Download

1 / 0

0 likes | 153 Views

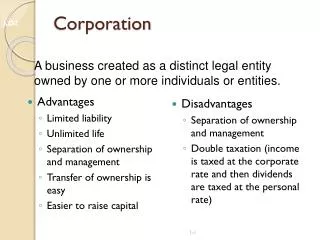

Advantages Limited liability Unlimited life Separation of ownership and management Transfer of ownership is easy Easier to raise capital. Disadvantages Separation of ownership and management

E N D