Download

1 / 21

230 likes | 761 Views

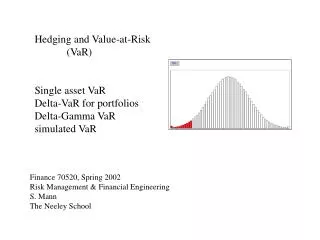

VAR and VEC. Using Stata. VAR: Vector Autoregression. Assumptions: y t : Stationary K-variable vector v : K constant parameters vector A j : K by K parameters matrix, j=1,…,p u t : i.i.d.( 0 , S ) Exogenous variables X may be added. VAR and VEC.

E N D

VAR and VEC Using Stata

VAR: Vector Autoregression • Assumptions: • yt: Stationary K-variable vector • v: K constant parameters vector • Aj: K by K parameters matrix, j=1,…,p • ut: i.i.d.(0,S) • Exogenous variables X may be added

VAR and VEC • If yt is not stationary, VAR or VEC can only be applied for cointegrated yt system: • VAR (Vector Autoregression) • VEC (Vector Error Correction)

VEC: Vector Error Correction • If there is no trend in yt, let P = ab’ (P is K by K, a is K by r, b is K by r, r is the rank of P, 0<r<K):

VEC: Vector Error Correction • No-constant or No-drift Model: g = 0, m = 0 (or v = 0) • Restricted-constant Model: g = 0, m≠ 0 (or v = am) • Constant or Drift Model: g≠ 0, m≠ 0

VEC: Vector Error Correction • If there is trend in yt

VEC: Vector Error Correction • No-drift No-trend Model: g = 0, m = 0, t = 0, r = 0 (or v = 0, d = 0) • Restricted-constant Model: g = 0, m≠ 0, t = 0, r = 0 (or v = am, d = 0) • Constant or Drift Model: g≠ 0, m≠ 0, t = 0, r = 0 (or d = 0) • Restricted-trend Model:g≠ 0, m≠ 0, t = 0, r≠ 0 (or d = ar) • Trend Model:g≠ 0, m≠ 0, t≠ 0, r≠ 0

Example • C: Personal Consumption Expenditure • Y: Disposable Personal Income • C ~ I(1), Y ~ I(1) • Consumption-Income Relationship:Ct = a + bYt-1 + gCt-1 +…(+ dt) + e • Cointegrated C and I: e ~ I(0) • Johansen Test with constant model and 10 lags

Example • VAR: • VEC: • Rank 1 P = ab’

Example • Empirical Model: 1949q4 – 2006q4 • Constant, 10 lags • Restricted-constant, 10 lags

Restricted VAR • Parameters Restrictions • Many of the parameters associated with augmented lags are 0 • Structural VAR • Linking with macroeconomic theory

Impulse Response Function • Based on VMA representation, we can trace out the time path of the various shocks on the variables in the VAR system.

VAR and Simultaneous Equations • Identification: • A = -B-1G, ut = B-1et • A = [A1,…,Ap,v], G = [G1,…, Gp,g0] • B and G1,…,Gp are K by K parameters matrices • Var(ut) = S = B-1Var(et)B-1’

Structural VAR • VAR as a reduced form of simultaneous equations model requires parameters restrictions so that the system model is identified or estimatable. • A structural VAR corresponds to an identified simultaneous equations system. • The restrictions are necessarily placed on the parameters matrix B and therefore the variance-covariance matrix S of VAR.

Example • 2-Equation System Model: • Structural VAR:

Example • Structural VAR: • Identification and Parameters Restrictions

Stata Programs • us_dpi_pce.txt • dpi_pce4.do • dpi_pce5.do • dpi_pce6.do • dpi_pce7.do