Download

1 / 11

110 likes | 338 Views

Could Turkey’s financial crisis and the collapse of its currency have been prevented?. Turkey’s Kriz (A). Turkey’s Kriz (A).

E N D

Could Turkey’s financial crisis and the collapse of its currency have been prevented? Turkey’s Kriz (A)

Turkey’s Kriz (A) • It was only when optimistic Turks started snapping up imports that investors began to doubt that foreign capital inflows would be sufficient to fund both spendthrift consumers and the perennially penurious government. “On the Brink Again,” The Economist, February 24, 2001.

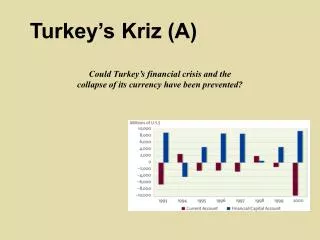

Turkey’s Kriz (A) • In February 2001 Turkey’s rapidly escalating economic kriz, or crisis, forced the devaluation of the Turkish lira. • The Turkish government had successfully waged war on the inflationary forces embedded in the country’s economy in 1999 and early 2000. But just as the economy began to boom in the second half of 2000, pressures on the country’s balance of payments and currency rose. • The question asked by many analysts in the months following the crisis was whether the crisis had been predictable, and what early signs of deterioration should have been noted by the outside world. • First, Turkey seemingly suffered significant volatility in the balances on key international accounts. • The financial account swung between surplus (1993) to deficit (1994), and back to surplus again (1995-1997). After plummeting in 1998, the financial surplus returned in 1999 and 2000. • Secondly, as is typically the case, the current account behaved in a relatively inverse manner to the financial account, running deficits in most of the years shown. • But the deficit on current account grew dramatically in 2000, to over $9.8 billion, from a deficit in 1999 of only $1.4 billion.

Exhibit 1 Turkey’s Balance of Payments, 1993–2000 Turkey’s current account had been relatively volatile (generally in deficit), but had taken a severe dive in 2000. The capital/financial account balance was in surplus nearly throughout the period reflecting the massive international borrowing by Turkey.

Turkey’s Kriz (A): Case Questions • Where in the current account would the imported telecommunications equipment be listed? Would this correspond to the increase in magnitude and timing of the financial account? • Why do you think that net direct investment declined from $571 million in 1998 to $112 million in 2000? • Why do you think that TelSim defaulted on its payments for equipment imports from Nokia and Motorola?

Exhibit 4 Turkish Inflation Rate and Exchange Rate (quarterly) Inflation Rate Exchange Rate

Turkey’s Kriz (A): Case Questions • Where in the current account would the imported telecommunications equipment be listed? Would this correspond to the increase in magnitude and timing of the financial account? • The telecom equipment would appear in the Current Account as an import of goods. Net other investment would include financing by the vendors that sold TelSim the equipment. • This and other imports of capital equipment probably accounted for most of the increase in net other investment and thus the large negative balance in the Financial Account in the year 2000. • Why do you think that net direct investment declined from $571 million in 1998 to $112 million in 2000? • The decline was probably caused by a lack of confidence in Turkey’s political stability and long-term growth prospects. • Turkey’s war on its own’ inflation during the period 1999 to early 2000 must have included high interest rates and other macroeconomic policies to slow down the rate of growth. • A slower rate of growth, if maintained in the long run, would reduce expected returns and direct investment inflows.

Turkey’s Kriz (A): Case Questions • Why do you think that TelSim defaulted on its payments for equipment imports from Nokia and Motorola? • TelSim needed to invest heavily in capital equipment in order to create a modern high speed, high capacity network. Unfortunately, a considerable time gap typically exists between the time a network is created and it s capacity is utilized by revenue-paying customers. • Thus long-term financing rather than short-term trade financing is needed. The timing gap experienced by TelSim was also experienced by many other telecommunications companies worldwide, including the highly-publicized case of Global Crossing, which also went bankrupt. • Expectations for the telecom industry and its ability to “monetize its customer base,” the ability to generate significant revenues from installed networks, proved overly optimistic. • A worldwide overcapacity of telecommunications networks led to cutthroat price competition, adding to the shortfall in revenues experience worldwide. The overcapacity continued for several years, however, as firms attempted to survive by covering variable costs but not fixed capital costs of providing services.

Turkey’s Kriz (A): Case Questions • Why do you think that TelSim defaulted on its payments for equipment imports from Nokia and Motorola? (continued) • Finally, there has been a continuing debate over the intentions and ethics of the Uzan family itself – the controlling interest group of TelSim. • The press has run a number of stories raising the question as to whether the Uzan family had ever truly intended to repay the massive infrastructure financing provided by Motorola and Nokia. At the time of this writing, however, there is no proof that this was the case.

Exhibit 2 Subaccounts of the Turkish Current Account, 1998–2000 (millions of U.S. dollars)

Exhibit 3 Subaccounts of theTurkish Financial Account, 1998–2000 (millions of U.S. dollars)