Real Estate The Integrated Business Model Australia’s leading Agribusiness Our vision delivered by.. Comprehensive product / service offering managed through an... Integrated Value Chain to ensure that AWB is the… Acquisition and Trading Milling and Processing Offshore Supply Chain Domestic Supply Chain End use demand Seeds and R&D Farm inputs Freight Business Partner of choice Primary producer Business partner of choice End use customer

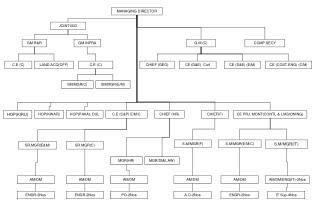

Group structure AWB Limited Commercial operations Pooling operations Pool Management Services Finance & Risk Management Grain Acquisition & Trading Supply Chain & Other Investments Grain Technology Landmark

AWB is focused on delivering value… • Financial Performance • Commercial skills and culture • Diversified agribusiness • Positive outlook for Australian agriculture