Download

1 / 21

220 likes | 454 Views

ANALYZING AND RECORDING TRANSACTIONS. Chapter 2. Record relevant transactions and events in a journal. Analyze each transaction and event from source documents. Post journal information to ledger accounts. Prepare and analyze the trial balance. Analyzing and Recording Process. C1.

E N D

ANALYZING AND RECORDING TRANSACTIONS Chapter 2

Record relevant transactions and events in a journal Analyze each transaction and event from source documents Post journal information to ledger accounts Prepare and analyze the trial balance Analyzing and Recording Process C1

Source Documents C2 Bills from Suppliers Checks Purchase Orders Employee EarningsRecords Bank Statements Sales Tickets

The Account and its Analysis C3 An account is a record of increases and decreases in a specific asset, liability, equity, revenue, or expense item. The general ledger is a record containing all accounts used by the company.

Asset Accounts C3 Cash Accounts Receivable Land AssetAccounts Notes Receivable Buildings Prepaid Accounts Equipment Supplies

Liability Accounts C3 Accounts Payable Notes Payable LiabilityAccounts Unearned Revenue Accrued Liabilities

Equity Accounts C3 Owner’s Equity Owner’s Withdrawals EquityAccounts Revenues Expenses Owner’s Capital

– – + + Owner’s Capital Owner's Withdrawals Revenues Expenses The Account and its Analysis C3 = + Assets Liabilities Equity

Ledger and Chart of Accounts C4 The ledger is a collection of all accounts for aninformation system. A company’s size and diversityof operations affect the number of accounts needed. The chart of accounts is a list of all accounts and includes anidentifying number for each account.

A T-account represents a ledger account and is a tool used to understand the effects of one or more transactions. Debits and Credits C5

= + Assets Liabilities Equity EQUITIES ASSETS LIABILITIES Debit Credit Debit Credit Debit Credit +- - + - + Double-Entry Accounting C5

_ _ Owner’s Capital Owner's Withdrawals + Revenues Expenses Owner’s Capital Owner's Withdrawals Revenues Expenses Debit Credit Debit Credit Debit Credit Debit Credit - + +- - + +- Double-Entry Accounting C5 Equity

An account balance is the difference between the increases and decreases in an account. Notice the T-Account. Double-Entry Accounting C5

= + Assets Liabilities Equity Step 1: Analyze transactions and source documents. Step 2: Apply double-entry accounting Step 4: Post entry to ledger Step 3: Record journal entry Journalizing & Posting Transactions P1

T-accounts are useful illustrations, but balance column ledger accounts are used in practice. Balance Column Account P1

Analysis: Double entry: 101 Posting: Analyzing Transactions A1 301

Analysis: Double entry: Posting: 101 126 Analyzing Transactions A1

Analysis: Double entry: Posting: 101 167 Analyzing Transactions A1

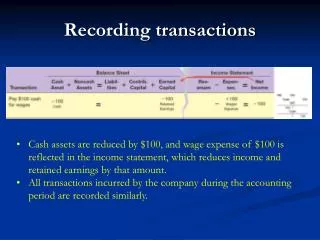

FastForward Trial Balance December 31, 2009 Debits Credits Cash $ 4,350 The trial balance lists all account balances in the general ledger. If the books are in balance, the total debits will equal the total credits. Accounts receivable - Supplies 9,720 Prepaid Insurance 2,400 Equipment 26,000 Accounts payable $ 6,200 Unearned consulting revenue 3,000 C. Taylor, Capital 30,000 Owner's Withdrawals 200 Consulting revenue 5,800 Rental revenue 300 Salaries expense 1,400 Rent expense 1,000 Utilities expense 230 Total $ 45,300 $ 45,300 After processing its remaining transactions for December, FastForward’s Trial Balance is prepared. P2

Preparing a Trial Balance P2 Preparing a trail balance involves three steps: List each account title and its amount (from ledger) in the trial balance. If an account has a zero balance, list it with a zero in the normal balance column (or omit it entirely). Compute the total of debit balances and the total of credit balances. Verify (prove) total debit balances equal total credit balances.