Download

1 / 16

180 likes | 347 Views

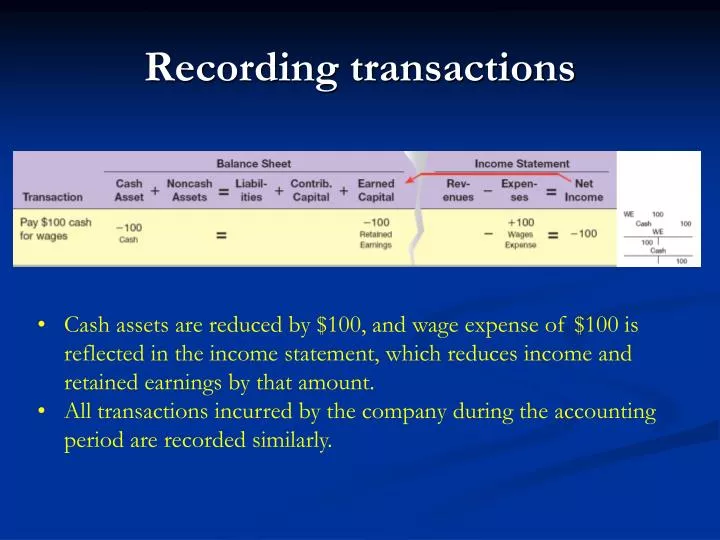

Recording transactions. Cash assets are reduced by $100, and wage expense of $100 is reflected in the income statement, which reduces income and retained earnings by that amount. All transactions incurred by the company during the accounting period are recorded similarly. Adjusting Accounts.

E N D

Recording transactions • Cash assets are reduced by $100, and wage expense of $100 is reflected in the income statement, which reduces income and retained earnings by that amount. • All transactions incurred by the company during the accounting period are recorded similarly.

Exercise: The Ice Cream Store, Inc. The Ice Cream Store, Inc. incurred the following start-up costs: • The Ice Cream Store, Inc. was formed on October 1, 20XX, with the investment of $90,000 in cash by the owners. • Obtained a bank loan and received the proceeds of $35,000 on October 2. The cash will be used for operations. • Purchased equipment for $25,000 cash on October 2. • Acquired a building at a cost of $80,000. It was financed by making a $20,000 down-payment and obtaining a mortgage for the balance. The transaction occurred on October 2. • On October 2, the President of the United States publicly declared that she will eat (and plug) our ice cream while entertaining guests in the White House. Prepare a transaction analysis of 1. – 5. using the financial statement effects template:

Ice Cream Shop Balance Sheet:

Ice Cream Shop – additional transactions • On October 4, purchased merchandise inventory (i.e., ice cream) at a cost of $15,000 by paying $5,000 cash and receiving short-term credit for the remainder from the supplier. • Immediately returned some of the ice cream because some of the flavors delivered were not ordered. The cost of the inventory returned was $3,000. • Sales of ice cream for the month of October, 20XX, totaled $8,000. All sales were for cash. The ice cream cost $3,500. • For all of October, total employee wages and salaries earned/paid were $3,000. • As of the end of October, one month's depreciation on the equipment and building was recognized -- $383 for the building and $167 for the equipment. • $450 interest expense on the note and mortgage was due and paid on October 31. Assume that the principal amounts ($35,000 + $60,000) of the note and mortgage remain unchanged. Prepare a transaction analysis of 6. -11. using the balance sheet/income statement template presented above:

Prepare the following financial statements (ignore income taxes): (i) an updated Balance Sheet as of October 31, 20XX; and (ii) an Income Statement for the month of October 20XX.

Additional Sources of Information • Form 10-K • Item 1, Business; Item 1A. Risk Factors; • Item 2, Properties; • Item 3, Legal Proceedings; • Item 4, Submission of Matters to a Vote of Security Holders; • Item 5, Market for Registrant’s Common Equity and Related Stockholder Matters; • Item 6, Selected Financial Data; • Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations; • Item 7A, Quantitative and Qualitative Disclosures About Market Risk; • Item 8, Financial Statements and Supplementary Data; • Item 9, Changes in and Disagreements With Accountants on Accounting and Financial Disclosure; • Item 9A, Controls and Procedures.

Additional Sources of Information • Form 8-K • Entry into or termination of a material definitive agreement (including petition for bankruptcy) • Exit from a line of business or impairment of assets • Change in the company’s certified public accounting firm • Change in control of the company • Departure of the company’s executive officers • Changes in the company’s articles of incorporation or bylaws

Credit and Data Services • Credit Analysis • Standard & Poor’s (StandardAndPoors.com) • Moody’s Investors Service (Moodys.com) • Fitch Ratings (FitchRatings.com) • Data Services • Thomson Corporation (Thomson.com) • First Call - summary of analysts’ earnings forecasts • Compustat database - individual data items for all publicly traded companies or for any specified subset of companies.