Download

1 / 22

220 likes | 2.1k Views

Financial System Overview and the Flow of Funds Week 1 – August 24, 2005 The Financial System What happened on August 9, 2005? What was market reaction? What are the linkages between those actions and business conditions? What is occurring in financial markets?

E N D

Financial System Overview and the Flow of Funds Week 1 – August 24, 2005

The Financial System • What happened on August 9, 2005? • What was market reaction? • What are the linkages between those actions and business conditions? • What is occurring in financial markets? • Interest rates, mortgage borrowing, restructuring of financial firms? • New financial products? • What framework can be used to comprehend these important changes?

This course • Overview of institutions and markets • Major institutions and their regulators • Interest rate determination • Risk. risk management, and risk premiums • Important financial markets in depth • Closer scrutiny of the money market and important factors influencing conditions • Detailed review of important credit markets and the market for equity

Readings in text first two weeks • This evening will we cover Chapters 1 to 3 • Chapter 1 - Functions of financial system • Chapter 2 - Markets and funds flows • Chapter 3 - Efficient markets and information • Try to review these and raise any questions by next time, they are introductory • Next week, cover Chapters 14 and 15 • Chapter 14 – Banks • Chapter 15 – Non-bank thrift institutions

Stages of financial systems • Each unit is independent, investments accumulate over time, e.g. a farm • Units can accumulate value in monetary asset (e.g. claim on government) in order to save for large investments • Units can borrow and lend individually • Financial intermediaries raise funds from saving units and lend to investing units

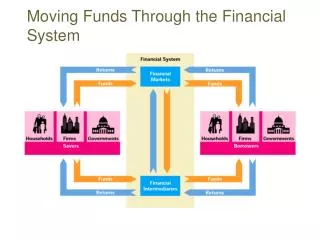

Circular Flows • Goods and services • National product accounts, gross domestic product • Produced by Commerce Department • Income flows • National income accounts • These accounts do not reflect financial market activity • Flow of Funds Accounts of Federal Reserve system track financial flows

Financial Markets • Money and capital markets • Open versus negotiated markets • Competitive market-based funding versus intermediated or bank-dominated funding markets • Primary versus secondary markets • Spot versus futures, forward, and option markets

Sources and uses = flows • Sources and uses are changes in balance sheets • We want to look at both • Balance sheets represents stocks, hence total size, at a point in time • Flows represent net changes in stocks (I.e. new issues minus repayments of financial assets or liabilities)

Balance sheets and portfolios • Assets = Liabilities + (net worth = equity, common stock shares, etc.) • Assets • Financial assets • Money, loans and bonds, equity investments • Real assets • Housing, consumer durables including autos • Inventory, plant and equipment

Balance sheets/portfolios (cont’d) • Liabilities • Monetary liabilities (loans, mortgages) • Other financial liabilities • Net worth is composed of equity in real assets and net financial claims on others • Sectors are aggregate balance sheets of similar units • Households, business, government • Financial institutions

Sectoral balance sheets • Balance sheets of Households and Non-profit organizations • 2004 largest real and financial assets • 2004 largest liabilities • 2004 composition of real asset holdings • share of monetary assets • Compare 1980 balance sheets • Share changes = growth and change in portfolio composition

Sectoral balance sheets (cont’d) • Farm + non-farm non-financial non-corporate + non-farm non-financial corporate business • Non-farm non-financial corporate balance sheet • 2004 largest assets • 2004 largest liabilities • 2004 composition of real asset holdings • share of monetary assets • Compare 1980 balance sheets

Wealth and flow of funds • Primary sectors = households, business government • Financial sector • Financial claims - financial liabilities (small holdings of real assets) • Aggregate wealth is real assets since all financial claims cancel

Wealth • Total wealth in 2004 is approximately (billions) $22,566.2 + $10,479.1 + 6,407.9 = $ 39.5 trillion • 2004 GDP is $11,734.9 trillion, so income-capital ratio is approximately .30 or capital-income ratio 3.4 • 1980 wealth approximately $ 9,729.7 trillion, GDP $ 2,789.5 trillion, so capital-income ratio is also about 3.5 (about the same) • GDP over assets in 1980 and 2004 around 30% • Has tangible wealth composition changed?

Distribution of GDP • Employee compensation in 2004 was $6,651, or 56.7% of GDP • Business tangible assets were $ 16,887.0 or 40.7% of “total” tangible assets • Roughly gross before tax return on business investment is: • Gross return illustrates top downapproach

Composition of wealth • Compare composition of tangible assets1980 2004Households Real Estate 78% 83% Durables 21% 16%Business (corporate + non-corporate) Real Estate 67% 68% P&E 22% 23% Inventories 11% 9% • Think of other economies

The Financial System • Channels savings into investment • Financial institutions assist in this process • Financial institutions create value for primary surplus and deficit units through • Increasing economic efficiency • Providing financial servies • The value of flow of funds framework is that we can trace the changing roles of financial institutions

Next time • Before next Wednesday, review Chapters 1 to 3 of Money and Capital Markets and identify any questions about this evening’s session • Read Chapters 14 and 15 of Money and Capital Markets • Bring a Wall Street Journal to class every Tuesday