Download

1 / 24

250 likes | 451 Views

Bank Restructuring developments IN EUROPE. 25 th September 2013. Tom McAleese. AGENDA. Banking Trends in Europe Case Study 1 – The Spanish Asset Management Co. ( SAREB ) Case Study 2 – The banking crisis in Cyprus The Single Supervisory Mechanism (SSM)

E N D

Bank Restructuring developments IN EUROPE 25th September 2013 Tom McAleese

AGENDA • Banking Trends in Europe • Case Study 1 – The Spanish Asset Management Co. (SAREB) • Case Study 2 – The banking crisis in Cyprus • The Single Supervisory Mechanism (SSM) • The Irish ‘model’ in Europe

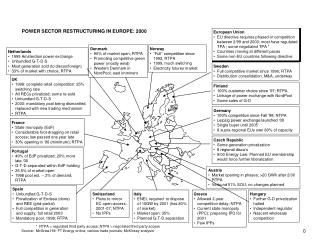

Europe can be split into four main market segments Sovereign Exposure to Banking Industry Index Luxembourg* Malta Ireland Countries with financial hubs Cyprus Banking Assets to GDP Ratio Large mature markets UK Medium mature markets Denmark France EU Average 3.95 Portugal Austria Holland Belgium Spain Finland Germany Greece Sweden Italy Lithuania Bulgaria Romania Slovakia Estonia Czech Republic Latvia Poland East European transition economies Hungary EU Average € 361 bn Slovenia GDP (in €bn) • * Luxembourg is an outlier with co-ordinates (43, 25) • Source: European Banking Federation Statistics

Systemic banks that are greater than 100% gain attention Individual Bank Assets as % of GDP • The asset base of the two largest banks in Cyprus was more than 4x GDP, in Ireland the corresponding number was 2.4x. • In countries such as UK, France and Italy this number varied between 2.3x to 1x. In Greece, it is the lowest amongst the countries studied. • Source: 2011 data, Liikanen Report

Banks in europe have been rebuilding their capital since 2008 • Capital ratios at European banks have risen from 9.0% to 11.8% since 2008. • Banks have developed new, loss-absorbing, forms of debt – such as contingent convertibles (known as CoCos) and wipeout bonds. • The European average of banking assets to GDP is 3.95x, while the US stands at 0.9x GDP. • Confidence is still an issue in Europe - US banks trade on 1.2x their book values, while European banks trade on 0.8x book. Source: SNL Financials - 2013 figure is to August 2013

What should banks be doing? • Banks should take the following five steps: • Stay close to European regulators, to understand their plans and enhance influence; • Understand the balance sheet’s strengths and weaknesses in rigorous detail; • Make risk management as robust as possible; • Solve legacy problems by separating non-core businesses either legally or through management; • Uphold the highest standards of moral conduct in reportable ways.

SAREB – AN OVERVIEW Source: FROB website and investor presentation April 2013

SAREB – transferred assets • The Bank of Spain defined three groups of banks: • Group 0: banks with no capital shortfall (Santander, BBVA, Sabbadell, etc.) • Group 1: banks already controlled by FROB (Bankia, Catalunya Caixa, NovaGalicia, Banco Gallego, Banco de Valencia) • Group 2: banks requiring public support (CEISS, BMN, Caja 3, Liberbank) • Group 3: banks to implement private measures • Group 1 banks’ assets were transferred first into SAREB on 27th December 2012, followed by Group 2 banks’ assets on 28th February 2013

sareb VS. NAMA – a comparison – cont’d Source: NAMA and SAREB websites

Why did cyprus get into trouble? • External causes • Consequences of joining the EU (2004) & Euro (2008) • Global financial crisis • Internal causes • Insufficient supervision of banks at a national level (“spoiling the party”) • Aggressive growth strategies (aggressive lending and overseas expansion / acquisitions) • Weak bank governance (“culture of deference”) • Imprudent business methods (lending against collateral or PGs / strong personal relationships) • Role of international financial centre (source of excess liquidity) • Cosy culture Source: Independent Commission on the Future of the Cyprus Banking Sector – Interim Report June 2013

debt and equity markets were immature resulting in a higher reliance on banks Market Capitalization of Top 12 Firms Listed on the CSE • The Cypriot Stock Exchange (CSE) has 111 listed companies with a total market capitalization of € 2.22 bn as of 7th February 2013. The median market capitalization was €3.9 m and the average market capitalization was significantly higher at €23.9 m. • The top 3 banks constituted 64% of the total market capitalization of the CSE. Laiki Bank • Source: Bloomberg, Cyprus stock exchange website

Timeline of key events • Eurogroup decision to reduce Programme envelope to €10bn, with no funds for recap of BoC or Laiki. Decision to implement a deposits levy, requiring banks to be closed for implementation • 16 March • ECB decided no further provision of ELA to Laiki unless an MoU is signed • 21 March • Final BoC depositor haircut set at 47.5% and BoC officially out of resolution • 30 July • Parliament urgently passes resolution law • 22 March • Cyprus request financial assistance from the IMF, after Greek crisis • June 2012 • 19 March • Parliament rejects bank levy • 18-28 March • Closure of banks and imposition of capital controls December 2012 Preliminary MoU agreed with €10bn to recapitalise the banking sector (total €17bn) January 2013 PIMCO results announce extra capital of €11bn • 25 March • Resolution – Eurogroup decision to resolve the two biggest banks, sale of Greek assets and bail-in. • 14 May • Agreement of the Programme – first tranche of €2bn on 14/5

Resolution steps 1 • Bank of Cyprus and Laiki put under resolution on 25/3/2013 on the basis of the new Resolution Law. • Country-wide capital controls introduced after Eurogroup meeting on 16 March 2013. Introduction of Capital Controls 2 BoC and Laiki under resolution 3 • Greek operations of BoC, Laiki and Hellenic sold to Piraeus Bank. The transaction included loans, fixed assets and deposits of the Greek branches (i.e. assets of €16.4bn and liabilities of €15bn). Greek Carve Out Transaction 4 • Issuance of the relevant decrees (29/3/2013):a) Laiki transferred its Cypriot operations and certain other assets and liabilities to BoCb) depositors and other creditors of BoC are bailed-in in order to recapitalise the bank Carve-out Laiki CY Bail-in BoC creditors 5 • The final step is the merger of Laiki Cyprus operations with Bank of Cyprus • Legacy Laiki will be wound down; main assets of the legacy entity are the investments in subsidiaries and the shares in BoC post the sale of its Cypriot operations to BoC Merger Laiki CY with BoC and wind down Legacy Laiki

Deposit Freeze and Release example – BoC customer with a €200,000 deposit 15 March 2013 2 April 2013 30 July 2013 €100,000 €110,000 €152,500 €100,000 €100,000 €100,000 €100,000 insured deposit €100,000 insured Accessible subject to capital controls Total deposit of €200,000 €10,000 €10,000 €100,000 uninsured Released 10% of €100,000 €5,000 €37,500 €40,000 blocked Released and placed into term deposits of 6/9/12 months (€12,500 each) €42,500 released €30,000 blocked €100,000 blocked deposit €22,500 blocked as reserve for share exchange €22,500 blocked as reserve for share exchange €47,500 exchanged for BoC shares €37,500 blocked for exchange into BoC shares €37,500 blocked for exchange into BoC shares

TROIKA want domestic banks to deleverage to 3.5x GDP (BELOW the EU Average) • Deleveraging of the domestic banking system • Domestic banking system with high banking assets to GDP ratio of 4.93x in 2012 • Troika set deleveraging target of 3.5x banking assets to GDP by 2018 • Significant deleveraging achieved to-date through sale of Greek operations in the amount of c. €20bn, resulting in a current banking assets to GDP ratio of 3.66x • Based on 2018 GDP forecast Troika target of €18.3bn, the total size of the domestic banking market could even increase from today’s size to €64bn

Mou tasks - A lot to be done within a short time frame Source: Memorandum of Understanding - Cyprus, April 2013

CURRENT BANK DEVELOPMENTS • Bank of Cyprus • Recapitalised at a CET 1 ratio of 12% after bail-in of uninsured BoC depositors of 47.5% • First AGM conducted as a new group held on 10th September 2013 and new BoD elected • Developing a restructuring plan to be approved by the European Commission • Hellenic Bank • Planned recapitalisedthrough a €300m debt-to-equity conversion • Cooperative Banking Sector • Developing a restructuring plan for the entire cooperative banking sector • Strategy includes multiple mergers to decrease number of individual cooperative banking institutions from 93 to 18 • Planned recapitalisation with €1.5bn of programme money upon approval of the restructuring plan by the European Commission • Cyprus Banking Sector Deleveraging • Significant deleveraging of Cyprus domestic banking market from c. €90bn in 2012 to currently c. €60bn, mainly due to sale of Greek banking operations

Cyprus – lessons learnt • 2 systemic banks under resolution at the same time • Disruption of the whole banking system • Significant hit on the real economy • Financial and social instability • Cross border resolution – how do you deal with international operations and regulators • Thousands of court actions against BOC and CBC • Operational issues: Identifying insured depositors, client a/cs, trustee a/cs, minor a/cs, set – off of deposits to loans, etc. • The term ‘resolution’ is incorrectly considered by different stakeholders as an event of default • Resolution cost more than re-capitalisation (with strict restructuring measures implemented over time). • Most severe bail-out yet – GGBs haircut, immediate deleverage, capital controls, bank merger and bail-in of depositors.

THE SSM is Coming… The Single Supervisory Mechanism (SSM) under the authority of the ECB shall have direct responsibility for the supervision and the financial stability of the biggest and systemic banks in the Eurozone. Scope and Structure • Commonbank supervision in the EU composed of the ECB and national authorities. • The ECB is endowed with final supervisory authority while national supervisors playing a supporting role. • Participation is mandatoryfor 17 Eurozone countries and optional for the other EU member states. • Banks deemed “significant” will be supervised directly by the ECB and will comprise more than 80% (more than €25 trillion) of the Eurozone’s banking assets. • The Supervisory Board will consist of 23 representatives including: 17 national supervisors, a chairperson, vice-chairperson and 4 ECB representatives. • SSM represents an entirely new architecture, unprecedented in its scope and scale. The successful implementation of the SSM therefore poses significant challenges for the ECB. Balance-Sheet Assessment (BSA) Exercise (“Entry test” condition) • The draft SSM Regulation requires the ECB to conduct a “comprehensive assessment”, including a balance-sheet assessment (BSA), of the qualifying credit institutions of the participating Member States” as pre-condition for entry. • The BSA exercise is envisaged to include a targeted risk-based balance sheet review, which will include an asset quality review (AQR), data integrity validation (DIV), risk weighted asset (RWA) assessment and capital adequacy assessment.

THE ‘IRISH MODEL’ in europe Certain Irish bank restructuring measures are now being applied in Europe