Download

1 / 27

270 likes | 391 Views

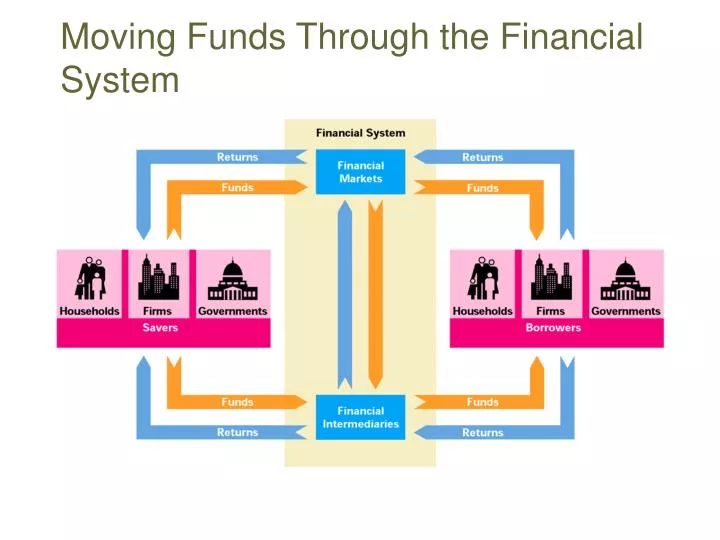

Moving Funds Through the Financial System. Purpose of the Financial System. Transfer funds from savers to borrowers. Savers are suppliers of funds, Borrowers are demanders of funds. Financial markets issue claims on borrowers. Financial intermediaries act as go-betweens.

E N D

Purpose of the Financial System • Transfer funds from savers to borrowers. • Savers are suppliers of funds, Borrowers are demanders of funds. • Financial markets issue claims on borrowers. • Financial intermediaries act as go-betweens.

Key Services Provided by the Financial System • Risk sharing by allowing savers to hold many assets (through diversification) • Providing liquidity, which is the ease with which an asset can be exchanged for money • Providing information about borrowers and returns on financial assets • Delegating monitoring activity • Pooling Funds for Investment

Describing the Financial System • Direct Financing and Indirect Financing • Direct Financing: lenders lend directly to borrowers in a market • Indirect financing: lenders lend to financial intermediaries who then lend to borrowers. (Financial Intermediaries: two broad types: bank and non-bank intermediaries (mutual funds, hedge funds etc.)

Financial Markets • Primary markets are those in which newly issued claims are sold to initial buyers. • Secondary markets are those in which previously issued claims are resold.

Direct Finance • Primary markets: newly issued claims are sold to buyers from the borrower. This could be: a. Debt (Requires borrower to pay principal (amount of loan)+ interest. Types? b. Equity (Allows for variable payments to be made, and lender gets to own share of profits and assets of firm) Which do you think accounts for larger amount of funds raised?

Beginning December 11, 2001 the Series EE savings bonds you buy will be inscribed with the special legend "Patriot Bond." These specially designated Series EE Patriot Bonds offer Americans one more way to express their support for our Nation's anti-terrorism efforts. Please follow the links below for more information about the Patriot Bond. Example of Government issued debt

Maturity • Short-term debt maturity of less than a year • Intermediate-term debt instruments of maturity of less than a year • Long term debt >10 years

Primary Market • Advantages and Disadvantages of: Debt • Issuers of debt continue to own their assets and can pay fixed payments • For lenders, there is the risk of default Equity • Issuers of Equity do not have a fixed scheduled payment (expect to give dividends) • For lenders there is the risk of no returns

Describing Secondary Markets • The Capital Market: where equity and debt whose maturity (length to payment) is greater than one year is traded • The Money Market where debt whose maturity (length to payment) is less than one year is traded

Secondary Market • Market where debt and equity from the primary market are bought and sold • Why have it? Provides for diversification of portfolio, promotes liquidity, and gives information • Auction and Over the Counter markets. Auction (prices are set by competitive bidding-e.g. stock exchange). OTC (prices are posted and can be bought at that price).

Types of Secondary Financial Markets • Maturity: money and capital markets • Trading places: auction and over-the-counter markets • Settlement: cash or derivative

Important Financial Instruments • Money market instruments- Treasury Bills, Commercial Paper, Banker’s acceptances, Repurchase agreements, Federal Funds, Eurodollars, CD • Capital Market Instruments- Treasury securities, Government agency securities, Municipal Bonds, Stocks, Corporate Bonds, Mortgages, Commercial Bank Loans

Flow of Funds is a good source of data • The US produces a flow of funds table which provides some useful information about where funds and liquidity are flowing. • This is available on class website .

Goals of Financial Regulation • Provision of information • Maintenance of financial stability • Controlling the money supply • Encouraging particular activities

Changes in Financial Integration and globalization • Financial Integration is on the rise • Much innovation • Higher globalization

Financial structure: bank-based vs. stock market-based • Three questions about the relationships between financial intermediation and real economic activity: • (1) Does FS affect economic activity? Evidence: Yes • (2) Direction of causality: FS leads econ activity or vice versa? Evidence: both • (3) Does the structure of the FS matter?

Role of banks in promoting investment • Pooling savings (under the view that savings cause investment) • Reducing liquidity risk (maturity transformation) • Information about investment opportunities (economies of scale in information gathering/processing) • Delegated monitoring • Customized financial products financial and technological innovation • Criticism of bank-based systems: • Rent extraction (from information) • Close bank-firm ties preclude competition

Role of stock markets (for investment) • Information about profitability of investment • Reduce the cost of capital: importance of SM liquidity, not just size • Pressure on management: takeovers (effective or threat) • Criticism of SM-based systems • Economic content of SM signals (do prices reflect fundamentals – see later, chap 10) • Takeovers: do not necessarily increase efficiency; hostile takeovers (costly); promoting short-termism in management

Banks vs. SM: where does research stand? • Complementarity of banks and SM • More productive research avenues: • Financial services view (both banks and SM) • Law and finance view: creditor and investor rights; quality of the legal system