Download

1 / 5

50 likes | 214 Views

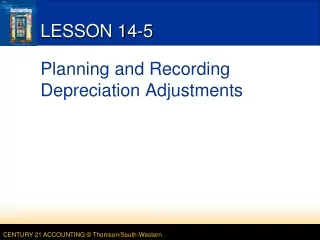

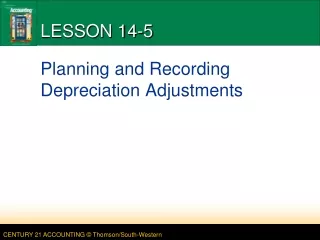

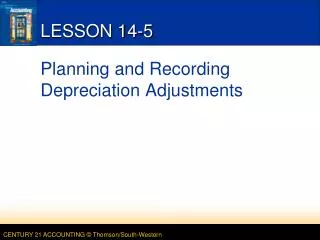

LESSON 14-5. Planning and Recording Depreciation Adjustments. Original Cost. Estimated Total Depreciation Expense. –. ÷. Estimated Salvage Value. Years of Estimated Useful Life. =. =. Annual Depreciation Expense. Estimated Total Depreciation Expense.

E N D

LESSON 14-5 Planning and Recording Depreciation Adjustments

OriginalCost Estimated TotalDepreciationExpense – ÷ EstimatedSalvage Value Years ofEstimatedUseful Life = = AnnualDepreciationExpense Estimated TotalDepreciationExpense CALCULATING DEPRECIATION EXPENSE AND BOOK VALUE page 424 (continued on next slide) 1. Subtract the asset’s estimated salvage value from original cost. 2. Divide the estimated total depreciation expense by the years of estimated useful life. 1 $1,250.00 – $250.00 = $1,000.00 2 $1,000.00 ÷ 5 = $200.00 LESSON 14-5

20X2AccumulatedDepreciation Original Cost + – 20X3DepreciationExpense AccumulatedDepreciation = = 20X3AccumulatedDepreciation EndingBook Value CALCULATING DEPRECIATION EXPENSE AND BOOK VALUE page 424 (continued from previous slide) $400.00 + $200.00 = $600.00 $1,250.00 – $600.00 = $650.00 LESSON 14-5

3 3 ANALYZING AND RECORDING ADJUSTMENTS FOR DEPRECIATION EXPENSE page 425 2 1 1. Write the debit amounts. 2. Write the credit amounts. 3. Label the adjustments. LESSON 14-5

TERMS REVIEW page 426 • current assets • plant assets • depreciation expense • estimated salvage value • straight-line method of depreciation • accumulated depreciation • book value of a plant asset LESSON 14-5