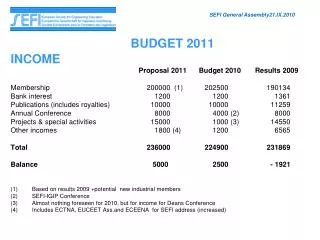

Download

1 / 71

710 likes | 828 Views

Budget Office. The Budget Process. Todd Lee Assistant Chancellor Budget & Planning April 2011. Budget Office. Key Concept to Take Away. University budgeting is not a single process.

E N D

Budget Office The Budget Process Todd Lee Assistant Chancellor Budget & Planning April 2011

Budget Office Key Concept to Take Away • University budgeting is not a single process. • It consists of a number of processes that have evolved separately and which occur with varying degrees of coordination.

Budget Office Discussion Topics • Permanent budget vs. General Ledger • Campus “budget” • UC funding from the State • UCOP allocations to the campus • Campus allocations • Current situation

PermanentOperating Budget • Reflects “funding” assumed to be available on an ongoing basis • As of July 1, 2010 = $469 million • 63% from General Funds • 71% of general fund budget related to salaries and benefits • 59% of total budget associated with salaries and benefits • 95% of instruction budget from general funds

General Ledger • Includes permanent budget plus: • Carry-Forward from previous years • Allocations made after July 1 • Contract and Grant awards • Current year gifts • Distributions from endowments • At year-end UCEN & AS added

Perm Budget vs. G.L. • Permanent Budget • Result of incremental budget approach • Represents base level of recurring resources to cover costs of salaries and supplies • General Ledger (Temporary Budget) • Permanent Budget, one-time allocations, and carry-forward from previous year

Perm Budget vs. General Ledger Difference reflects use of carry-forward, one-time funds, and growth in student fees and non-budgeted funds such as contracts & grants. Increased expenditures mostly related to research, financial aid and auxiliary services.

FY 2008-09 Operating Expenses Expenditure information reported in approximately 95,000 Account-Fund-Sub-Object Codes Includes all fund sources Top 3 Categories account for 77% of total expenses Savings produced in categories have different impacts on campus budget due to source of funding

Budget Office State Funding Process • UC Internal Budget Consultation • Regents Budget • Governor’s Budget Proposal • Budget Reviews • Governor’s May Revision • Budget Bill • Allocations from UCOP

Budget Office Budget by Fund Category

Budget Office Campus Allocation Decisions • Based on: • Funding formulas • Campus consultation • Campus priorities • Fund source restrictions • Control point decisions

Budget Office FUND SOURCE CATEGORY #1 • Core Funds • State General Funds • UC General Funds • Mandatory Student Fees • Indirect Cost Recovery (Overhead) • Other State

FUND SOURCE CATEGORY #2 • Non-Core Budgeted Funds • Sales and Services Revenue • Auxiliary Revenue • Student Fees (Campus Approved)

FUND SOURCE CATEGORY #3 • Extramural Funds • State & Local Contracts & Grants • Federal Contracts & Grants • Private Gifts and Endowments

Budget Office State General - Fixed Costs • Provided to campus as a “block allocation” • Used to fund salary increases, changes in benefit costs, and price increases on non-salary budgets • Salary funding provided directly to departments based on approved increases

Budget Office State General - Fixed Costs • Price increase funding distributed to four areas: • Library • Purchased Utilities • Graduate Block Grant (Financial Aid) • Control Points • Control point distribution based on formula that takes into account support expenditures

Budget Office State General - Workload • Primary allocation is for enrollment growth (Also receive funding for new space and financial aid.) • Enrollment growth first used to fund faculty and T.A. needs: • 1 faculty FTE per 18.7 student FTE • 1 T.A. per 44.0 undergraduate FTE • These allocations take up approximately 55-65% of the allocation

Budget Office State General - Workload • Remaining 35-45% distributed as support • Designated campus priorities such as • Instructional support • Library support • Graduate student support • Faculty recruitment • Academic advising

Budget Office State General - Workload • Designated campus priorities • Public safety • Systems development • Research support • Space initiatives • Undesignated control point allocations • Formula distribution • Based on number of faculty, staff, & students per control point

Budget Office State General - ProgramGrowth & Initiatives • Typically distributed to designated areas for specific purposes. For example: • Library allocation goes to library • Instructional equipment allocations goes to EVC for distribution to colleges and then to academic departments • Ongoing building maintenance allocation goes to facilities maintenance for general maintenance projects

Student Fees - Four Types • Mandatory Systemwide Fees • Extension & Summer Quarter • Course Material Fees • Lock-In Fees • Each fee type has a different review and approval process

Budget Office Student Fees • Systemwide Fees - Registration and Educational Fees • Fee levels established by Regents • Revenues change based on fee levels and number of students • Campus retains all student services (registration) fees • Beginning in FY 2011-12 Tuition (Ed Fee) Revenue remains at campus, after financial aid adjustment.

Mandatory Student Fees • Fee levels established by Regents

Budget Office Other Fee Programs • Extension (self-supporting program) establishes their own fee structure to cover program • Summer Session charges a per unit fee based on academic year systemwide fees • $247.32 per unit plus $360.02 campus based fee

Budget Office Student Fees • Course Material Fees • For “materials and services for special supplemental educational experiences” • Reviewed by: • Appropriate Provost/Dean • College Executive Committee • Income and Recharge Committee • Student Fee Advisory Committee • Executive Vice Chancellor & Chancellor

Budget Office Student Fees • Student Lock-In Fees • Approved by students in general election • Examples includes: • Facility Debt - (Ucen, ReCen) • Departmental Operating Expenses - UCC, Disabled Students, Multicultural Center • Programs - Bicycle System, ICA Scholarships, MTD Bus Passes • Current UG = $1,384; Grad = $721.74

Budget Office Indirect Cost Recovery • Overhead on federal and private contact and grants • Amount depends on indirect cost rate and grant activity • Complicated distribution formula with portion shared with State • Portion becomes part of General Fund with remainder becoming unique fund sources

Budget Office Indirect Cost Recovery • Portion of campus allocation already permanently budgeted • Portion goes to research control points by formula taking into account actual research activity • Remainder typically used to support campus development program (new space)

Budget Office Gifts and Endowments • Permanent budget includes annual payout on Regents’ endowments • Increases occur during the year due to current year gifts and transfers from the Foundation • Any given year $40 to $80 million in gifts distributed for current use, capital projects, and endowments

Gifts & Endowments • December 2009 endowment value of approximately $174 million (Foundation $99.3 million, Regents $74.7 million) • Annual payout of of approximately 4.75% ($8.3 million) • Most gifts (both endowment and current have use restrictions; only about $1.8 million on annual gifts are unrestricted

Budget Office Income • User charges for campus provided services • Fees established by departments with campus review • Examples include: • Student housing • Parking • Residential Communication Services

Budget Office Other State • Funding for special state programs • Primarily financial aid and lottery funds • Lottery funds designated for instructional programs such as: • Instructional Use of Computers • Instructional Equipment Replacement • Arts and Humanities

Budget Cuts - Context • Approximately $116 million net reduction in state funding for our campus over the last decade. • Student tuition, for the first time, surpasses the state contribution to education • Level of state funding equal to FY 1098-99 when the university was serving 73,000 fewer students.

Current Campus Situation • Looking at $39.6 million in cuts • Another $26.7 in unfunded expenses • Recent memo from Chancellor Yang outlined the current campus budget situation.

The Process • Coordinating Committee on Budget Strategy • Planning Principles • Budget Review Topics • Budget Cut Targets

Campus Planning • CCBS - Coordinating Committee on Budget Strategy • Originally created in January 2003 to help guide the cuts earlier this decade. • Reactivated in March 2008 • Includes Administrators, Academic Senate, Faculty, Staff, and Students • Develop strategies designed to protect academic quality and student access while facing the challenge of budget reductions.

Budget Office Coordinating Committee on Budget Strategy • Develop principles and priorities to guide budget reduction process • Protect academic quality and student access • Achieve short term budget reductions • Establish framework for long term stability • Interact with groups and committees to develop and share information, and provide opportunity for feedback

Planning Principles • Strategic Solutions • Budget reductions should be implemented strategically, not across the board, in a manner that will maintain focus on the campus academic mission. • Priorities • The campus should attempt to minimize the impact of cuts on higher priority programs and services

Budget Office Planning Principles • Revenue Considerations • Decisions about cost reductions need to consider the impact on revenue generation, as well as long-term capital and operating cost impacts. • Recruitment and Retention • Strategies should protect our ability to recruit, develop, and retain a diverse and highly qualified faculty, staff, and student body

Planning Principles • Strategic Investments • Strategic investments will continue to be made. These investments may require slightly larger budget cuts. • Efficiencies • Current processes and procedures should be streamlined to eliminate any duplicated or unnecessary services.

Draft Planning Principles • Staffing Layoffs • Every effort should be made to avoid layoffs or furloughs by taking advantage of normal attrition, planned retirements, and voluntary reductions. • Self-Supporting Departments • Recharge and income generating units are not exempt from the budget reduction process.