Download

1 / 10

100 likes | 268 Views

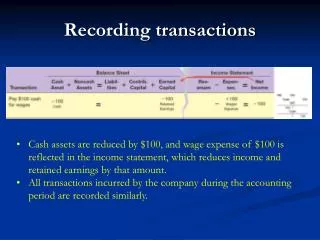

Recording Transactions. The “nuts and bolts” of accounting. T-Accounts. Expenses. Revenues. Debit. Credit. Debit. Credit. Liabilities. Assets. Debit. Credit. Debit. Credit. Owners’ Equity. Debit. Credit.

E N D

Recording Transactions The “nuts and bolts” of accounting

Expenses Revenues Debit Credit Debit Credit Liabilities Assets Debit Credit Debit Credit Owners’ Equity Debit Credit Expenses and Assets normally have a Debit balance; and Revenues, Liabilities and Owners’ Equity normally have a Credit balance.

Journal page 2 Notice that the cash transaction is a credit (less cash), but the balance is a (positive) debit balance, as usual. Account Cash Account No. 11 Account Prepaid Insurance Account No. 15

The Trial Balance Debits must equal credits on every transaction. Therefore, on the ledger (where all accounts are kept), total debit balances must also equal total credit balances. Frequently, accountants print out a Trial Balance that shows the debit or credit balances of each account. The sum total of the debit balances must equal the sum total of the credit balances. The Trial Balance may also have a debit and credit column showing the change in the balance from the previous accounting period. The Trial Balance is not a financial statement. It is an informal document that helps accountants check for errors in bookkeeping.

The Trial BalanceNovember 15, 2010 Obviously, there will be more accounts than this. But the format is accurate. This Trial Balance is NOT related to the earlier example of Journal posting, which showed an example of one transaction for a different business. Note: The Trial Balance encompasses all transactions over a period of time. As on any posting, the Trial Balance could show a Credit on the “Change” column but a debit on the “Balance” column. Change Balance